The Manley Macro Memo

The S&P 500 rallied 17% higher over the past 8-weeks due to favorable seasonality and positive fund flows. We expect the bear market to resume when the year-end rally ends in January.

If you enjoy our work, please hit the like button and share our memo with others! Thanks, JLM

Summary

The S&P 500 rallied by more than 17% from its mid-October low. In our view, this was a bear market rally fueled by favorable seasonality, corporate buybacks, passive inflows from 401k's, and declining volatility. We expect the bear market to resume when the year-end rally ends in January.

The bear market's first leg– driven by higher interest rates and declining valuations – ended in October. Next year, we think stocks will breach October lows as the economy falters and corporate profits fall. Our base case for next year is that a mild recession leads to a 10% earnings decline. In this environment, the S&P 500 could fall to 3000, which would be a 16.5 P/E multiple on earnings of $180.

We believe the economy is entering a recessionary period of declining growth and inflation. We are invested in the stock market's defensive sectors, U.S. Treasury bonds, and gold, which have historically performed well during recessionary periods. Since stocks remain overvalued and Wall Street earnings expectations seem unrealistic (estimated +13.3% profit growth in 2023), we will continue to focus on preserving capital and managing portfolio risk.

Stocks and bonds performed poorly this year because the Fed aggressively raised interest rates to slow economic growth and fight inflation, which reached a 40-year high. The higher interest rates pushed down the valuations of all financial asset classes. In fact, stocks and bonds declined for only the 5th time in the last 100 years. 2022 was a challenging year, and there was no place to hide – stocks and bonds were historically overvalued, while cash yielded 0.0%. Although we expect 2023 to be a challenging year for the economy, we see many opportunities to generate a solid positive return.

FINANCIAL MARKET PERFORMANCE

MARKET REVIEW:

Stocks and bonds are in a bear market this year because of a series of significant monetary mistakes by the Federal Reserve. Since the 2008 financial crisis, the Federal Reserve has tried to stimulate the economy by setting interest rates below inflation and printing money to buy bonds. This profligate policy led to weak economic growth, an increased debt burden, and a misallocation of capital. The artificially low-interest rates also pushed asset valuations to a historic level.

When the Pandemic struck in the spring of 2020, the Federal government and the Federal Reserve acted to stabilize and support the economy. The government increased its budget deficit to nearly 15% of GDP, while the Fed cut interest rates to 0% and printed $120 billion each month to buy mortgage securities and Treasury bonds.

As the economy recovered, the Fed maintained its emergency monetary measures, and the government continued to spend at a record rate. This unprecedented monetary and fiscal stimulus led to strong economic growth and elevated inflation. By June of 2021, inflation surged to 5%, yet the Fed failed to reduce its monetary stimulus because it believed that inflation was "transitory. Finally, in March of 2022, the Fed increased interest rates by 0.25% to a paltry yield of 0.50% and terminated its bond-buying program -- unfortunately, inflation had already reached 8.6%.

Despite strong economic growth and inflation at a 40-year high, the Fed failed to remove its emergency monetary measures because it incorrectly believed that inflation was "transitory."

Source: FRED

By early summer, the Fed realized inflation was not transitory and raised interest rates at the most aggressive pace since 1981. In nine months (from March to December), the Fed raised interest rates from 0.25% to 4.50%. Unfortunately, the Fed's actions led to an awful environment for stocks and bonds.

This summer, the Fed realized it was wrong and hiked interest rates at a record rate. This year, stocks and bonds declined because of the Fed's errors, and we believe the economy will suffer next year.

Source: Statista, and the Daily Shot

The S&P 500 fell by 27.5% from its January all-time high to its mid-October low, while the 10-year U.S. Treasury bond declined by 16.1% because the Federal Reserve aggressively increased short-term interest rates to fight inflation, which reached a 40-year high. Although the Fed raised interest rates to slow economic growth and tame inflation, the higher interest rates also adversely affected the valuation of all financial assets (since asset values are the present value of future cash flows, higher interest rates lead to lower valuations).

In most economic environments, balanced portfolios of stocks and bonds (i.e., 60% stocks, 40% bonds) reduced portfolio risk and maintained most of the stock market's reward because stocks and bonds typically have a low or negative correlation. Additionally, in periods of recession or financial stress, bonds act as a safe haven and typically appreciate when stocks fall. In fact, since 1928, there were only five years when both stocks and bonds declined. Unfortunately, the Federal Reserve's monetary policy errors have led to balanced portfolios' worst performance since the Great Depression.

The Fed's aggressive rate hikes have led to a sharp equity bear market and the worst year on record for the U.S. Treasury bond market. Also, 2022 is only the fifth year since 1928, when stocks and bonds declined.

Source: Ned Davis Research

After declining nearly 30%, the stock market was oversold, and investors were pessimistic heading into the mid-term election. Historically, the stock market bottoms near the mid-term election and stocks typically rally into the new year. This year was no exception -- the S&P 500 bottomed in mid-October and rallied by 17.4%, which retraced 46% of the bear market decline in eight weeks.

We believe this robust advance is a technically driven bear market rally, and nothing fundamentally has changed or improved. Stocks were very oversold entering a strong seasonal period, which benefits from large passive inflows (401k contributions, target date funds, and corporate buybacks), and systematic investment strategies (risk parity, vol targeting, trend-following CTAs, and option gamma trading).

Many Wall Street strategists and reporters create narratives in an attempt to explain these technical or flow-based market moves. These pundits pushed the narrative that stocks were rallying because the Fed was poised to pivot, which would lead to an economic soft landing instead of a recession next year. Wall Street analysts support this ebullient economic view; according to S&P Global, S&P 500 earnings are forecasted to grow by 13.3% next year.

Despite the stout 8-week rally and the optimistic narrative, economic growth is slowing, and most market-based indicators continued to forecast a recession next year. Last week, the Fed also pushed back on the "Fed Pivot" narrative at its FOMC meeting. Instead of indicating that a pause and pivot was imminent, the Fed's Summary of Economic Projections forecast an additional 0.50% increase in short-term rates next year to 5.1%, and there would be no rate cuts until 2024. Additionally, Fed Chair Powell stated, "it is our judgment today that we are not at a sufficiently restrictive policy stance yet," and "we will stay the course until the job is done." "Restoring price stability will likely require maintaining a restrictive policy stance for some time," he said.

Since the 2008 financial crisis, the Fed's easy monetary policy (negative real rates and printing money to buy bonds) led to weak growth, the misallocation of capital, a record debt burden, and asset bubbles. When the Pandemic stuck, the Fed cut interest rates to 0% and grew its balance sheet by a massive $4.8 trillion to nearly $9 trillion. The Fed maintained its emergency measures until this March, when inflation reached 8.6%.

Last year, market-based indicators and the money supply indicated the economy was strong, and inflation would be a problem. Unfortunately, the Fed ignored these indicators and continued its unprecedented monetary stimulus, which drove inflation to a 40-year high. We believe that the Fed is making another monetary mistake by focusing on inflation and employment measures – which are lagging economic indicators – and again ignoring the message from the money supply and leading economic indicators. The yield curve, energy prices, and the Conference Board Leading Economic Index indicate that a recession is likely next year. Also, the plunging money supply growth rate shows that inflation has peaked and will decline to an acceptable level late next year.

The yield curve's slope is probably the most accurate economic indicator. Every post-WWII recession has been preceded by an inverted yield curve (short-term interest rates yield more than long-term interest rates). The yield curve has been inverted since July. Since the yield curve typically inverts 12 months before a recession, a recession is likely to occur next summer.

Source: FRED

The oil price is a reliable indicator of economic growth, and sharp declines usually presage an economic slowdown or recession. Currently, the price of oil declined by 30% over the last six months.

Source: stockcharts.com

Another accurate indicator of the economy is the Conference Board's Leading Economic Index. The LEI has declined for eight consecutive months and is currently forecasting a recession. According to famed economist David Rosenburg, the LEI has had a perfect record of forecasting recessions since 1959.

Source: The Conference Board

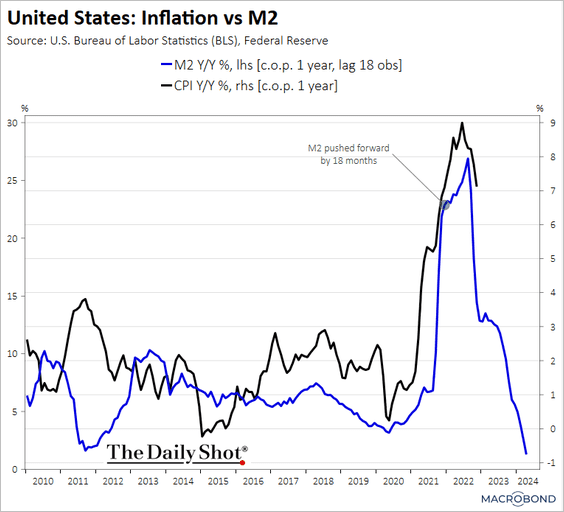

Milton Freidman famously said:" inflation is always and everywhere a monetary phenomenon. Last year, the Fed ignored the surging money supply, and inflation surged to a 40-year high. Today, the money supply's growth rate has collapsed, and inflation is poised to fall to an acceptable level later next year.

Source: MacroBond and The Daily Shot

We believe that the Fed is poised to make another monetary mistake that could lead to a deep recession beginning next year. The Fed is concerned about the labor market's impact on inflation. Since the unemployment rate is at 3.7%, it believes that the labor market is out of balance (too many jobs and not enough workers), which will lead to further wage increases and fuel inflation. The Fed's solution is to slow economic growth and rebalance the labor market by reducing the number of jobs.

The problem (other than its policy goal of reducing employment) is that inflation and employment are lagging economic indicators, and today's numbers may not accurately represent the present economic environment. Also, monetary policy acts with a lag, so last week's interest rate hike won't impact the economy for approximately a year. In essence, the Fed is looking in the rearview mirror to make policy decisions that won't impact the economy until next fall.

Another problem with making monetary decisions based on the employment market is that the government jobs data is imprecise or flawed. It excludes discouraged workers, makes inaccurate birth-death estimates, contains seasonal adjustments, and there are substantial annual benchmark revisions to the jobs data. In fact, last week, the Philadelphia Fed reported that it believes the establishment payroll data may have significantly overestimated hiring. It estimates that only 10,500 new jobs were created in the second quarter of this year rather than the Bureau of Labor Statistics estimate of 1,121,500 new jobs. If this initial revision is accurate and the labor market isn't as strong as the government data suggests, the Fed is making another monetary mistake by tightening monetary policy into an economic slowdown – which isn't surprising since most Fed tightening cycles led to recession.

Market Outlook:

Stocks and bonds performed poorly this year because the Fed aggressively raised interest rates to slow economic growth and fight inflation. The higher interest rates pushed down the valuations of all financial asset classes. In fact, stocks and bonds declined for only the 5th time in the last 100 years.

We believe that the bear market's first leg– driven by higher interest rates and declining valuations – ended in October. Currently, stocks are in a seasonal countertrend rally which started near the mid-term election and should end next month. Next year, we think stocks will breach their October low as the economy falters and corporate profits decline. While stocks will struggle, we expect U.S. Treasury bonds and gold to perform well as we enter a recessionary economic environment (i.e., declining growth and falling recession).

In our view, stocks are especially vulnerable next year because Wall Street analysts and retail investors are far too optimistic about the economy's strength. As discussed previously, most leading indicators of the economy estimate that a recession is likely next year. Typically, S&P 500 earnings decline by about 20% in a recession. According to S&P Global, Wall Street analysts forecast corporate profits to grow by 13.3% next year. This growth estimate seems exceedingly unlikely since profit margins are near a record high and vulnerable as interest rates rise and growth slows.

Corporate profits are 11.1% of GDP, which is about two standard deviations above its 60-year average of 7.2%. Profit margins are highly mean reverting and vulnerable as interest rates rise and growth slows.

Source: FRED

In addition to Wall Street analysts, retail investors seem too optimistic. According to EPFR, households typically sell about $10 billion in stocks after the S&P 500 falls at least 10% from its peak. Despite a 30% decline and the worst year for stocks since the 2008 financial crisis, mutual funds and ETFs have attracted more than $100 billion this year, which is the highest annual amount on record, according to EPFR data. Usually, bear markets end with panic and capitulation. Since it appears that the retail investors "bought the dip" this year instead of selling, we believe the bear market has much more downside.

In Sum:

The first leg of the bear market was due to rising interest rates and their negative impact on the value of financial assets. We believe the next leg down for stocks will be driven by a weak economy and declining profits. While economically sensitive stocks will suffer, we think that U.S. Treasury bonds, gold, and the defensive sectors of the S&P 500 (healthcare, consumer staples, and utilities) will perform well in this recessionary economic environment.

We believe the stock market has a poor risk-reward. Despite the short-term positive impact of fund flows (passive 401k contributions, corporate buybacks, and systematic trading strategies), stocks have a limited upside because retail investors are too optimistic, and WS earnings expectations seem unrealistic in a slowing economy. The market's downside is predicated on the depth of the recession and how far earnings decline, which will be driven by the Fed's monetary policy. Our base case for next year is that a mild recession leads to a 10% earnings decline. In this environment, the S&P 500 could fall to 3000, which would be a 16.5 P/E multiple on earnings of $180.

In our view, the bear market will not end until stocks are cheap, the economy is in recession, the Fed is cutting interest rates, Wall Street analysts are pessimistic, and retail investors have panicked.

Portfolio Review:

This year we performed well relative to our 60/40 benchmark because of our defensive investment posture, which was underweight stocks and invested in the market's defensive sectors (healthcare, consumer staples, utilities). Also, our investments in gold, energy stocks, commodities, and TIPs (Treasury Inflationary Protected Securities) helped us perform well in the stagflationary economic environment of elevated inflation and slowing growth.

Since very few asset classes (energy stocks, oil, and the U.S. dollar) appreciated this year, it was a challenging investing environment. We believe inflation has peaked and will moderate next year as growth slows and the economy enters a mild recession. Historically, in recessionary environments safe havens (gold and long-term U.S. treasury bonds), defensive stocks (healthcare, utilities, and consumer staples), and high-quality bonds perform well. While growth and economically sensitive stocks, commodities, and lower credit-quality bonds perform poorly.

Our portfolio is mainly positioned for a recessionary environment; only energy stocks and the Goldman Sachs commodity index remain from our Stagflation portfolio. We expect to hold these positions as insurance against an escalation this winter in Ukraine. We have focused our fixed-income exposure on shorter-term U.S. Treasury notes (two years and less) because they have a high risk-free yield and will provide capital gains if we enter a recession next year.

In 2022, there was no place to hide – stocks and bonds were historically overvalued, and cash yielded 0.0%. Although we expect 2023 to be a challenging year for the economy, we see many opportunities to generate a solid positive return.

Current Risk-Weighted Model Portfolio:

Our portfolio's risk level (annualized volatility) is 11.8%, which is significantly less than our 60\40 benchmark's risk level of 18.7%.

Thank you for reading The Manley Market Memo.

Subscribe for free to receive new posts and support our work. Also, this post is public, so please feel free to share it.

We appreciate any likes!

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. All investments contain risk.