The Manley Macro Memo

Investors are ebullient that the Fed has orchestrated a soft landing, yet corporate profits have declined for three consecutive quarters, and the leading economic indicators continue to deteriorate.

If you enjoy our work, please hit the like button and share our memo with others! Thanks, JLM

Summary

The S&P 500 rallied by 6.5% in June and finished the second quarter up 8.2%. During Q2, interest rates rose -- the U.S.10-year Treasury bond increased by 0.33% to yield 3.82%, and the U.S.10-year Treasury note rose by 0.81% to yield 4.87% -- while gold and oil declined by 3.2% and 6.6%, respectively. Despite the "risk-on" investing environment, the yield curve (3-month T-bill minus the 10-year U.S. Treasury bond) inverted to -1.6%, which is the deepest inversion in 41 years.

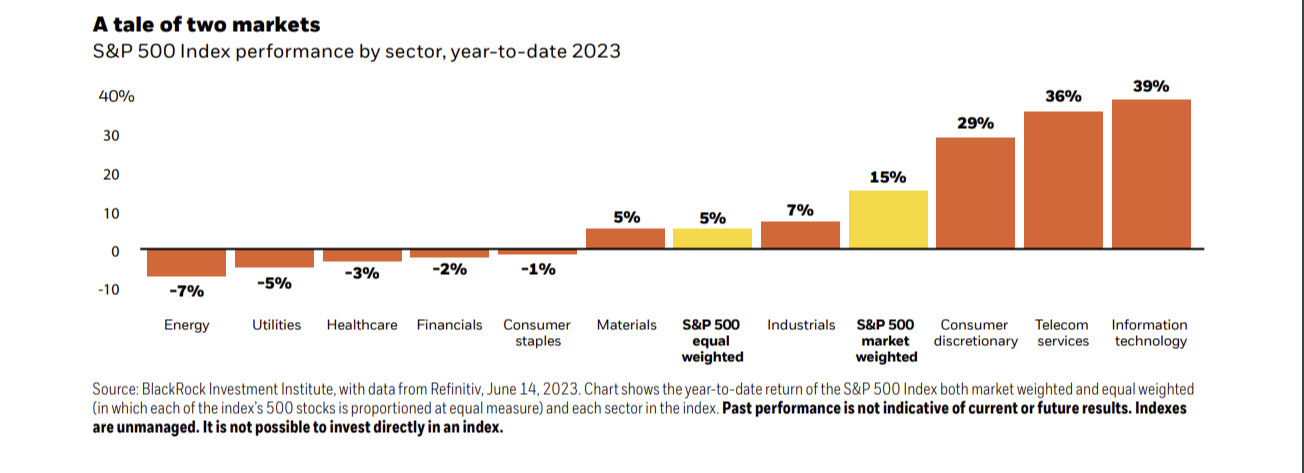

The "Magnificent Seven" (AAPL, MSFT, AMZN, GOOG, META, TSLA, NVDA) are currently 28% of the S&P 500, a record concentration level. According to Goldman Sachs, they have increased by more than 50% this year and are accountable for nearly 70% of the S&P 500's year-to-date return. The remaining 493 stocks in the S&P 500 are up about 5% this year and are significantly below last year's high.

According to S&P Global, the estimated 2023 operating earnings fell slightly to $216.9 during the second quarter, which increased the S&P 500's P/E from 18.8 to 20.5. Also, since interest rates rose sharply during the quarter, the Equity Risk Premium (the stock market's earnings yield minus the three-month U.S. Treasury bill) for the stock market fell sharply (0.40%). Historically, the ERP is around 5%, so the stock market is very unattractive relative to a 5.2% risk-free U.S. Treasury bill.

Investors are ebullient that the Fed has orchestrated a soft landing, yet corporate profits have declined for three consecutive quarters, and the leading economic indicators continue to deteriorate. Since monetary policy acts with a lag, and credit growth will continue to decline due to the regional bank crisis, we expect economic growth to slow and corporate profits to disappoint.

Despite weak fundamentals and an expensive stock market, many pundits believe we are in a new cyclical bull market. Traditionally, new bull markets are characterized by a shift in leadership and robust market breadth. We doubt that we are in a new bull market because the S&P 500 was driven higher by seven mega-cap stocks, which have been the market leaders since the 2008 financial crisis. Also, if we were in a new bull market, the small-cap Russell 2000 should be leading – instead, it's lagging.

We continue to believe that we are in a high-risk environment and think a 5% risk-free rate is very attractive. We are positioned in the market's defensive sectors and have a significant investment in a 2-year U.S. Treasury ladder, yielding around 5%. Our portfolio is well positioned to provide a solid return until the economic headwinds are reduced and stocks and bonds offer better risk-reward.

Q2 Market Review:

The S&P 500 rallied by 6.5% in June and finished the second quarter up 8.2%. During Q2, interest rates rose -- the U.S.10-year Treasury bond increased by 0.33% to yield 3.82%, and the U.S.10-year Treasury note rose by 0.81% to yield 4.87% -- while gold and oil declined by 3.2% and 6.6%, respectively. Despite the "risk-on" investing environment, the yield curve (3-month T-bill minus the 10-year U.S. Treasury bond) inverted to -1.6%, which is the deepest inversion in 41 years.

Since 1968, every time short-term rates yielded more than long-term rates, a recession occurred with an average lead time of 14 months. One of the key explanations behind an inverted yield curve's ability to forecast the last eight recessions lies in the challenges it creates for banks and financial institutions, resulting in reduced lending, which leads to slower economic growth.

The S&P 500's strong Q2 performance was due to a significant increase in valuation and not improving fundamentals. According to S&P Global, the estimated 2023 operating earnings fell slightly to $216.9 during the second quarter, which increased the S&P 500's P/E from 18.8 to 20.5. Also, since interest rates rose sharply during the quarter, the Equity Risk Premium (the stock market's earnings yield minus the three-month U.S. Treasury bill) for the stock market fell sharply from 0.70% to (0.40%). Historically, the ERP is around 5%, so the current valuation level makes the stock market unattractive, especially relative to risk-free U.S. Treasury bills.

Despite several positive macro events occurring in the second quarter -- such as the U.S. successfully averting a debt default, the subsiding of the regional bank crisis, a decline in the inflation rate, stable labor market conditions, and the Federal Reserve's decision to hold interest rates steady during its June meeting -- the primary catalyst behind the remarkable performance of the S&P 500 was an exuberant rally in the mega-cap technology stocks.

The "Magnificent Seven" (AAPL, MSFT, AMZN, GOOG, META, TSLA, NVDA) are currently 28% of the S&P 500, a record concentration level. According to Goldman Sachs, they have increased by more than 50% this year and are accountable for nearly 70% of the S&P 500's year-to-date return. The remaining 493 stocks in the S&P 500 are up about 5% this year and are significantly below last year's high.

The "Magnificent Seven" (AAPL, MSFT, AMZN, GOOG, META, TSLA, NVDA) have increased by more than 50% this year and are accountable for nearly 70% of the S&P 500's year-to-date return. According to Goldman Sachs, the remaining 493 stocks in the S&P 500 are up about 5% this year and are significantly below last year's high.

The conventional wisdom is that the mega-cap technology stocks benefitted from the belief that the economy would avoid recession, and investing in the "Magnificent Seven" was the best way to capitalize on the excitement around artificial intelligence and the very successful debut of ChatGPT. While these narratives led to significant inflows into the technology sector, we believe that oversold technicals and market structure issues best explain the mega-cap tech stocks' parabolic move.

In 2022, the stock and bond markets experienced a sharp decline due to the Federal Reserve's aggressive measures to combat inflation by raising short-term interest rates, thereby intentionally slowing down the economy. This interest rate increase directly impacted the valuation of investments, as they are essentially the present value of future cash flows. Consequently, when interest rates rise, the value of these anticipated cash flows diminishes.

During periods of rising interest rates, growth stocks tend to be more susceptible because a significant portion of their earnings is projected to materialize further into the future. Hence, when the Federal Reserve raised interest rates from 0% to 4.1% last year, it led to a substantial decline of 29.1% in the Russell 1000 Growth Index. In comparison, the S&P 500 and Russell 1000 Value Index experienced 18.0% and 7.5% declines, respectively.

Despite being great franchises (some having monopolistic characteristics) with strong balance sheets and robust cash flows, the "Magnificent Seven" dropped on average 46.7% last year – significantly worse than the S&P 500 and the Russell 1000 Growth Index. While the Magnificent Seven have had a great six months this year, they were oversold after a terrible 2022.

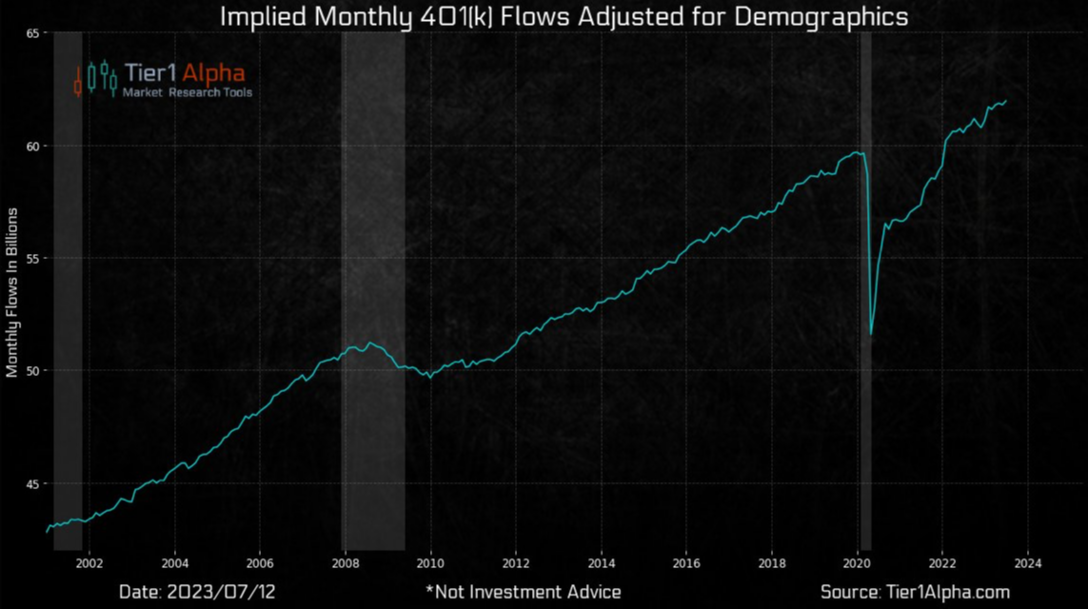

In addition to benefiting from an extreme oversold condition, the "Magnificent Seven" receive large passive inflows each month from 401k retirement plans and corporate buybacks, which can significantly impact their market values. Over 45% of the S&P 500 is owned by passive investment funds that buy or sell stocks based on investment flows (contributions and redemptions), not fundamental change. As passive investing has grown significantly over the past few decades, the S&P 500 has become more inelastic (less stock is available to buy or sell due to the passive holders), and its price in the short-term is increasingly a function of investment flows instead of the fundamentals.

The "Magnificent Seven" are about 28% of the S&P 500 (see table above), so they receive $28 out of every $100 invested in the S&P 500. Since passive investing's market share has created an inelastic market, these flows, coupled with corporate buybacks, have an outsized impact on the value of these companies – i.e., the company's value increases by a significant multiple of the passive inflow. While these passive flows have a virtuous impact on the S&P 500 and especially the "Magnificent Seven", these passive flows can reverse (especially during a recession), leading to a negative feedback loop of selling into an inelastic market.

According to Tier 1 Alpha, 401(k) retirement plans contribute $70 billion monthly to the financial markets, with around $38 billion flowing into equities. Also, corporate buybacks could reach $1 trillion this year, which is an additional $83 billion each month. Since passive investing has made markets inelastic, these flows have an outsized impact on the value of the large corporations.

In Sum

Improving fundamentals did not drive the S&P 500 higher in the second quarter. Interest rates rose, the yield inverted more, and Wall Street reduced its 2023 earnings estimates. The S&P 500's 8.2% rally was solely due to an increase in the market's valuation.

The S&P 500's strong Q2 performance was due to its extreme 28% concentration in the oversold mega-cap tech stocks. These stocks benefited from large passive flows and quantitative investment strategies (CTA's, Risk Parity, Short Volatility, and 0 DTE options speculation) that invest based on volatility, not the fundamentals.

While passive flows can be significant in the short term, profits and interest rates drive the long-term value of the market. We believe the main drivers of passive flows – the unemployment rate near a 54-year low and artificially low corporate interest rates – are waning and will become significant headwinds as the economy slows and interest rates remain elevated.

Our Model Portfolio Review:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

Our performance for the first half of 2023 was disappointing. We were underweight the growth and technology stocks, which had rallied significantly, and overweight the market's defensive sectors (healthcare, staples, and utilities), which declined during the first half of the year.

Last year, our portfolio benefited from our decision to steer clear of mega-cap technology stocks, which experienced a significant decline of nearly 50%. However, our performance has suffered this year due to our avoidance of these stocks. We believe that mega-cap technology stocks carry an unfavorable risk-reward ratio due to their extreme valuations and earnings that are more cyclical than commonly perceived by investors.

The mega-cap technology sector thrived during the pandemic because growth was pulled forward. We anticipate its profits will become vulnerable as spending diminishes and the economy slows. We draw parallels to a similar boom-bust cycle that occurred in the tech sector in 2000, where business soared before Y2K and subsequently plummeted during the 2001 recession, we perceive a similar vulnerability today. Since the mega-cap stocks now represent 28% of the S&P 500, we believe the market is susceptible to a substantial decline.

As long-term value investors, we focus on valuation and the leading economic indicators to estimate the economy's likely path and corporate profits. Economic growth is declining, and we have been in a profit recession since the fourth quarter of 2022 (earnings are expected to fall by 8.1% in the recently concluded second quarter). Despite the "Magnificent Seven's" large rally in the first half, interest rates rose sharply, while the leading indicators and the credit-sensitive sectors of the economy continued to deteriorate, which indicates that we are in the early stages of the earnings recession.

Our portfolio remains positioned for a recessionary environment – i.e., declining growth rates and falling inflation. We are underweight stocks relative to our 60/40 benchmark and invested in the value stocks and the defensive sectors of the stock market – healthcare, staples, and utilities.

We have significant fixed-income exposure on shorter-term U.S. Treasury notes (two years and less). Short-term Treasuries are attractive because they have a high risk-free yield, which pays us more than 5% to wait until there is less economic and financial uncertainty. Our gold investment has performed well this year, and we expect significant outperformance as the economy enters recession and a credit crisis accelerates.

In Sum

Parabolic rallies in the mega-cap tech stocks drove the S&P 500 sharply higher in the first half of 2022. Since earnings estimates fell, leading economic indicators deteriorated, and interest rates increased, the market's risk-reward deteriorated significantly. Higher interest rates drove stocks down last year, and we believe stocks are poised for another decline as the economy slows and profits disappoint.

As the economy slows, our defensive equity investments and gold should outperform, and our large 2-year Treasury ladder pays us a solid return to wait for a better environment. Above all, during this challenging economic environment, we will focus on preserving capital until the economic headwinds have dissipated and the stock market offers a better risk reward.

Current Risk-Weighted Model Portfolio:

Our portfolio's risk level (annualized volatility) is 5.2%, which is less than our 60\40 benchmark's risk level of 9.1%.

Market Outlook

The stock market offers a very poor risk-reward, especially compared to a risk-free rate above 5%.

Stocks are overvalued, and investors are ebullient that the Fed has orchestrated a soft landing, yet corporate profits have declined for three quarters. Economic leading indicators and the credit-sensitive sectors of the economy are deteriorating, which indicates that the economy will continue to slow and corporate profits will disappoint.

The Fed began raising interest rates to fight inflation in March of 2022. Over the last 16 months, the S&P 500 has been flat while earnings declined and interest rates and valuations rose sharply. In our view, the stock market is priced for perfection, which is unlikely due to the weakness of the leading economic indicators and the long and variable lag times between changes in monetary policy and its economic impact.

The Fed, the media, and many investors ignore the economy's leading indicators and instead myopically focus on the labor market, which is a lagging economic indicator. We focus on the leading indicators and the credit-sensitive sectors of the economy to help us forecast the economy's most likely path. The leading indicators show that the economy is headed toward recession. It is unlikely that growth will accelerate since the monetary policy acts with a lag, and the economy is only beginning to be adversely impacted by the reduction in loan growth due to the regional banking crisis.

In addition to the yield curve, another accurate indicator of the economy is the Conference Board's Leading Economic Index. The LEI is currently forecasting a recession. According to famed economist David Rosenburg, the LEI has had a perfect record of forecasting recessions since 1959.

Milton Freidman famously said:" inflation is always and everywhere a monetary phenomenon." The Fed ignored the surging money supply, and inflation rose to a 40-year high. Today, the money supply's growth rate has collapsed, and economic growth and inflation will continue to decline.

The ISM Purchasing Manager Index is a widely recognized economic indicator that provides insights into the health and direction of the manufacturing industry in the United States. The ISM has contracted for eight consecutive months and indicates that the economy's manufacturing sector is in a recession. Since 1948, the economy has been in recession nearly every time the ISM was 46.

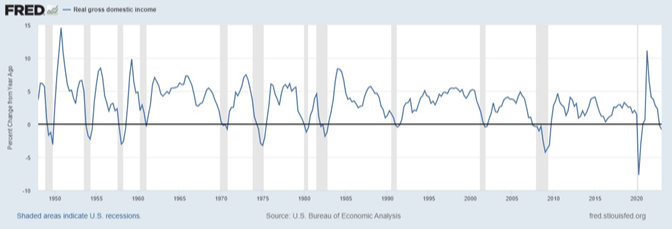

In addition to the leading economic indicators, several coincident indicators are contracting, indicating that we may already be in a recession. There are two measures of economic growth – Gross Domestic Product and Gross Domestic Income. GDP measures the total value of all final goods and services produced each year, while GDI represents the total income generated by the factors of production (such as labor and capital). While real GDP increased by 1.8% in the first quarter of 2023, real GDI declined by 0.8%. In our view, it is impossible to rule out a recession when real GDI is negative, and the full impact of the Fed's rate hikes and the reduction in credit growth due to the regional banking crisis has not yet impacted the economy.

Real Gross Income is a coincident economic indicator that has contracted over the past year and indicates that the economy may already be in recession.

According to ECRI, the Philadelphia Fed's GDPplus, which is based on information from both GDP and GDI is a better estimate of the economic activity that drives GDP and GDI. GDPplus also indicates that we are likely already in recession.

Several factors supported economic growth during this period of high inflation and rising interest rates. The Federal government ran a massive $2.25 trillion deficit (8.5% of GDP), the price of oil fell 22.7% over the last year, and households depleted their excess savings that were accumulated during the Covid lockdowns. We expect these beneficial factors to hurt growth as the deficit becomes more costly to finance due to higher interest rates, oil stabilizes because of OPEC's production cuts, and many households rebuild their savings and begin paying off their student loans after a three-year hiatus.

Despite the unemployment rate at a 50-year low, the budget deficit is 8.5% of GDP, which is greater than most recessionary periods. While the large government spending contributed to economic growth, it also spurred inflation. Since budget deficits increase significantly during a recession, weak growth, and high-interest rates place the U.S. in a vulnerable position.

Over the past year, the price of oil dropped by 22.7%, which acts as a "tax cut" for consumers. Unfortunately, OPEC's recent cutbacks and a decline in the rig count make a further drop unlikely unless there is a global recession.

While earnings are in recession, and further economic weakness is probable, the stock market is very expensive and priced for perfection.

Market Value to GDP – "Still, it is probably the best single measure of where valuations stand at any given moment." –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks are 60% higher than their historical average level and more expensive than during the 2000 technology bubble.

Source: Longtermtrends

Source: Longtermtrends

Despite weak fundamentals and an expensive stock market, many pundits believe we are in a new cyclical bull market. Traditionally, new bull markets are characterized by a shift in leadership and robust market breadth. We doubt that we are in a new bull market because the S&P 500 was driven higher by seven mega-cap stocks, which have been the market leaders since the 2008 financial crisis. Also, if we were in a new bull market, the small-cap Russell 2000 should be leading – instead, it's lagging.

New bull markets are characterized by a change in leadership and outperformance by the small-cap sector. The Russell 2000 outperformed the S&P 500 by 16.5% and 10% during the nine months after the 2002 and 2008 bear markets ended.

The S&P 500 bottomed last October and has risen by 25.6%, while the Russell 2000 has increased by only 14.8%. The small cap's poor relative performance indicates that this is not a new cyclical bull market.

In Sum:

The Federal Reserve increased interest rates at its most aggressive pace in forty years to fight inflation. Most Fed tightening cycles lead to a recession and a credit event. We believe that this historical sequence is playing out, and the leading indicators and the credit-sensitive sectors of the economy signal that a recession is likely.

We believe that stocks offer a very poor risk-reward because valuations are extreme, earnings are in recession, and the market's breadth is poor – i.e., S&P 500 is being driven by seven mega-cap technology stocks. Additionally, since monetary policy lags, the economy has yet to be fully impacted by the Fed's rate hikes and the contraction of credit growth due to the regional banking crisis.

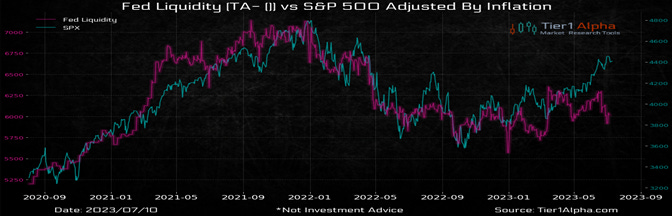

The "Magnificent Seven's" strength this year was because they were oversold after a terrible 2022, and they benefited from the passive flows, volatility-based quantitative strategies, and inelastic market structure. Liquidity drove the market higher during the first half of 2023, and the S&P 500 is vulnerable to a significant decline as the Fed shrinks its balance sheet by $95 billion monthly and real rates continue to increase as inflation falls. The S&P 500 is especially vulnerable since the overvalued mega-cap stocks represent 28% of the index.

The S&P 500 has decoupled from the Fed's liquidity. As the Fed pursues Quantitative Tightening and shrinks its balance sheet by $95 billion monthly, we believe the liquidity-based stock rally will end soon.

Thank you for reading The Manley Market Memo.

Subscribe for free to receive new posts and support our work.

Also, this post is public, so please feel free to share it. And we appreciate any likes!

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. All investments contain risk.