The Manley Macro Memo

We are in a high risk period and stocks offer a poor risk-reward -- especially relative to a 5.5% risk-free rate.

Summary

Financial markets in Q3 2023 were volatile, with stocks and bonds posting negative returns. Hawkish Federal Reserve rhetoric, surging energy prices, and an unexpected flood of new Treasury bond issuance due to the $2 trillion budget deficit led to a fear that interest rates would remain higher for longer to quell inflation. These concerns drove the 10-year U.S. Treasury bond yield up 0.80% to 4.6% at the end of the third quarter -- its highest level in 16 years.

Higher interest rates and increased economic uncertainty pressured the equity markets in the third quarter. The S&P 500 index of U.S. large-cap stocks declined 3.3% for the quarter, while the Russell 2000 index of small-cap stocks fell 5.5%. Global stocks also struggled, with the MSCI EAFE and the MSCI Emerging Market index declining 6.1% and 5.3%, respectively. Oil surged by 27% in Q3 as Saudi Arabia and Russia announced they would continue their oil production cut of 1.3 million barrels per day through 2023.

The Federal Reserve increased interest rates at its most aggressive pace in forty years to fight inflation. Most Fed tightening cycles led to a recession and a credit event. While the Fed attempts to slow the economy to curb inflation, government deficit spending surged this year. Although massive government spending may delay the recession, it thwarts the Fed's effort to curb inflation and adds to our long-term structural imbalances. Also, the leading indicators and the credit-sensitive sectors of the economy indicate that a recession is likely. In this uncertain economic environment, stocks offer a very poor risk-reward because they are overvalued, and corporate profits are at risk as higher interest rates and tighter lending conditions push the economy toward recession.

Despite last October's market bottom, the stock market remains in a bear market, and the bubble in the mega-cap technology stocks is masking the market's underlying weakness. Most stocks -- including the "Magnificient Seven" -- have lost value over the past twenty-two months. We believe the Q3 weakness in the stock and bond market will continue until the economy is in recession, stocks offer a favorable risk-reward, and the Federal Reserve is cutting interest rates to stimulate the economy.

We are in a high-risk environment and think a 5% risk-free rate is very attractive. We are underweight stocks, positioned in the market's defensive sectors, and have a significant investment in a 3-year U.S. Treasury ladder yielding more than 5%. Our portfolio is well positioned to provide a solid return until the economic headwinds are reduced and stocks offer better risk-reward.

Q3 Market Review:

Financial markets in Q3 2023 were volatile, with stocks and bonds both posting negative returns. Hawkish Federal Reserve rhetoric, a nearly $2 trillion 2023 budget deficit, and surging oil prices led to a fear that interest rates would remain higher for longer to quell inflation. These concerns drove the 10-year U.S. Treasury bond yield from 3.8% to 4.6% at the end of the third quarter, which is its highest level in 16 years.

Higher interest rates and increased economic uncertainty pressured the equity markets. The S&P 500 index of U.S. large-cap stocks declined 3.3% for the quarter, while the Russell 2000 index of small-cap stocks fell 5.5%. Global stocks also struggled, with the MSCI EAFE and the MSCI Emerging Market index declining 6.1% and 5.3%, respectively. Oil surged by 27% in Q3 as Saudi Arabia and Russia announced they would continue their oil production cut of 1.3 million barrels per day through 2023.

The main driver of asset prices in Q3 was rising long-term bond yields. On July 26th, the Federal Reserve increased short-term interest rates to 5.5%, while the 10-year U.S. Treasury note yielded 3.85%. Wall Street pundits believed the hiking cycle was nearly complete, and the Fed would reduce interest rates by 1.00% in 2024. Instead, the Fed indicated that it planned to keep interest rates "higher for longer," and a 1.00% interest rate reduction was unlikely in 2024. In addition to the Fed's hawkish rhetoric, long-term interest rates jumped to nearly 4.9% because the labor market remained resilient, oil surged, and the $2 trillion budget deficit led to an unexpected flood of new Treasury bond issuance.

After three quarters, most stocks are essentially flat for 2023 after a sharp decline in 2022. The S&P 500 is having a good year because its performance is dominated by the "Magnificent Seven" (seven mega-cap technology stocks -- Apple, Microsoft, Google, Amazon, Meta, Nvidia, and Tesla) that comprise approximately 30% of the index and have contributed about 90% of the index's return this year. We believe the equal-weighted S&P 500 and the small-cap Russell 2000, which appreciated only 1.7% and 2.5% during the third quarter, are more diversified indexes that better indicate the market's struggle this year.

While many pundits believe stocks are in a new bull market, we think the market's performance since January 2022 indicates that stocks remain in a bear market, and the bubble in the "Magnificent Seven" is masking the broad-based weakness in the equity market this year. Also, new bull markets are typically led by economically sensitive small-cap and financial stocks – not mega-cap technology stocks.

Since the bear market began in January 2022, all major stock averages have declined, and even the "Magnificent Seven" has lost value, notwithstanding an epic rally this year. Despite being great franchises (many having monopolistic characteristics) with strong balance sheets and robust cash flows, the "Magnificent Seven" dropped on average 46.8% last year – significantly worse than the S&P 500 and the Russell 1000 Growth Index. While the "Magnificent Seven" has had a great year so far in 2023, they were very oversold after a terrible 2022. And their extreme valuations make them vulnerable in a rising interest rate environment (see table below).

In addition to benefiting from an extreme oversold condition, we believe that the significant passive flows into the market can explain the "Magnificent Seven's" outperformance. Over 45% of the S&P 500 is owned by passive investment funds that buy or sell stocks based on investment flows (contributions and redemptions), not fundamental change. As passive investing has grown significantly over the past few decades, the S&P 500 has become more inelastic (less stock is available to buy or sell due to the passive holders), and its price in the short-term is increasingly a function of naïve investment flows instead of the fundamentals.

The "Magnificent Seven" are nearly 30% of the S&P 500 (see table above), so they receive $30 out of every $100 invested in the S&P 500. Since passive investing's market share has created an inelastic market, these flows, coupled with corporate buybacks, have an outsized impact on the value of these companies – i.e., the company's value increases by a significant multiple of the passive inflow.

In addition to the large passive flows and buybacks, the mega-cap stocks benefitted this year from quantitative investment strategies (CTA's, Risk Parity, Short Volatility, and 0 DTE options speculation) that invest based on volatility, not the fundamentals. These systematic strategies aggressively bought the S&P 500 this year, not because the fundamentals improved but because the VIX (implied volatility) fell from 21.7 at the beginning of the year to 12.7 in mid-September. While these passive and systematic flows have had a virtuous impact on the S&P 500, especially the "Magnificent Seven," the flows can reverse (particularly during a recession), leading to a negative feedback loop of selling into an inelastic market.

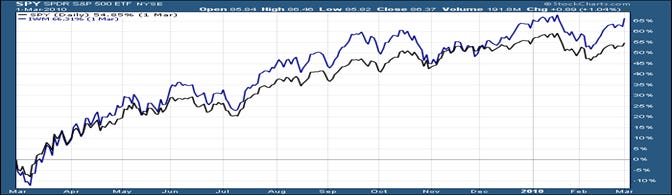

The stock market bottomed a year ago on October 13th. Over the last twelve months, the small-cap Russell 2000 and the S&P Financials sectors have declined by more than 2%. Typically, these economically sensitive stocks are the leaders in the first year of a bull market. Instead, we believe their weak performance after a sharp decline last in 2022 indicates that the economy and the stock markets are at risk as sharply higher interest pushes the economy toward recession.

New bull markets are characterized by a change in leadership and outperformance by the small-cap sector. The Russell 2000 outperformed the S&P 500 by 27.2%, 11.3%, and 30% during the twelve months after the 2003, 2009, and 2020 bear markets ended.

The S&P 500 bottomed out last October and has risen by 22.9%, while the Russell 2000 has increased by only 3.4%. The small cap's poor relative performance indicates that this is a bear market rally, not a new cyclical bull market.

In Sum:

Despite bottoming a year ago, the stock market remains in a bear market, and the bubble in the mega-cap technology stocks is masking the market's underlying weakness. The stock market offers a poor risk-reward, especially relative to the 5.5% risk-free rate. We believe the Q3 weakness in the stock and bond market will continue until the economy is in recession, stocks offer a favorable risk-reward, and the Federal Reserve is cutting interest rates to stimulate the economy.

Our Model Portfolio Review:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

We remain defensively positioned because stocks offer a poor risk-reward, and we expect the sharp increase in interest rates over the past eighteen months will push the economy into recession. Also, the tragic events in Israel and the ongoing war in Ukraine have significantly increased the geopolitical risks during this period of economic uncertainty.

To preserve capital in this challenging economic environment, we are underweight stocks relative to our 60/40 benchmark and overweighting the market's defensive sectors (healthcare, staples, and utilities), which typically outperform during periods of weak economic growth.

We have significant fixed-income exposure in shorter-term U.S. Treasury notes (three years and less). Short-term Treasuries are attractive because they have a high risk-free yield, which pays us more than 5% to wait until there is less economic uncertainty and stocks offer a favorable risk-reward. Also, we are invested in gold – the ultimate safe haven – which should perform well in periods of geopolitical stress and recessions.

As long-term value investors, we focus on valuation and the leading economic indicators to estimate the economy's likely path and corporate profits. Economic growth is declining, and we have been in a profit recession since the fourth quarter of 2022. Interest rates have risen sharply over the past eighteen months, and the economy's leading indicators and credit-sensitive sectors indicate a recession is likely. While massive government deficit spending this year has supported the economy, it is delaying the inevitable recession.

In Sum

We are in a high-risk period. Economic and geopolitical uncertainty make risk assets unattractive, especially relative to the 5.5% risk-free rate. Despite the "Magnificent Seven's" large rally this year, most stocks have performed poorly after a sharp decline last in 2022.

As the economy slows, our defensive equity investments and gold should outperform, while our large 3-year Treasury ladder pays us a solid return to wait for a better environment. Above all, during this challenging economic environment, we will focus on preserving capital until the economic and geopolitical headwinds have dissipated and the stock market offers a better risk reward.

Current Risk-Weighted Model Portfolio:

Our portfolio's risk level (annualized volatility) is 7.0%, which is less than our 60\40 benchmark's risk level of 14.2%.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

Market Outlook

Stocks offer a very poor risk-reward, especially compared to a risk-free rate of 5.5%. Despite a sharp increase in interest rates over the past eighteen months, the S&P 500's valuation has remained elevated. Additionally, corporate earnings appear at risk as the economy slows and profit margins regress to an average level.

Since the "Great Financial Crisis of 2008," the Federal Reserve set interest rates at 0%, well below inflation, and printed money to buy long-term bonds to stimulate the economy. Because asset values are the present value of future cash flows, changes in interest rates make future cash flows more or less valuable, positively or negatively affecting the asset's price.

Because the Fed pushed interest rates to an artificially low level, cash flows became more valuable, and asset values increased dramatically. In addition to inflating stock values, the Fed's easy money policy favored borrowers at the expense of savers, which led to an excessive corporate and government debt burden and created great wealth inequality.

After fourteen years, the Fed reversed its profligate monetary policy by allowing real interest rates to return to normal. Historically, short-term interest rates provided a small 0.30% return over inflation. Longer-term bonds and stocks provided a risk premium over short-term interest rates to compensate investors for taking more risk. The QE era disrupted these relationships because the Fed set interest rates well below inflation – which punished savers and subsidized borrowers. While real interest rates have normalized, the stock market's Equity Risk Premium remains at the artificial QE-era level.

Last March, the Fed ended its profligate monetary policy after inflation surged to a forty-year high. The Fed raised real interest rates to the highest level in 14 years to combat inflation. With positive real rates, the Fed no longer punishes savers and subsidizes borrowers.

Historically, short-term interest rates provided a small 0.30% return over inflation, and longer-term bonds and stocks provided a premium over short-term interest rates to compensate investors for taking more risk. The QE era disrupted these relationships because the Fed set interest rates well below inflation, which led to many structural imbalances and inflation at a forty-year high.

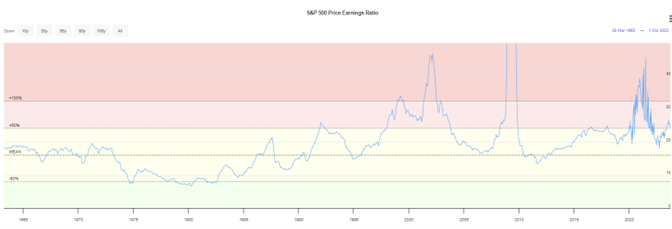

While interest rates have adjusted to provide an attractive return over inflation, stock valuations remain elevated -- especially relative to the fixed-income market. Since the Fed began raising interest rates last March, short and long-term interest rates are 5.2% and 2.5% higher and offer a positive real return. Despite sharply higher interest rates, the S&P 500 P/E multiple is unchanged, and its Equity Risk Premium (earnings yield minus Fed Funds) is negative. According to this measure, an investor will receive a lower return investing in stocks than being in cash.

Currently, the S&P 500 sells at 20.8 times trailing earnings. At this level, stocks discount a return to artificially low-interest rates, which is unlikely because inflation is around 4%. If inflation and government bond yields remain near their historical averages of 2.9% and 5.2%, the stock market should sell at its long-term average of 16, leading to a 23.8% decline.

Despite sharply higher interest rates and a normalization of real rates, stocks remain overvalued and pricing in a return to a low-rate environment. We expect stocks to decline as valuation levels regress to a normal level.

Source: Longtermtrends

While we believe the stock market could fall sharply as valuations adjust to a positive real interest rate environment, we also remain concerned that earnings are vulnerable as the economy approaches recession and profit margins decline from an elevated level.

To fight inflation, the Fed raised interest rates aggressively and reduced the size of its balance sheet, which led to an inverted yield curve and a collapse in the money supply's growth rate. These tighter monetary conditions drove the leading, credit-sensitive sectors of the economy into recession. Additionally, Gross Domestic Income (a coincident economic measure) is flat, and the financial sector is under stress because of the massive unrealized losses in their bond portfolios.

Many ebullient Wall Street pundits have pushed the narrative that this time is different and we are headed to a soft or no landing. They point to a robust labor market and the fact that we aren't in recession yet. In our view, the recession is still on pace relative to the historic lead times of the leading indicators. Also, this year's unprecedented amount of government deficit spending has propped up the economy and may have delayed the recession while adding to our structural imbalances.

Since 1968, every time short-term rates yielded more than long-term rates, a recession occurred with an average lead time of 14 months. One of the key explanations behind an inverted yield curve's ability to forecast the last eight recessions lies in the challenges it creates for banks and financial institutions, resulting in reduced lending, which leads to slower economic growth. A flattening yield curve after inversion indicates that the recession is imminent.

While recessions occur on average 14 months after the yield curve inverts, the timing is highly variable. Many pundits point to the resilient labor market as a sign that we will avoid recession. As the chart below shows, the labor market is a lagging indicator that typically doesn't deteriorate until a year after the yield curve inverts.

In addition to the yield curve, another accurate indicator of the economy is the Conference Board's Leading Economic Index. The LEI is currently forecasting a recession. According to famed economist David Rosenburg, the LEI has had a perfect record of forecasting recessions since 1959.

Milton Freidman famously said:" inflation is always and everywhere a monetary phenomenon." The Fed ignored the surging money supply, and inflation rose to a 40-year high. Today, the money supply's growth rate has collapsed, and economic growth and inflation will continue to decline.

There are two measures of economic growth – Gross Domestic Product and Gross Domestic Income. GDP measures the total value of all final goods and services produced each year, while GDI represents the total income generated by the factors of production (such as labor and capital). Although real GDP increased by 2.4% over the past year, real GDI rose by only 0.2%. In our view, it is impossible to rule out a recession when real GDI is not growing, and the full impact of the Fed's rate hikes and the reduction in credit growth due to the regional banking crisis has not yet impacted the economy.

Real Gross Income is a coincident economic indicator that hasn't grown over the past year and indicates that the economy may already be in recession.

An unintended consequence of the Fed's interest rate hiking cycle is massive unrealized bank balance sheet losses. These losses have impaired their lending ability as they focus on repairing their balance sheet. Since the bond market declined sharply since Q2, the record losses below are likely understated.

Banks are lending less because of the inverted yield curve and the significant unrealized losses on their balance sheet. According to Apollo, bank lending standards are already at recessionary levels.

It is disconcerting that the government is aggressively spending while the Fed is trying to slow the economy to curb inflation. Over the past twelve months, real government spending and investment grew at a 4.1% rate, and the budget deficit reached $2 trillion, which is 7.4% of GDP. While government spending may delay the recession, it thwarts the Fed's effort to curb inflation and adds to our long-term structural imbalances.

The Treasury Department failed to extend the term structure of our national debt when the 10-year Treasury bond fell below 1% after the pandemic. In fiscal 2023, the government's largest spending increase was the cost to service the debt. According to the CBO, the Treasury spent $711 billion on net interest payments this year, which was a 33% increase from fiscal 2022. If interest rates remain around 5%, interest expense will surge again next year since the current average interest rate on our $33 trillion debt is only 2.9%.

While real GDP and real GDI grew 2.2% and 0.2% over the past year, real government spending and investing surged by 4.1%.

In the last twelve months, the government's budget deficit reached $2 trillion, which is equal to 7.4% of GDP. This massive government spending hurts the Fed's effort to slow inflation and adds to our long-term structural imbalances.

Despite the unemployment rate at a 50-year low, the budget deficit is 7.4% of GDP, which is greater than most recessionary periods. While the large government spending contributed to economic growth, it also spurred inflation. Since budget deficits increase significantly during a recession, weak growth, and high interest rates will place the U.S. in a vulnerable position as we try to service our exploding debt burden.

In Sum:

The Federal Reserve increased interest rates at its most aggressive pace in forty years to fight inflation. Most Fed tightening cycles lead to a recession and a credit event. While the government's massive deficit spending this year may have delayed the recession, the leading indicators and the credit-sensitive sectors of the economy indicate that a recession is likely.

In this uncertain economic environment, stocks offer a very poor risk-reward. Stocks are overvalued and do not reflect the positive real rate environment. Also, corporate profits are at risk as higher interest rates and tighter lending conditions push the economy toward recession, and elevated profit margins regress to an average level. We believe it is prudent to underweight stock and invest in a three-year government bond ladder that yields more than 5% until the economic uncertainty diminishes and stocks offer a favorable risk-reward.

Thank you for reading The Manley Market Memo.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed. All investments contain risk.