The Manley Macro Memo

Should Investors Sell in May and Go Away? We believe the economy is on the verge of recession, and the next leg of the Bear Market is imminent.

If you enjoy our work, please hit the like button and share our memo with others! Thanks, JLM

Summary

The major stock market averages were mixed in March. The S&P 500 and Nasdaq 100 rallied by 3.5% and 9.3%, respectively, while the small-cap Russell 200 fell by 5.2%. The main driver of financial assets in March was turmoil in the banking system. SVB and Signature Bank failed, and First Republic dropped by 89% as a liquidity crisis spread to the U.S. banking system. To stop the bank runs, the Federal Reserve created the Bank Term Funding Program, which provides one-year loans to banks to meet depositors' redemption requests. While the Fed's lending program successfully ended the bank runs, the Regional Bank Index finished March down 28.8%, which indicates that despite the Fed's intervention, fundamental problems remain in our financial system.

S&P 500 is currently up a respectable 7.7% year to date, but most of this appreciation was driven by a handful of mega-cap technology stocks. According to Bianco Research, more than 80% of the S&P 500's year-to-date gain is from only eight stocks (Apple +27.2%, Microsoft +18.8%, Amazon +29.7%, Google +20.6%, Tesla +34.1%, Meta +77.3%, Nvidia +86.7%, and Netflix +13.2%). Incredibly, Apple and Microsoft accounted for approximately 3.0% or 40% of the S&P 500's year-to-date performance.

We believe the S&P 500's strong performance this year is not due to a favorable economic environment but due to passive investment flows (401(k) contributions and corporate buybacks) and quantitative investment strategies (that invest based on volatility and not the fundamentals. While the S&P 500 is up nearly 8% year-to-date, most NYSE stocks are below their 200-day moving average and in a bear market. The market's weak breadth is consistent with a bear market rally and an economy headed toward a recession.

The economy's leading indicators uniformly indicate that a recession is likely. To fight inflation, which reached a 40-year high, the Fed aggressively raised interest rates by 5% in 13 months. This aggressive tightening has pushed the credit-sensitive sectors of the economy (housing, manufacturing, and durable goods) into recession and created instability in our financial sector. We expect this weakness will spread to the rest of the economy, and we'll enter a recession later this year. Also, we think the problems in the financial sector will lead to a credit crisis as overleveraged commercial real estate and public and private companies have difficulty refinancing their maturing debt.

Stocks offer a very poor risk-reward since valuations are historically high and corporate profits are declining. Sharply higher interest rates drove stocks down last year, and we believe stocks are poised for another decline as the economy enters recession and profits disappoint. Bear markets usually trough with the S&P 500 selling less than 14 times peak earnings. Since earnings peaked last March at $210, the S&P 500 could fall to 3000, which is an additional 28% decline from its current level.

In this high-risk environment – economic uncertainty and problems in the banking sector – we believe a nearly 5% risk-free rate is very attractive. We have a significant investment in a 2-year U.S. Treasury ladder, yielding around 5% and giving us a solid return until the headwinds are reduced, and stocks and bonds offer better risk-reward.

Market Review:

The major stock market averages were mixed in March. The S&P 500 and Nasdaq 100 rallied by 3.5% and 9.3%, respectively, while the small-cap Russell 200 fell by 5.2%. The main driver of financial assets in March was turmoil in the banking system. SVB and Signature Bank failed, and First Republic dropped by 89% as a liquidity crisis spread to the U.S. banking system. To stop the bank runs, the Federal Reserve created the Bank Term Funding Program, which provides one-year loans to banks to meet depositors' redemption requests. While the Fed's lending program successfully ended the bank runs, the Regional Bank Index finished March down 28.8%, which indicates that despite the Fed's intervention, fundamental problems remain in our financial system.

The turmoil in the banking sector led to a "flight to safety" in which bond yields plunged, and gold rallied 7.9%. The yield on the U.S. 2-year Treasury note dropped 1.02% in three days, which was the sharpest decline since the 1987 stock market crash. Additionally, the 10-year Treasury bond fell by 0.42% in March to yield 3.49%. The sharp drop in interest rates led to a surge in interest-sensitive growth stocks. The Russell 1000 Growth Index rallied by 6.6%, while the Russell 1000 Value Index fell by 1.1% in March. Also, the technology sector jumped by 10.6% as Apple, Microsoft, and Nvidia rallied by 11.9%, 15.6%, and 19.6%, respectively.

The S&P 500 finished the first quarter 7.5% higher. Most of the appreciation was driven by a handful of mega-cap technology stocks. Without the Technology sector's 21.8% Q1 gain, the S&P 500 would have increased by 2.7%, which is similar to the S&P 500 Equal-Weight Index (+2.9%), and the small-cap Russell 2000 (+2.7%).

In the first quarter, the safe havens (gold and the U.S. long-term Treasury bond) rallied by 8.8% and 7.0%, respectively, which is consistent with our macro view that economic growth is slowing and a recession is likely later this year.

Financial Market Performance

The S&P 500 is currently up a respectable 7.7% year to date, but most of this appreciation was driven by a handful of mega-cap technology stocks. According to Bianco Research, more than 80% of the S&P 500's year-to-date gain is from only eight stocks (Apple +27.2%, Microsoft +18.8%, Amazon +29.7%, Google +20.6%, Tesla +34.1%, Meta +77.3%, Nvidia +86.7%, and Netflix +13.2%). Incredibly, Apple and Microsoft accounted for approximately 3.0% or 40% of the S&P 500's year-to-date performance.

This year, we believe the S&P 500's strength is due to non-fundamental passive flows and not an improving investment outlook. While the S&P 500 is up 7.7% year-to-date, the equal-weighted S&P 500 (each stock has an equal weighting instead of a weighting based on its market value) is up only 3.1%, and the small-cap Russell 2000 has appreciated by 2.2%.

The S&P 500 is a market cap-weighted index, so the larger stock's performance has an outsized impact on the index's performance. While the mega-cap tech stocks have been very strong this year, most stocks have appreciated modestly, which is typical during periods of slowing growth and increasing economic risk.

Source: Stockcharts.com

Historically, the stock market was a discounting mechanism that was a sound leading indicator of the economy. We believe that the advent of passive investing has structurally changed the S&P 500 and made it a coincident indicator of economic activity. Over 45% of the S&P 500 is owned by passive investment funds that buy or sell stocks based on investment flows (contributions and redemptions), not fundamental change. As passive investing has grown significantly over the past few decades, the S&P 500 has become more inelastic (less stock is available due to the passive holders), and its price is increasingly a function of investment flows instead of the fundamentals.

According to Tier 1 Alpha, 401(k) retirement plans contribute $70 billion monthly to the financial markets, with around $38 billion flowing into equities. Also, corporations announced that they expect to buy back $1 trillion of stock this year, which is an additional $83 billion each month. Since the S&P 500 is currently valued at $34.5 trillion, passive retirement contributions into the stock market and share buybacks will equal 4.2% of its value.

While passive flows are important in the short term, profits and interest rates drive the long-term value of the market. As the economy slows, we believe the main drivers of passive flows – the unemployment rate at a 54-year low and artificially low corporate interest rates – are waning and could become significant headwinds when the economy enters recession later this year.

We believe the S&P 500's strong performance this year is not due to a favorable economic environment but due to passive investment flows and quantitative investment strategies (CTA's, Risk Parity, Vol Target) that invest based on volatility and not the fundamentals. While the S&P 500 is up nearly 8% year-to-date, most NYSE stocks are below their 200-day moving average and in a bear market. The market's weak breadth is consistent with a bear market rally and an economy headed toward a recession.

The S&P 500 is up nearly 8% this year, yet 55% of NYSE stocks are below their 50-day and 200-day moving averages. The market's weak breadth is consistent with a bear market rally and an economy headed toward a recession.

Source: Stockcharts.com

Economic Outlook:

Our tactical asset allocation is driven by the business cycle and the likely path forward for the economy and corporate profits. While the coincident economic indicators -- GDP growth, the unemployment rate, and inflation -- tell us how the economy is doing today, the economy's leading indicators – the yield curve, the Conference Board's LEI, the money supply, and the credit-sensitive cyclical components of the economy (housing, manufacturing, capital investment) -- help us estimate where the economy is headed. Once we understand where the economy and profits are headed, we build a diversified and balanced portfolio based on investments that perform best in that economic environment.

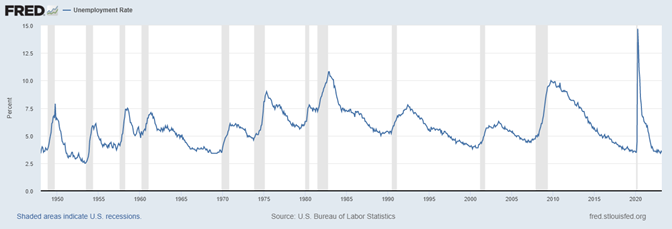

While we focus on the leading indicators, the media, and many Wall Street analysts focus on the labor market – which is a lagging indicator of the economy – to estimate the economy's health. In fact, in February, U.S. Treasury Secretary Yellen said, "You don't have a recession when you have 500,000 jobs and the lowest unemployment rate in more than 50 years." Unfortunately, Sec. Yellen is wrong. The unemployment rate is usually near its cyclical low when the recession starts. Also, the labor market isn't a good coincident economic indicator because the data is prone to heavy revisions, especially in recessions. Basically, high unemployment doesn't cause a recession; a recession causes high unemployment.

Strong labor markets do not prevent recessions. The unemployment rate is typically near its cyclical low when the recession starts. For example, the unemployment rate was 3.9% three months before the start of the 2001 recession, and the unemployment rate was 4.7% one month before the 2008 Great Financial Crisis.

Source: FRED

The economy's leading indicators uniformly indicate that a recession is likely soon. To fight inflation, which reached a 40-year high, the Fed aggressively raised interest rates by 5% in 13 months. This aggressive tightening has pushed the credit-sensitive sectors of the economy (housing, manufacturing, and durable goods) into recession and created instability in our financial sector. We expect this weakness will spread to the rest of the economy, and we'll enter a recession later this year. Also, we think the problems in the financial sector will lead to a credit crisis as commercial real estate, and public and private companies have difficulty refinancing their maturing debt.

The yield curve's slope is the most accurate economic indicator. Every post-WWII recession was preceded by an inverted yield curve (short-term interest rates yield more than long-term interest rates). The yield curve has been inverted since July and is the most inverted since 1981. Since the yield curve typically inverts 12 months before a recession, a recession will likely occur this summer.

Source: FRED

Another accurate indicator of the economy is the Conference Board's Leading Economic Index. The LEI is currently forecasting a recession. According to famed economist David Rosenburg, the LEI has had a perfect record of forecasting recessions since 1959.

Source: The Conference Board

Historically, to fight inflation, the Fed tightens until something breaks. This isn't surprising since the Fed focuses on lagging economic indicators (inflation and employment) and ignores the yield curve, the money supply, and other leading economic indicators. We believe the SVB and Signature bank failures may mark the beginning of a credit crisis that will spread to overleveraged commercial real estate, private equity, and public zombie companies.

Milton Freidman famously said: "inflation is always and everywhere a monetary phenomenon." The Fed ignored the surging money supply, and inflation rose to a 40-year high. Today, the money supply's growth rate has collapsed, and economic growth and inflation will continue to decline throughout this year.

Source: Fred

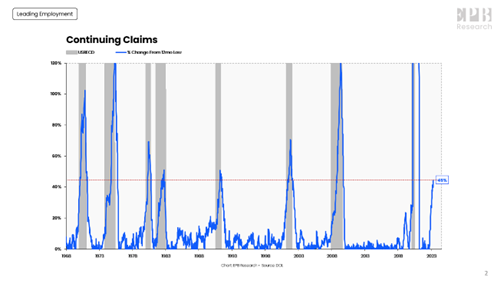

While most investors focus on the labor market to gauge the economy's health, it is interesting to note that it has begun to deteriorate. The average hourly work week is declining (a precursor to layoffs), and Continuing Unemployment Claims have increased by 45% from their 12-month low, which is consistent with previous recessions. Given the weakness in the leading economic indicators and the acceleration in continuing claims, we expect the labor market is poised to contract, which will signal to most investors that the economy is in recession.

Source: EPB Research

In Sum

The Fed, the media, and most investors ignore the economy's leading indicators and instead myopically focus on the labor market, which is a lagging economic indicator. The Fed raised interest rates at an unprecedented rate to fight the inflation that it helped create. Most Fed tightening cycles led to a recession and a credit event. The leading indicators show that a recession is likely later this year, while the Fed-induced problems in the banking sector make a credit crisis likely when trillions of dollars of debt come due in the next two years. Although the unemployment rate is at a 50-year low, there are signs that the labor market is deteriorating, and we may already be in recession. Since the S&P 500 depends on passive 401(k) retirement flows, a deteriorating labor market may deleteriously impact the S&P 500 and its mega-cap components.

Financial Market Outlook:

In our view, the stock market offers a poor risk-reward -- stocks are overvalued, earnings are declining, and investors are complacent even though the economy is on the verge of a recession. According to Factset, the S&P 500 sells at 18.2 times 12-month forward earnings, which is an earnings yield of 5.5%. Since the risk-free 3-month U.S. Treasury bill yields 4.85%, and the 10-year U.S. Treasury bond yields 3.5%, investors are not adequately compensated for taking equity risk. Also, stocks have rarely been this expensive based on long-term valuation measures (Market cap to GDP, Shiller Cape, and Tobin-Q).

Earnings usually decline by 20% during recessions. Despite the downturn in the credit-sensitive sectors of the economy and the problems in the banking sector, ebullient Wall Street analysts estimate that earnings will grow by 0.8% this year. We believe this is too optimistic, especially since Q1 reported earnings have dropped by 6.1%.

Market Value to GDP – "Still, it is probably the best single measure of where valuations stand at any given moment." –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks are 60% higher than their historical average level and more expensive than during the 2000 technology bubble.

Source: Longtermtrends

Shiller's CAPE (a valuation measure that smooths out cyclical earnings fluctuations) indicates that stocks are more than 50% above their long-term average.

Source: Longtermtrends

Investors are complacent despite expensive stocks, declining earnings, and an economy on the verge of a recession. The VIX, which measures the cost of options, is more than one standard deviation from its long-term average, which shows investors are not buying much insurance.

In Sum:

Stocks offer a very poor risk-reward since valuations are at a historical high and corporate profits are declining. Sharply higher interest rates drove stocks down last year, and we believe stocks are poised for another decline as the economy enters recession and profits disappoint. Bear markets usually trough with the S&P 500 selling at less than 14 times peak earnings. Since earnings peaked last March at $210, the S&P 500 could fall to 3000, which is an additional 28% decline from its current level.

In this period of economic uncertainty, we believe a nearly 5% risk-free rate is very attractive. We have a significant investment in a 2-year U.S. Treasury ladder, yielding around 4.75% and giving us a solid return until the headwinds are reduced, and stocks and bonds offer better risk-reward.

Our Model Portfolio:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

Our portfolio is mainly positioned for a recessionary environment – i.e., declining growth rates and falling inflation. We are underweight stocks relative to our 60/40 benchmark and invested in the value stocks and the defensive sectors of the stock market – healthcare, staples, and utilities.

We have significant fixed-income exposure on shorter-term U.S. Treasury notes (two years and less). Short-term Treasuries are attractive because they have a high risk-free yield, which pays us nearly 5% to wait until there is less economic and financial uncertainty. Our gold investment has performed well this year, and we expect significant outperformance as the economy enters recession and a credit crisis develops.

So far this year, our defensive portfolio has underperformed our benchmark. As interest rates declined due to problems in the banking sector, investors rotated into the interest-sensitive technology sector, which has appreciated by 18.2% this year. We believe that the technology sector has the worst risk-reward among the sectors of the S&P 500. Valuations are extreme, and earnings are more cyclical than most investors think. The tech sector prospered by pulling business forward during the pandemic, and we believe its profits will be vulnerable as spending is reduced during the recession. A similar boom-bust cycle occurred in the tech sector in 2000, when business soared before Y2K and then plummeted during the 2001 recession.

In Sum:

The leading economic indicators show that a recession is likely later this year. The recent Fed-induced problems in the banking sector indicate that a credit crisis may develop when borrowers try to refinance their maturing debt. Despite this dire outlook, stocks have rarely been more expensive, especially relative to a risk-free 3-month Treasury bill that yields nearly 5%.

We believe we are positioned to perform well in a challenging investing environment. As the economy slows, our defensive equity investments and gold should outperform, and our large 2-year Treasury ladder pays us a solid return to wait for a better environment. Above all, during this challenging economic environment, we will focus on preserving capital until the economic headwinds have dissipated and the stock market offers a better risk-reward.

Current Risk-Weighted Model Portfolio:

Our portfolio's risk level (annualized volatility) is 6.7%, which is less than our 60\40 benchmark's risk level of 13.1%.

Thank you for reading The Manley Market Memo.

Subscribe for free to receive new posts and support our work.

Also, this post is public, so please feel free to share it. And we appreciate any likes!

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. All investments contain risk.