The Manley Macro Memo

Q3 Market Review: Stocks Hit Record Highs Amid Fed Rate Cuts, AI Optimism, and Economic Uncertainty

Executive Summary:

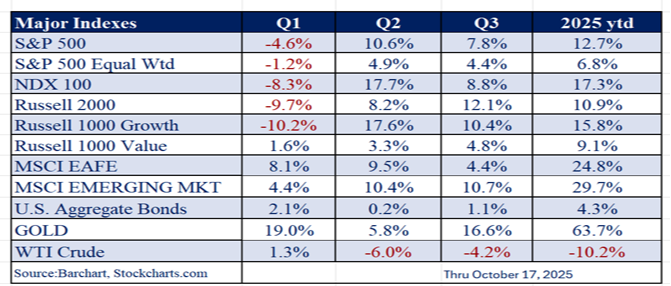

Stocks performed well in the third quarter as trade tensions eased and the economy proved resilient despite lingering uncertainty from tariffs, elevated inflation, and slowing labor market growth. Investors drove equities to new all-time highs and record valuations after the Federal Reserve signaled that labor market softness justified interest rate cuts. Meanwhile, optimism over the AI-driven capital spending boom fueled expectations for productivity gains and improved economic growth. In this risk-on environment, the S&P 500 advanced 7.8% during the third quarter, while the equal-weighted S&P 500 gained 4.4%. International equities also performed well, aided by a weaker U.S. dollar, with the MSCI EAFE Index up 4.4% and the MSCI Emerging Markets Index rising 10.7%. Despite the strength in risk assets, gold—often viewed as the ultimate safe haven and a “risk-off” asset—surged 16.6%, whereas oil slipped 4.2% over the same period.

We believe there is significant economic uncertainty driven by several factors. The nation’s heavy debt load and an unprecedented peacetime budget deficit have heightened long-term fiscal risks. Recent tariff hikes represent a record-breaking tax increase, which is a significant headwind for the economy. Additionally, persistent inflation and tepid wage growth have negatively impacted most Americans. Currently, economic strength relies overwhelmingly on three pillars: outsized government deficits, consumption concentrated among the top 10% of households, and a historic surge in AI-related capital spending. In our view, none of these factors is sustainable, and we expect disappointing economic growth in the future.

Stocks currently present a poor risk-reward as they are overbought and overvalued, with weak market breadth masked by AI-driven mania. Gold’s 60% rally this year is a clear signal that economic and market risks are elevated. The S&P 500 lacks adequate diversification, and its heavy concentration in mega-cap technology stocks makes it especially vulnerable to a correction if the AI boom fades. In this environment, we expect international equities, value stocks, and real assets to outperform the S&P 500.

We continue to maintain an underweight position in equities, particularly within the technology sector, while our bond exposure has little duration risk. Our allocation to international stocks, gold, and other precious metals provides economic balance and diversification, which we believe positions the portfolio to perform well in a period of economic uncertainty. We plan to maintain a highly diversified and balanced asset allocation until economic uncertainty diminishes and equities present a more favorable risk-reward opportunity.

Third Quarter 2025 Market Review:

The S&P 500 reached an all-time high in the third quarter, driven by easing trade tensions, rising expectations for Federal Reserve interest rate cuts, and AI euphoria. In this risk-on environment, the S&P 500 advanced 7.8% during the third quarter, while the equal-weighted S&P 500 and Russell 2000 small-cap indexes gained 4.4% and 12.1%, respectively. International equities also performed well, aided by a weaker U.S. dollar, with the MSCI EAFE Index up 4.4% and the MSCI Emerging Markets Index rising 10.7%.

Interest rates eased modestly during the quarter, providing support for equities. The U.S. 2-year Treasury yield declined 10 basis points to 3.62%, while the 10-year yield fell 6 basis points to 4.15%. Despite the strength in risk assets, gold—often viewed as the ultimate safe haven and a “risk-off” asset—surged 16.6%, whereas oil slipped 4.2% over the same period.

The U.S. economy continued to demonstrate resilience. The unemployment rate remained at a historically low 4.3%, while core inflation edged higher, rising from 2.9% in June to 3.1% in August. Real GDP expanded by 2.1% year-over-year in the second quarter, and according to S&P, corporate profits exceeded expectations, growing by 10.4%.

Stocks performed well in the third quarter as trade tensions eased and the economy proved resilient despite lingering uncertainty from tariffs, elevated inflation, and slowing labor market growth. Investors drove equities to new all-time highs and record valuations after the Federal Reserve signaled that labor market softness justified interest rate cuts. Meanwhile, optimism over the AI-driven capital spending boom fueled expectations for productivity gains and improved economic growth.

In the first quarter of 2025, stocks declined more than 20% as investors grew concerned that a potential trade war between the U.S. and its major trading partners. The market rebounded sharply when the Trump administration delayed the implementation of tariffs, and stocks rallied further as trade agreements were reached with minimal retaliation. Additionally, bond yields fell during this period, as the tariffs—poised to generate revenue greater than 1% of GDP—helped narrow the budget deficit.

As trade tensions eased, the labor market weakened. Job growth was revised significantly lower in the third quarter, and the Bureau of Labor Statistics announced that the U.S. economy added roughly 911,000 fewer jobs over the 12 months ending March 2025 than previously reported.

The Federal Reserve has a dual mandate to pursue maximum employment and price stability. At the Fed’s annual Jackson Hole conference in August, Chairman Jerome Powell notably shifted his emphasis, focusing more on growing labor market risks rather than persistent inflation. Discussing tariffs, he stated that “a reasonable base case is that the effects will be relatively short-lived—a one-time shift in the price level.” Powell went on to explain that “while the labor market appears to be in balance, it is a curious kind of balance—driven by marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly, in the form of sharply higher layoffs and rising unemployment.”

Powell’s comments were interpreted as a pivot toward prioritizing the labor market—signaling a willingness to cut interest rates aggressively should unemployment surge, even at the expense of tolerating somewhat elevated inflation. The market responded very positively to this dovish shift. The fixed income market priced in 0.75% of interest rate cuts in the fourth quarter of 2025 and at least another 0.70% in 2026. Since Powell’s dovish remarks at the Jackson Hole symposium on August 22nd, the S&P 500 advanced 4.4%, while gold surged a staggering 28%.

In addition to reduced trade tensions and the Federal Reserve’s dovish policy shift, a surge of AI-driven optimism propelled the stock market higher. Throughout Q3, unprecedented AI deals and record capital investment sparked substantial gains in the technology sector, which drove the S&P 500 higher.

In our view, stocks are priced for perfection. Investors are overlooking the structural issues of excessive debt, a $1.8 trillion budget deficit, and inflation that is significantly higher than the Fed’s 2% target. Even a weak labor market is considered a positive because it allows the Fed to ignore inflation and aggressively cut interest rates. Moreover, the full economic consequences of the recent tariffs— representing a significant tax increase exceeding 1.2% of GDP—have yet to be fully realized. We are concerned that the excitement about the dovish Fed and the AI mania are masking a weak economy, and if the AI capital spending boom slows from its torrid pace or the Fed is unable to stimulate growth, the economy and stocks are at risk.

Economic Outlook

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of the rate of change for economic growth and inflation. This enables us to strategically position our portfolio to perform well in all economic environments.

We believe the current environment is characterized by significant economic uncertainty, stemming from the nation’s substantial debt burden, an unprecedented peacetime budget deficit, and the implementation of tariffs representing a record-setting tax increase. Additionally, elevated inflation and sluggish wage growth have left many Americans feeling as though they have been in a recession ever since the pandemic.

Currently, the primary drivers of the economy are an unprecedented peacetime budget deficit, spending by the top 10% of households, and extensive AI capital investments, all of which, in our view, are unsustainable.

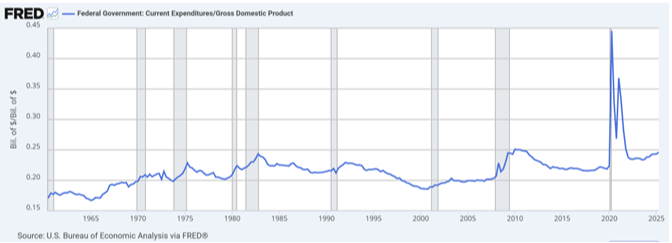

During the COVID pandemic, government spending surged to support individuals and stabilize the economy throughout the lockdowns. Since then, government spending has remained elevated and has not returned to pre-pandemic levels. According to the Congressional Budget Office, the budget deficit for fiscal year 2025, which ended in September, was $1.8 trillion, or 5.9% of the country’s GDP. While government revenue grew by 6%, spending still increased by 4%. Federal spending now stands at 23.1% of GDP—$358.7 billion above the pre-COVID 40-year average of 21.9%. This level of spending exceeds what is typical during most recessions and is particularly unprecedented given the historically low 4.3% unemployment rate.

Government spending increased by 54.2% from 2020 to 2025 and is currently 1.2% or $358.7 billion above its 40-year average spending-to-GDP ratio of 21.9%. Although the unemployment rate is low at 4.3%, government spending remains higher than during most past recessions.

Source: FRED

Alongside elevated government spending, current economic growth is increasingly being driven by the wealthiest households. The top 10% of households—those earning more than $250,000 annually—now account for nearly half of all consumer spending, up from about 36% several decades ago. This group is benefitting from a pronounced “wealth effect.” Since they own 87% of publicly traded stocks and are more likely to own their homes, record highs in equity markets and home prices have made them substantially wealthier, fueling even greater consumption.

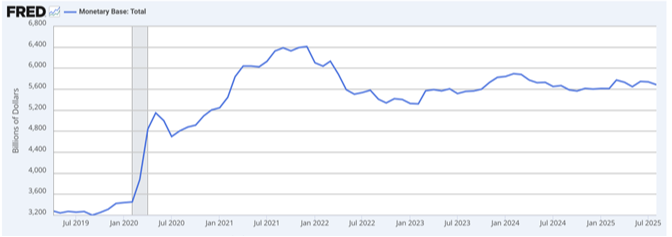

While loose monetary and fiscal policies implemented during and after the pandemic boosted asset values, which benefited the top 10% of households, these policies have also contributed to significant wealth inequality and persistent inflation for the broader population. Unfortunately, the Federal Reserve compounded these challenges by failing to sufficiently reduce its bloated balance sheet once the pandemic subsided. We believe this failure by the Fed led to a housing and stock market bubble. When these bubbles burst, the wealthy will reduce their spending, and the government’s massive budget deficit will expand.

The Federal Reserve did not sufficiently unwind its emergency policies after the pandemic, leading to a significant rise in inflation, which hit a forty-year high in 2022 and remains well above the Fed’s 2% target. This sustained inflation is due to the Fed’s failure to shrink its balance sheet adequately.

Source: FRED

Since OpenAI launched ChatGPT—the first mainstream AI assistant—in November 2022, capital spending on AI infrastructure has surged dramatically. Current AI-related spending now equals 1.5% to 2.0% of U.S. GDP. Remarkably, in the first half of 2025, AI investment accounted for roughly 92% of overall GDP growth. Without business investment in data centers, information processing equipment, and related technology, GDP growth would have been nearly flat at just 0.1%.

The surge in AI capital spending also drove technology stocks and the S&P 500 to record highs. This stock market strength contributed to the “wealth effect” discussed previously. We recognize that AI represents a profound technological advancement that may ultimately have an even greater impact on society than the internet. However, we are skeptical that AI capital spending can continue to grow at the current torrid pace and that all of the announced deals will come to fruition. In our view, the current environment of AI euphoria and easy financial conditions has fostered a classic investment bubble.

As with prior investment bubbles, investor excitement often drives an overestimation of future demand, leading to excessive building and, ultimately, a market correction or bust. While investors frequently suffer substantial losses when the bubbles burst, society as a whole tends to benefit in the long run. The surplus infrastructure and capacity created during the boom period often result in lower prices and expanded access, enabling new applications and future waves of innovation.

ChatGPT was launched nearly 3 years ago, and there is no “killer app” yet. Additionally, after spending hundreds of billions of dollars, there is very little AI revenue. In fact, OpenAI, the parent of ChatGPT, has committed to spending more than $1.0 trillion on AI infrastructure over the next five years, yet they are estimated to have revenue of only $15 billion and is expected to lose about $13 billion this year. Even if OpenAI could raise $ 1 trillion in capital, which is unlikely, the amount of energy needed would be massive. Recently, OpenAI’s CEO, Sam Altman, stated they need to build 250 gigawatts (GW) of new computing capacity by 2033 to power its AI ambitions – this is equivalent to about one-third of the entire U.S. peak grid demand.

The AI mania has recently been driven by capital spending commitments that seem dubious and rely on circuitous vendor financing that is typical late in a spending boom. While no one knows when the AI spending boom will bust, we are confident that the economy and stocks will be vulnerable.

In summary, we believe there is significant economic uncertainty, driven by several factors. The nation’s heavy debt load and an unprecedented peacetime budget deficit have heightened long-term fiscal risks. Recent tariff hikes represent a record-breaking tax increase, which is a significant headwind for the economy. Additionally, persistent inflation and tepid wage growth have negatively impacted most Americans. Currently, economic strength relies overwhelmingly on three pillars: outsized government deficits, consumption concentrated among the top 10% of households, and a historic surge in AI-related capital spending. In our view, none of these factors is sustainable, and we expect disappointing economic growth in the future.

Stock Market Outlook:

We believe the stock market offers a poor risk-reward. Stocks are extremely overvalued, concentration risk remains elevated, as a handful of mega-cap stocks dominate index performance, while underlying market breadth is weak. The S&P 500’s recent surge to an all-time high was primarily fueled by the Federal Reserve’s dovish pivot and the surge in AI-driven capital expenditures.

In our assessment, the market has fully discounted aggressive Fed rate cuts (0.75% this year and 0.70% next year), making it unlikely that actual easing will drive additional upside for stocks. Likewise, the scale of recently announced AI deals is so large—both in terms of capital and energy demands—that incremental announcements should have less impact on equity prices and increasingly highlight the improbability of the current AI infrastructure buildout. As a result, the risk of disappointment remains high, and any negative surprise in monetary policy or AI spending will lead to a sharp market correction.

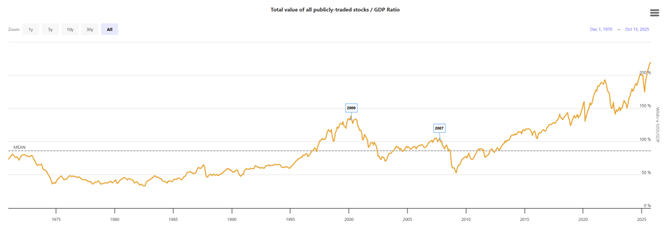

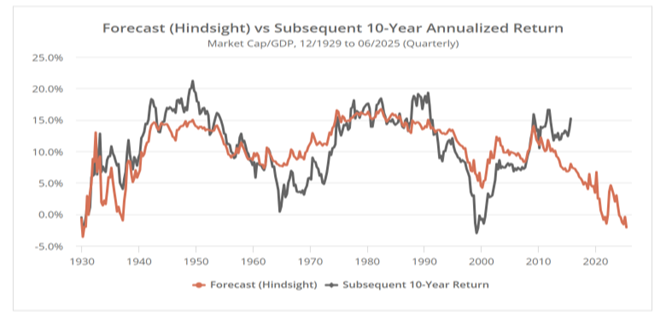

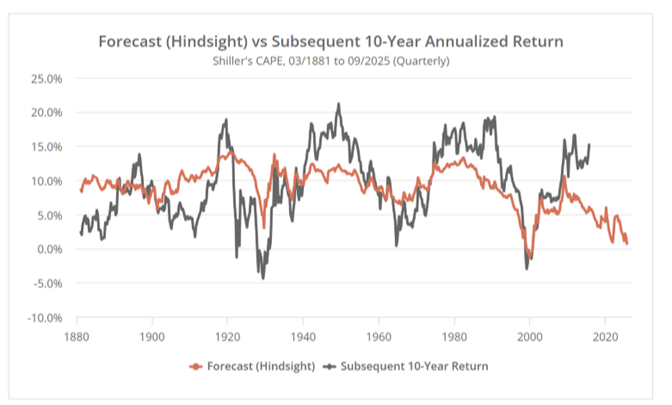

As value investors, we believe that the price you pay most accurately determines your return on investment. While valuation models exhibit little predictive power over the short term, they correlate strongly with long-term returns over ten years or more. Two robust long-term valuation models—Market Value to GDP and Shiller’s CAPE—indicate that the S&P 500 is projected to deliver annual returns between -2.1% and 0.7% over the next decade. Given that 10-year Treasury Inflation-Protected Securities (TIPS) currently yield a real return of 1.76%, equities are substantially overvalued and present an unattractive risk premium.

Market Value to GDP – “Still, it is probably the best single measure of where valuations stand at any given moment.” –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks are more than 100% higher than their historical average level and more expensive than during the 2000 technology bubble. Over the next ten years, the model forecasts an annual return for the S&P 500 of -2.1%.

Source: Longtermtrends.com, Allocate Smartly

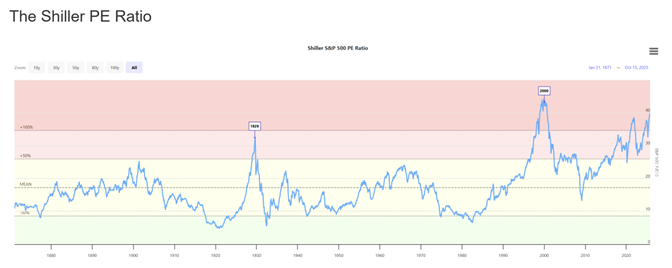

Shiller’s CAPE (a valuation measure that smooths out cyclical earnings fluctuations) indicates that stocks are more than 90% above their long-term average, and the 10-year expected return is about 2.5% per annum. Since the 10-year Treasury Inflation Protected Securities (TIPS) yield a real return of 1.76%, the S&P 500 has an inadequate risk premium. Over the next ten years, the model forecasts an annual return for the S&P 500 of 0.7%.

Source: Longtermtrends.com, Allocate Smartly

While the S&P 500’s valuation remains elevated, its vulnerability is amplified by concentration risk: the “Magnificent Seven” mega-cap tech stocks now comprise approximately 36% of the index’s market capitalization. Driven largely by AI-fueled capital spending, these overvalued stocks offer limited diversification. Should AI investment slow or fail to meet lofty expectations, the S&P 500 will face significant downside risk.

Although many investors consider these mega-cap tech stocks “blue chips,” they underestimate their volatility. For example, during the 2022 inflation surge—when U.S. headline inflation reached 9% and the broader market declined—the Magnificent Seven stocks fell by approximately 45%.

So far in 2025, the S&P 500 has gained roughly 13.3%, whereas the S&P 500 equal-weight index has risen only 7.3%, illustrating the extent to which recent gains are concentrated in a handful of stocks. While this dominance has recently bolstered returns, if the AI-driven rally were to stall or reverse, the lack of diversification would leave the S&P 500 acutely vulnerable to a sharp correction.

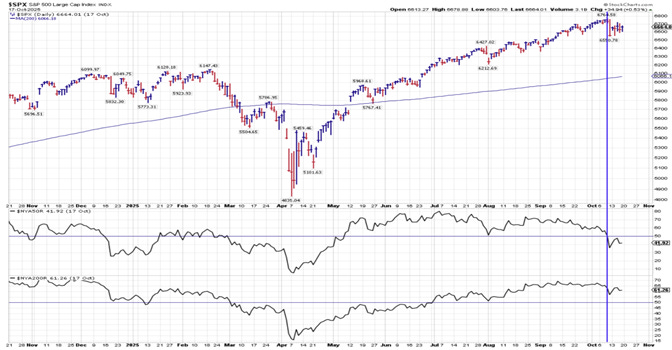

Finally, while the S&P 500 reached an all-time high on October 9th, market breadth was poor. Only 50.3% of NYSE stocks were above their 50-day moving average, and only 63.1% were above their 200-day moving average. Also, the economically sensitive regional bank and transportation indexes have not made a new high in several years. The continued underperformance of these key cyclical sectors signals underlying weakness and suggests that the overall economy and stock market may not be as healthy as headline indices imply.

While the S&P 500 reached an all-time high on October 9th, 37% of NYSE stocks were below their 200-day moving average and in a bear market. Weak market breadth is often a sign of impending market weakness.

Source:Stockmarketcharts.com

While the S&P 500 reached an all-time high on October 9th, economically sensitive indexes—such as the Regional Bank Index and the Dow Jones Transportation Average—have not made new highs in several years. The continued underperformance of these key cyclical sectors signals underlying weakness and suggests that the overall economy and stock market may not be as healthy as headline indices imply.

Source:Stockmarketcharts.com

Finally, gold—the ultimate safe haven—has surged more than 60% year-to-date, marking its strongest annual gain in over four decades. In fact, the metal soared by over 30% after the Federal Reserve’s August 22nd Jackson Hole meeting, when officials signaled diminished concern about inflation and an increased willingness to lower interest rates to support the labor market. This dovish shift heightened economic uncertainty, driving investors toward the safety of gold, which is traditionally sought during periods of heightened risk and waning confidence in financial markets. In our view, gold’s strength is the clearest sign that economic and stock market risks are elevated.

Gold surged by over 30% following the Federal Reserve’s August Jackson Hole meeting, when officials signaled less concern about inflation and a greater willingness to reduce interest rates in support of the labor market. This dovish policy pivot heightened economic uncertainty, prompting investors to seek the safety of gold, which is traditionally favored during periods of elevated risk and diminished confidence in financial markets.

Source:Stockmarketcharts.com

In summary, stocks currently present a poor risk-reward as they are widely overbought and overvalued, with weak market breadth masked by AI-driven mania. Gold’s 60% rally this year is a clear signal that economic and market risks are elevated. The S&P 500’s heavy concentration in mega-cap technology stocks makes it especially vulnerable to a correction if the AI boom fades. In this environment, we expect international equities, value stocks, and real assets to outperform the S&P 500.

Our Model Portfolio Review:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark’s historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of the rate of change for economic growth and inflation. This enables us to strategically position our portfolio to perform well in all economic environments.

In our view, stocks are priced for perfection. Investors are overlooking the structural issues of excessive debt, a $1.8 trillion budget deficit, and inflation that is significantly higher than the Fed’s 2% target. Even a weak labor market is considered a positive because it allows the Fed to ignore inflation and aggressively cut interest rates. Moreover, the full economic consequences of the recent tariffs— representing a significant tax increase exceeding 1.2% of GDP—have yet to be fully realized. We are concerned that the excitement about the dovish Fed and the AI mania are masking a weak economy, and if the AI capital spending boom slows from its torrid pace or the Fed is unable to stimulate growth, the economy and stocks are at risk.

We continue to maintain an underweight position in equities, particularly within the technology sector, while our bond exposure has little duration risk. Our allocation to international stocks, gold, and other precious metals provides economic balance and diversification, which we believe positions the portfolio to perform well in a period of economic uncertainty.

We plan to maintain a highly diversified and balanced asset allocation until economic uncertainty diminishes and equities present a more favorable risk-reward opportunity.

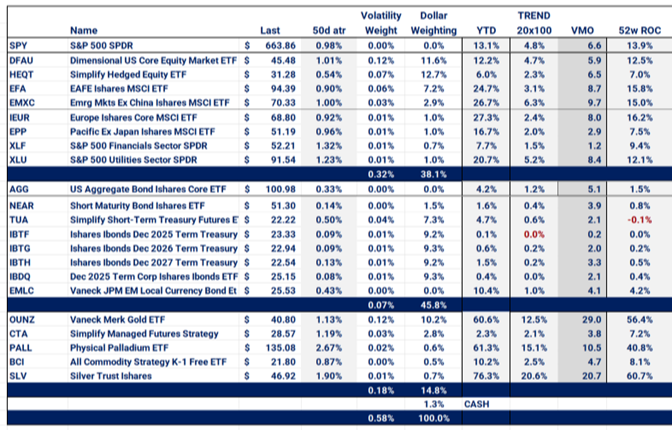

Current Risk-Weighted Portfolio

Our portfolio’s risk level (annualized volatility) is 9.2%.

Our 60\40 benchmark has a historic risk level of 10.7%, and its current risk level is 11.6%.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed.

All investments contain risk.

All information disclosed in this statement is accurate and complete to the best of our knowledge. Past performance is no guarantee of future results, and there is no assurance that the firm or client’s investment objectives will be achieved.

Thanks for reading The Manley Market Memo! Subscribe for free to receive new posts and support my work.

Your analysis of the three pillars supporting the economy - government deficits, top 10% consumption, and AI capital spending - is quite sobering. The comparison to dot-com era valuations combined with weak market breadth definitly suggests caution is warranted. I appreciate the emphasis on economic balance through international equities and real assets rather than following the crowd into overvalued mega-cap tech stocks.

Excellent deep dive into the current market dynamics! Your point about AI capital spending accounting for 92% of GDP growth in early 2025 is particularly striking. The comparison to past investment bubbles is spot-on—excessive building driven by overestimated demand is a classic pattern. The fact that gold has surged 60% this year while stocks hit new highs is indeed a powerful contrarian signal that somthing is off. Your analysis of the concentration risk in the Magnificent Seven is also well-articulated.