The Manley Macro Memo

Goldilocks or Stagflation?

Executive Summary:

Following a strong performance in the fourth quarter, the S&P 500 reached an all-time high in the first quarter. The S&P 500 and the S&P 500 Equal Weight Index increased by 10.6% and 7.9%, respectively, while the small-cap Russell 2000 advanced by 5.2%. Over the past two quarters, the S&P 500 rose by 22.5%. To explain the market's epic move, Wall Street crafted a "goldilocks" economic narrative, claiming the Fed defeated inflation and was poised to cut interest rates by 1.50% in 2024, despite disappointing inflation reports and an unemployment rate at a nearly fifty-year low.

Unfortunately, the economic data does not support Wall Street's narrative. The Bureau of Economic Analysis released a disappointing Q1 GDP report on Thursday. Economic growth unexpectedly slowed to a 1.6% annualized rate -- the lowest growth rate in six quarters and a significant decline from the previous quarter's increase of 4.9% -- while inflation surged at a greater-than-expected rate of 3.7%.

The Q1 GDP report confirmed that we are in a stagflationary economic environment driven by higher interest rates, tight lending standards, and a record budget deficit. The leading indicators still point to a recession, while the coincident indicators are mixed. We expect inflation will remain elevated until the economic weakness spreads to the remaining coincident indicators and we enter a mild recession.

We believe the stock market offers a poor risk-reward. Stocks are overvalued and offer a negative risk premium. Investors are positioned for a "goldilocks economy," yet recent economic data indicates that inflation remains elevated and growth is slowing. Market breadth is poor, while a few mega-cap technology stocks drive the S&P 500.

While the market's risk-reward is poor and the stagflationary economic environment is not favorable, Chairman Powell is clearly less concerned about fighting inflation and more concerned with easing financial conditions. It is unclear if his unnecessary dovish pivot is ineptness or politically motivated or if he sees a more significant problem coming.

We expect the stock market to trade in a wide range, with the upside limited by high valuations and the downside protected by the "Fed's Put." As value investors, we will add to our equity exposure in periods of weakness and reduce our risk exposure when the market is overbought and investors are too optimistic.

Market Review:

Following a strong performance in the fourth quarter, the S&P 500 reached an all-time high in the first quarter. The S&P 500 and the S&P 500 Equal Weight Index increased by 10.6% and 7.9%, respectively, while the small-cap Russell 2000 advanced by 5.2%. Over the past two quarters, the S&P 500 has increased by 22.5%. The primary drivers of this epic rally were the anticipation of the AI productivity boom and the belief that the Fed successfully defeated inflation and was poised to implement six interest rate cuts totaling 1.50% starting in March 2024.

However, despite the S&P 500 rallying to an all-time high in the first quarter, 2024 earnings expectations fell slightly, and the bond and commodity markets diverged from the prevailing "goldilocks" economic narrative of stable growth and declining inflation. As the table below indicates, the market's stout Q1 rally was due to an 11.1% increase in valuation, which is unusual since rising interest rates (the yield on the U.S. 10-year Treasury bond increased by 0.33%) and surging commodities (gold and oil appreciated by 12.7% and 15.6%, respectively) typically lead to a contraction in valuation.

In December, the Federal Reserve indicated that it was finished raising interest rates and was poised to cut interest rates in 2024. Wall Street extrapolated the Fed's dovish pivot into a "goldilocks" economic narrative that the Fed defeated inflation and would implement six interest rate cuts totaling 1.50% starting in March 2024. In addition to falling inflation and aggressive interest rate cuts, Wall Street estimated that the S&P 500's earnings would grow at about 11% in 2024 – truly an economic Nirvana.

The Fed didn't cut interest rates at their March meeting, as Wall Street expected, because the January and February inflation reports were disappointingly strong. Despite the bad inflation reports, Federal Reserve Chair Powell reassured the bulls that the goldilocks narrative was on track: "the recent data do not, however, materially change the overall picture, which continues to be one of solid growth, a strong but rebalancing labor market, and inflation moving down toward 2 percent on a sometimes bumpy path."

Unfortunately, the March inflation report (reported on April 10th) was again worse than expected and indicated that the inflation rate had, in fact, turned higher. On a six-month annualized basis, inflation rose to 3.6% in March from 3.0% in December 2023, while Core CPI increased by 0.3% to 3.8%.

Source: EPB Business Cycle Research

On April 16th, after three disappointing inflation reports, Fed Chair Powell pivoted again, which rebuffed the "goldilocks" narrative: "The recent data have clearly not given us greater confidence, and instead indicate that it's likely to take longer than expected to achieve that confidence...If higher inflation does persist, we can maintain the current level of restriction for as long as needed."

On December 13th, the Fed made a dovish pivot and said it would cut interest rates in 2024. It's been four months since the Fed's dovish pivot, yet there's been little improvement in inflation, and unemployment remains near a fifty-year low. Based on the table below, it is unclear why the Fed made its dovish pivot in December, but in hindsight, it was a mistake that artificially inflated stock prices and likely fueled inflation.

The S&P 500 rose by 22.5% over the past two quarters. To explain the market's epic move, Wall Street crafted a "goldilocks" economic narrative, claiming the Fed defeated inflation and was poised to cut interest rates by 1.50% in 2024, despite disappointing inflation reports and an unemployment rate at a nearly fifty-year low. We believe the S&P 500 surged because the U.S. Treasury and the Fed orchestrated a liquidity-driven rally, not because the U.S. entered a "goldilocks" economic environment.

Each quarter, the U.S. Treasury Department issues its Quarterly Funding Announcement, which outlines the amount of bonds and bills the Treasury will issue in the next quarter to fund the budget deficit. Typically, 80% of its issuance is in bonds, and 20% is in T-bills that mature in less than a year.

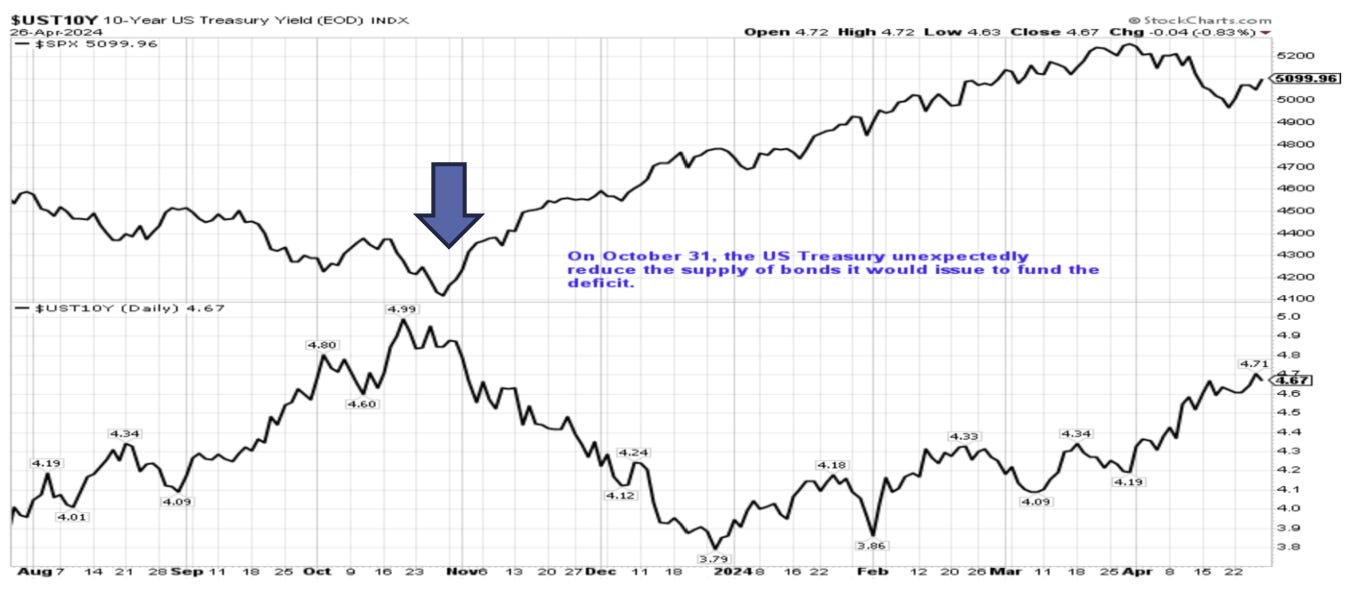

On October 30th, the U.S. Treasury unexpectedly announced that it would increase the issuance of bills from 20% to 60% and decrease its bond issuance to only 40%. The Treasury's actions led to sharply lower long-term interest rates and a surge in liquidity, which propelled stocks higher. By mid-December, the U.S. 10-year U.S. Treasury bond fell by 1.16% to 3.79%, and the S&P 500 surged 16.2%.

On December 13th, during the epic stock and bond market rally, Federal Reserve Chair Powell announced that the Fed was finished raising rates and was discussing when to cut them. This dovish pivot by the Fed was surprising since inflation was significantly above its 2% target, and only two weeks prior, on December 1st, Powell said, "It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance or to speculate on when the policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so."

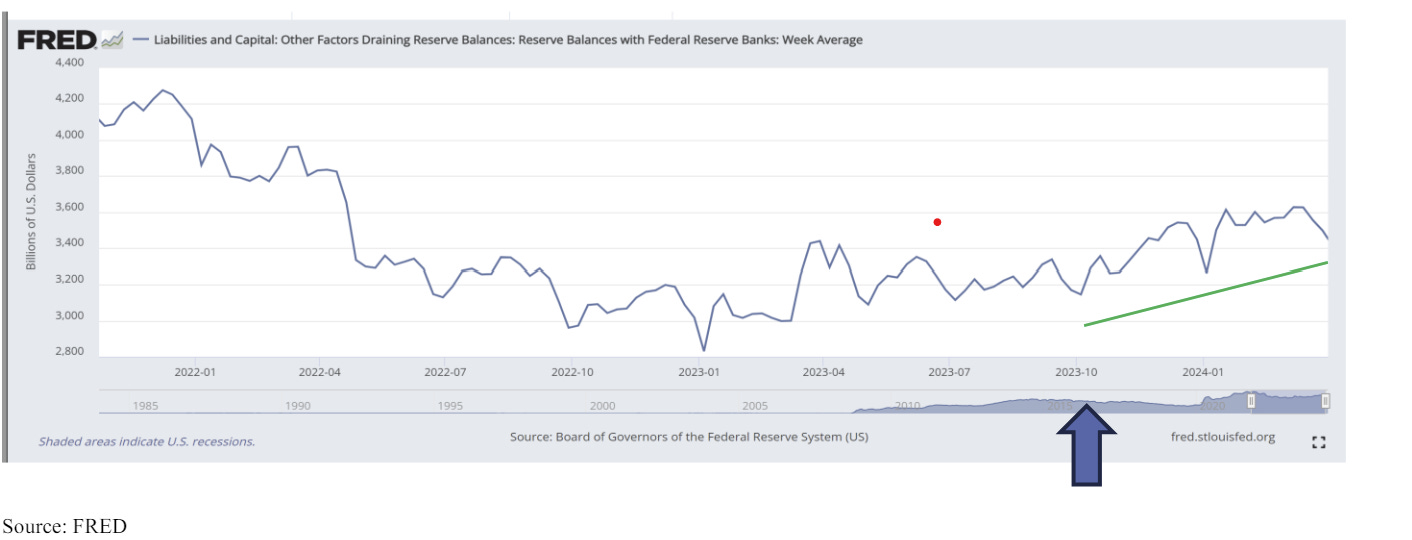

In addition to the U.S. Treasury-induced bond market rally and the Fed's dovish pivot, stocks rallied in Q4 and Q1 because of a liquidity surge. Despite higher short-term interest rates and Quantitative Tightening (the Fed is reducing the size of its balance sheet by $95 billion each month), bank reserves increased from $3.145 trillion on October 4th to $3.63 trillion in mid-March, an increase of $485 billion.

In our view, stocks surged over the past six months not because inflation was defeated or the economic environment improved but because of the surge in liquidity created by the U.S. Treasury and the Fed. Additionally, in this period of surging liquidity, systematic investors (CTA's, short volatility, and risk parity strategies that invest based on momentum and volatility, not the fundamentals) helped drive the equity market farther away from its intrinsic value.

In Sum:

The S&P 500 rose 22.5% during the last two quarters because the U.S. Treasury and the Fed orchestrated a liquidity-driven rally. To explain the market's epic move, Wall Street crafted a "goldilocks" economic narrative, claiming the Fed defeated inflation and was poised to cut interest rates by 1.50% in 2024.

Unfortunately, the economic data does not support Wall Street's narrative. The Bureau of Economic Analysis released a disappointing Q1 GDP report on Thursday. Economic growth unexpectedly slowed to a 1.6% annualized rate -- the lowest growth rate in six quarters and a significant decline from the previous quarter's increase of 4.9% -- while inflation surged at a greater-than-expected rate of 3.7%.

Last December, the Fed's dovish pivot was an unnecessary mistake that artificially inflated stock prices and likely spurred inflation. Unfortunately, this is only the Fed's latest policy mistake. In response to the Pandemic, the Fed printed nearly $3 trillion to stabilize the economy and support financial markets. This monetary surge drove inflation to a forty-year high. In February of 2022, inflation surged to 7.95%, yet the Fed kept short-term interest rates at 0% and continued to print money because it believed that inflation was "transitory." After several monetary mistakes, it is unclear why the Fed unnecessarily pivoted last December: is it inept, politically motivated, or is there a more significant problem that the Fed is trying to avoid by substantially easing financial conditions – i.e., commercial real estate and regional bank crisis?

Economic Outlook

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of economic growth and inflation rates. This enables us to strategically position our portfolio to perform well in all economic environments.

As discussed previously, Wall Street is positioned for a "Goldilocks" environment of accelerating economic growth and declining inflation. However, the Q1 economic data shows that we are in a stagflationary environment – i.e., growth is waning, and inflation is surprising to the upside.

For more than a year, the leading indicators of the economy -- the yield curve, money supply, and LEI --coupled with the contraction in the housing, manufacturing, and durable goods industries indicated that a mild recession was likely. The recession didn't occur because the Federal government ran a nearly $2 trillion budget deficit, and consumers significantly decreased their savings rate to spend more. Currently, the economy is bifurcated; the credit-sensitive areas are in contraction, while the service sectors are performing well. Since the government won't reduce its spending level – especially in an election year – we expect to remain in a stagflationary environment until the consumer reduces its spending and we have a mild recession.

According to the National Bureau of Economic Research (NBER), a recession is a significant decline in broad-based economic activity that lasts more than a few months. To determine the peaks and troughs in the economy, the NBER looks at six coincident economic indicators: real personal income less transfers, nonfarm payroll employment, employment as measured by the household survey, real personal consumption expenditures, real retail sales, and industrial production. As the chart below from EPB shows, only half of the coincident indicators are growing.

Source: EPB Business Cycle Research

Despite an unprecedented non-recessionary peacetime deficit, the coincident economic indicators are mixed, while the leading indicators point to a recession.

In Sum:

The Q1 GDP report confirmed that we are in a stagflationary economic environment driven by higher interest rates, tight lending standards, and a record budget deficit. The leading indicators still point to a recession, while the coincident indicators are mixed. We expect inflation will remain elevated until the economic weakness spreads to the remaining coincident indicators and we enter a mild recession.

Stock Market Outlook:

Over the past two quarters, investors drove the S&P 500 22.5% higher, believing that the Fed defeated inflation and was poised to reduce interest rates by 1.50%, while earnings grew at about 11%. Currently, stocks are overvalued, the market's breadth is poor, and stocks offer a poor risk-reward. Since the "Goldilocks" scenario isn't playing out, we expect that elevated inflation will lead to a contraction in valuation and a moderate correction for the S&P 500.

Over the past year, the S&P 500 appreciated by 24.1%, as earnings grew 7% and valuations increased by 16%. Based on long-term market measures, the stock market is significantly overvalued. Also, since the S&P 500 has a trailing earnings yield of 4.2% (EPS/price) and risk-free T-bills yield 5.3%, investors are not adequately compensated for assuming equity risk – i.e., stocks have a negative risk premium. Historically, the equity risk premium was 2.2% (6.6% average earnings yield minus 4.4% average risk-free rate) – currently, the ERP is -1.1%.

A narrow market breadth (very few stocks participating in the market rally) indicates that the market is unhealthy and could be vulnerable to a significant correction. While the S&P 500 reached a record high in Q1, the small-cap Russell 2000 remains nearly 14% below its all-time high and has essentially been flat over the past two years. This narrow market breadth is consistent with our view of slowing economic growth, not a goldilocks economic environment.

In Sum:

The stock market offers a very poor risk-reward. Stocks are overvalued and offer a negative risk premium. Investors are positioned for a "goldilocks economy," yet recent economic data indicates that inflation remains elevated and growth is slowing. Market breadth is poor, while a few mega-cap technology stocks drive the S&P 500.

While the market's risk-reward is poor and the stagflationary economic environment is not favorable, it is clear that Chairman Powell is less concerned about fighting inflation and more concerned with easing financial conditions. It is unclear if his unnecessary dovish pivot is ineptness, politically motivated, or if he sees a more significant problem coming. We expect the stock market will trade in a large range with the upside limited by high valuations and the downside protected by the "Fed's Put." As a value investor, we will add to our equity exposure in periods of weakness and reduce our risk exposure when the market is overbought and investors are too optimistic.

Our Model Portfolio:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, we risk-weight our positions to manage volatility.

As long-term value investors, we focus on valuation and the leading economic indicators to estimate the economy's likely path and corporate profits. Currently, stocks are overvalued and offer a poor risk-reward. Additionally, we are in an unfavorable stagflationary economic environment, with slow growth and elevated inflation.

We are underweight stocks relative to our benchmark and overweight the healthcare and energy sectors, which typically outperform during periods of stagflation. About 60% of the portfolio is invested in short-duration bonds that yield about 5.5%. This is a great risk-reward, considering the S&P 500's earnings yield is only 4.2%. Also, since the stock market's historical average return is 10%, we receive 55% of the market's historic return with no principal risk.

We expect to maintain a significant short-term fixed-income position until there is less economic uncertainty and stocks offer a favorable risk-reward. Finally, we are invested in gold – the ultimate safe haven – which is performing well this year due to geopolitical stress, economic uncertainty, and central bank ineptness.

In Sum:

We expect a volatile year, and we believe that stocks will be in a broad trading range with the upside capped by extreme valuation and the downside protected by the "Fed Put." In this environment, we will add to our equity exposure in periods of weakness and reduce our risk exposure when the market is overbought and investors are too optimistic.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. All investments contain risk.