The Manley Macro Memo

The S&P 500 is significantly overvalued and is not adequately diversified since 30% of the index is concentrated in six mega-cap technology companies.

Executive Summary:

The stock market was mixed during the second quarter. The S&P 500 increased by 3.9% during Q2, while the equal-weight S&P 500 and the Russell 2000 declined by 3.0% and 3.6%, respectively. Also, the Russell 1000 Growth index rallied by 8.2% in the quarter, while the Russell 1000 Value index fell by 2.4%. It is very rare to have such a bifurcated market, and the market's poor breadth is a negative sign.

The S&P 500 increased by a stout 14.5% during the first half of 2024, while the equal-weight S&P 500 and the Russell 2000 increased by 4.1% and 1.1%, respectively. The MSCI EAFE International and the MSCI Emerging Markets indexes also increased by 4.0% and 5.9%, respectively. Similar to q2, the S&P 500's outperformance was driven by the 30% concentration in the mega-cap technology stocks that benefited from the AI infrastructure buildout.

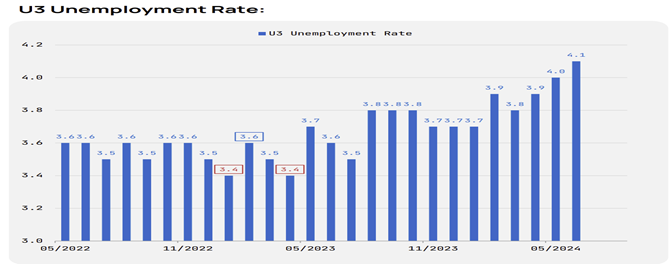

Early in the second quarter, the economic data was surprisingly strong – inflation remained sticky, while job growth exceeded expectations. Wall Street feared that the economic data would prevent the Federal Reserve from reducing short-term interest rates. June's economic data, which was reported this month, showed that inflation was approaching the 2.0% Fed's target, and the unemployment rate increased to 4.1%, which is 0.70% above its cyclical low (see chart below). Wall Street currently expects the Fed to cut interest rates by 0.25% in September and December.

The economy's leading indicators signaled that a recession was likely this year. Elevated inflation and high interest rates pushed the cyclical sectors of the economy into contraction, but massive government spending prevented the economy from falling into recession. This year, the budget deficit is estimated to be 7% of GDP, and government spending is expected to increase by 12.4%. The current level of deficit spending is unsustainable and is leading to a significant debt problem. It is estimated that this year, the U.S. will spend more to service its debt than on our military.

The stock market offers a very poor risk-reward. The S&P 500 is significantly overvalued and is not adequately diversified since 30% of the index is concentrated in six technology companies. We are concerned that there is an AI bubble and that any slowdown in capital spending will adversely impact the S&P 500. While investors are positioned for a "goldilocks economy," we believe the economy has avoided recession due to the massive and unsustainable budget deficits. We believe the modest performance of the Russell 2000 better reflects the fundamentals than the S&P 500, which is overly impacted by AI spending and passive flows.

We expect the stock market to trade in a wide range, with the upside limited by high valuations and the downside protected by the "Fed's Put." As value investors, we will add to our equity exposure in periods of weakness and reduce our risk exposure when the market is overbought and investors are too optimistic.

Second Quarter Review:

The stock market was mixed during the second quarter. The S&P 500 increased by 3.9% during q2, while the equal-weight S&P 500 and the Russell 2000 declined by 3.0% and 3.6%, respectively. Also, the Russell 1000 Growth index rallied by 8.2% in the quarter, while the Russell 1000 Value index fell by 2.4%. It is very rare to have such a bifurcated market, and the market's poor breadth is a negative sign.

Most stocks struggled during a challenging economic period marked by high interest rates, sluggish growth, and elevated inflation. However, the mega-cap tech stocks (Microsoft, Apple, Nvidia, Amazon, Meta, and Google) thrived due to the excitement surrounding Artificial Intelligence (AI) and their ability to invest in the expensive AI infrastructure buildout. The index significantly outperformed the broader market since these six companies account for 31% of the S&P 500. Remarkably, Nvidia—the biggest beneficiary of the AI infrastructure buildout—contributed more than 30% of the S&P's year-to-date performance through the end of June.

Despite the boom in AI spending, the S&P's 2024 earnings estimate increased by only 0.10% from March. As the table below indicates, the S&P 500's increase was primarily due to a 3.8% increase in valuation, which is unusual since rising interest rates (the yield on the U.S. 10-year Treasury bond increased by 0.17%) typically lead to a contraction in valuation.

The S&P 500 increased by a stout 14.5% during the first half of 2024, while the equal-weight S&P 500 and the Russell 2000 increased by 4.1% and 1.1%, respectively. The MSCI EAFE International and the MSCI Emerging Markets indexes also increased by 4.0% and 5.9%, respectively. Similar to q2, the S&P 500's outperformance was driven by the 30% concentration in the mega-cap technology stocks that benefited from the AI hype. Since 2024 earnings expectations fell by 0.8% in the first half, the S&P 500's appreciation was solely due to higher valuation, which is surprising since interest rates rose by 0.50% in the first half, and oil and gold prices increased by more than 10%.

Early in the second quarter, the economic data was surprisingly strong – inflation remained sticky, while job growth exceeded expectations. Wall Street feared that the economic data would prevent the Federal Reserve from reducing short-term interest rates. June's economic data, which was reported this month, showed that inflation was approaching the 2.0% Fed's target, and the unemployment rate increased to 4.1%, which is 0.70% above its cyclical low (see chart below). Wall Street currently expects the Fed to cut interest rates by 0.25% in September and December.

Source: EPB Business Cycle Research

In Sum:

The S&P 500 rose 14.5% during the first half of 2024, while the S&P 500 equal-weight index was up only 4.1%. The S&P 500's extreme 30% concentration in the six mega-cap tech stocks drove most of the index's outperformance. Since the S&P 500's 2024 earnings expectations decreased by 0.80% in the first half, the index's appreciation was solely due to valuation – not improving growth.

Since interest rates rose by 0.50% and commodity prices rose by more than 10%, the market's valuation increase is not due to lower interest rates or falling inflation. Instead, stocks were driven higher in the first half by two Wall Street narratives – the AI revolution and the Fed's orchestrated "soft landing." These narratives drove the S&P 500 to one of the most expensive levels in history. We remain concerned that stocks are very expensive, the market's breadth is weak, and the economy may be headed toward a mild recession. Additionally, the S&P 500 is not adequately diversified since only six names account for 30% of the index's value. While many pundits believe the six mega-cap stocks are safe havens – they declined by more than 40% in 2022.

Economic Outlook

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of economic growth and inflation rates. This enables us to strategically position our portfolio to perform well in all economic environments.

In June 2022, the inflation rate reached 9%, a 40-year high. The Fed aggressively raised short-term interest rates to slow the economy and reduce inflation to its 2% target. In July 2022, the yield curve inverted (the U.S. 2-year Treasury bond yielded more than the U.S. 10-year bond), indicating a probable recession.

Since 1968, every time short-term rates yielded more than long-term rates, a recession occurred with an average lead time of 14 months. One key explanation behind an inverted yield curve's ability to forecast the last eight recessions lies in the challenges it creates for banks and financial institutions. This results in reduced lending, which leads to slower economic growth. A flattening yield curve after inversion indicates that the recession is imminent.

Source: FRED

Last December, the Fed pivoted toward easing its monetary policy. Wall Street predicted that starting in March, the Fed would reduce interest rates by 1.5% in 2024 and successfully orchestrate a "soft landing." Stocks rallied on Wall Street's narrative that a "Goldilocks economy" of accelerating growth and falling inflation was imminent. Unfortunately, inflation remained elevated through the year's first half, and the rate cuts didn't occur. This month, BLS reported that the inflation rate fell to 2.5% (Core CPI was 3.1%), which many economists believe is low enough for the Fed to cut interest rates by 0.25% increments in September and December.

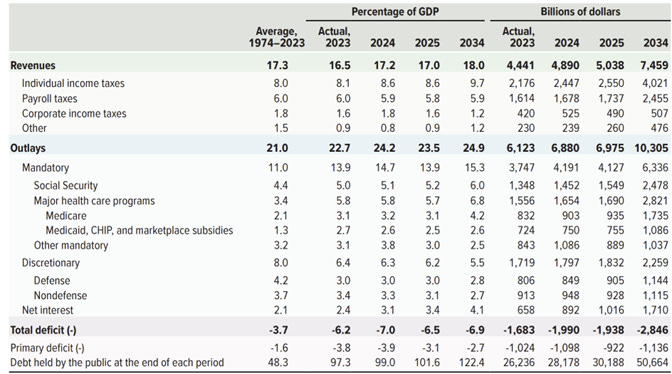

While Wall Street believes inflation is defeated and economic growth is poised to accelerate, we remain circumspect. We believe the economy has avoided recession due to the unprecedented level of government spending. Last year, the government ran a $1.7 trillion budget deficit (6.2% of GDP), and recently, the CBO revised its 2024 budget deficit forecast from $1.6 trillion to $2 trillion (7% of GDP). Incredibly, it estimates that government spending will increase by 12.4% in fiscal 2024. Deficits of this magnitude are unsustainable and put our country at significant financial risk. It is estimated that this year, the U.S. will spend more to service its debt than on our military.

Source: CBO

Despite record government spending, the economy remains bifurcated. The services sector performs well, while the credit-sensitive cyclical sectors are contracting. We believe that high interest rates and elevated inflation will continue to weigh on consumer spending, leading to weakness in the services sector.

As the election nears, the probability of a Republican sweep has increased. If a sweep occurs, the economy's primary driver will shift from the government to the private sector. We expect that low taxes and reduced regulations will significantly improve economic growth. Since government tax receipts averaged 17.9% of GDP (tax receipts averaged 17.3% over the past fifty years) after the Tax Cuts and Jobs Act of 2017 (TCJA), we are not concerned that low taxes will increase the deficit. However, spending must be reduced to its historical average of 21% of GDP or better to reduce the long-term structural imbalances, and excessive tariffs or a weak dollar policy could lead to higher inflation.

In Sum:

The economy's leading indicators signaled that a recession was likely this year. Elevated inflation and high interest rates pushed the cyclical sectors of the economy into contraction, but massive government spending prevented the economy from falling into recession. This year, the budget deficit is estimated to be 7% of GDP, and government spending is expected to increase by 12.4%. The current level of deficit spending is unsustainable and is leading to a significant debt problem. It is estimated that this year, the U.S. will spend more to service its debt than on our military.

If the GOP sweep occurs this November, its pro-growth policies of low taxes and deregulation will lead to better economic growth next year. However, government spending needs to be reduced, and excessive tariffs or a weak dollar policy could lead to higher inflation.

Stock Market Outlook:

We believe the stock market offers a poor risk-reward. Economic growth is slowing, stocks are extremely expensive, and the market's breadth is poor. Despite these factors, Wall Street is ebullient based on its soft-landing narrative and the generative AI mania. While we believe stocks offer a poor risk-reward (especially compared to a 2-year U.S. Treasury note), we are concerned that the S&P 500 is especially vulnerable because it lacks diversification (six stocks account for 30% of the index) and is driven by passive flows, not changes in the fundamentals.

Similar to the economy, the stock market is bifurcated. The S&P 500 appreciated 14.5% during the first half, while the equal-weight S&P 500 and the small-cap Russell 200 rose by 4.1% and 1.1%, respectively. While most stocks struggled with elevated inflation and high interest rates, the S&P 500 benefitted from its concentration in mega-cap technology stocks that gained from the AI infrastructure buildout.

The table below illustrates that the S&P 500 increased by 14.5% in the first half. This appreciation was solely due to an increase in valuation since the 2024 earnings estimate declined by 0.80%. Changes in long-term interest rates typically drive valuations, but since the U.S. 10-year bond increased by a massive 0.50%, something else caused the rally.

Although the S&P 500 significantly outperformed all other major equity indexes in the first half, we are concerned that the index is not adequately diversified and is detached from the fundamentals. The index benefited from its extreme 30% concentration in six mega-cap technology stocks, which prospered due to their exposure to the AI infrastructure buildout. Nvidia alone accounted for 30% of the S&P 500's first-half appreciation.

Chat GPT was launched in November of 2022. Since then, the six mega-cap tech stocks have had epic rallies.

Source: Stockcharts.com

While generative AI will lead to significant efficiency and productivity gains and, in healthcare, contribute to more timely disease diagnosis and important drug and healthcare discoveries, some experts are concerned that the modest revenue benefits so far do not justify the high cost. After eighteen months and hundreds of billions invested in the AI infrastructure, there is no killer application, and many tasks can't be performed on a cost-effective basis. Additionally, our nation's energy grid is a significant barrier that will slow AI development.

We believe that AI technology will be revolutionary and improve our lives for many decades to come. However, we are concerned that mega-cap tech stocks are priced for perfection, and any reduction in AI capital expenditures could significantly impact the value of these stocks and the S&P 500 – i.e., in 2022, the mega-cap tech stocks dropped more than 40%.

In addition to concentration risk and reliance on accelerating AI capex, we are concerned that the S&P 500 is not discounting the fundamentals because passive flows and speculative investment strategies drive it. The S&P 500 benefits from monthly 401k contributions that are passively invested in the index regardless of the fundamentals. More than thirty cents of each 401k contribution dollar is invested in the mega-cap technology stocks. Also, the S&P is impacted by quantitative investment strategies –short volatility, dispersion trades, risk parity, gamma squeezes, and trend following – that are not driven by the fundamentals – i.e., changes in earnings and interest rates. Changing market conditions can lead to forced selling as these quant strategies de-lever and unwind their speculative positions.

The S&P 500 is significantly overvalued and offers a very poor risk-reward. We expect the value and defensive sectors of the market to outperform relative to the rest of the market, and the small and midcap sectors could be poised for significant gains if pro-growth policies are implemented after the election.

Market Value to GDP – "Still, it is probably the best single measure of where valuations stand at any given moment." –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks are more than 100% higher than their historical average level and more expensive than during the 2000 technology bubble.

Source: Longtermtrends

In Sum:

The stock market offers a very poor risk-reward. The S&P 500 is significantly overvalued and is not adequately diversified since 30% of the index is concentrated in six technology companies. We are concerned that there is an AI bubble and that any slowdown in capital spending will adversely impact the S&P 500. While investors are positioned for a "goldilocks economy," we believe the economy has avoided recession due to the massive and unsustainable budget deficits. We believe the modest performance of the Russell 2000 better reflects the fundamentals than the S&P 500, which is overly impacted by AI spending and passive flows.

We expect the stock market to trade in a wide range, with the upside limited by high valuations and the downside protected by the "Fed's Put." As value investors, we will add to our equity exposure in periods of weakness and reduce our risk exposure when the market is overbought and investors are too optimistic.

Our Model Portfolio Review:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

As long-term value investors, we focus on valuation and the leading economic indicators to estimate the likely path of the economy and corporate profits. Currently, stocks are overvalued and offer a poor risk-reward. Additionally, we are in an unfavorable economic environment, with slow growth and elevated inflation. While the Fed will likely reduce interest rates by 0.25% this September, we believe it will have little favorable economic impact.

We performed well in the year's first half, especially on a risk-adjusted basis. We are outperforming the equal-weight 60/40, a more accurate measure of how most stocks performed. We are underweight stocks relative to our benchmark and overweight the healthcare consumer staples and energy sectors, which typically outperform during periods of slowing growth.

About 50% of the portfolio is invested in short-duration bonds that yield about 5.3%. This is a great risk-reward, considering the S&P 500's earnings yield is only 4.4%. Also, since the stock market's historical average return is 10%, we receive 53% of the market's historic return with no principal risk.

We expect to maintain a significant short-term fixed-income position until there is less economic uncertainty and stocks offer a favorable risk-reward. Finally, we are invested in gold – the ultimate safe haven – which is performing well this year due to geopolitical stress, economic uncertainty, and central bank ineptness. We also invested in several alternative investment strategies that increase our diversification and should perform well as the economy slows.

Current Risk-Weighted Model Portfolio

Our portfolio's risk level (annualized volatility) is 7.9%, which is less than our 60\40 benchmark's risk level of 10.4%.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. All investments contain risk.