The Manley Macro Memo

The S&P 500 is priced for perfection despite potential short-term risks from transitioning to a private sector-driven economy, uncertain tariffs and deportation policies, and terming out our debt

Executive Summary:

Equity markets had a mixed performance in Q4 2024. The S&P 500 rose 2.5%, but the equal-weight S&P 500 and S&P 600 Small-cap indexes fell by 1.9% and 0.5%. Foreign markets also struggled, with the MSCI EAFE International down 8.4% and the MSCI Emerging Markets index dropping 7.3%. The weak performance was due to rising interest rates and a strong dollar. Despite the Federal Reserve cutting short-term rates by 1.00% in Q4, long-term rates increased sharply, indicating another potential monetary policy error by the Fed.

In 2024, major stock markets performed well. The S&P 500 increased by 23.3%, mainly driven by the "Magnificent Seven" tech stocks (Apple, Nvidia, Microsoft, Amazon, Google, Meta, and Tesla), which surged 67% and contributed 53% of the index's gains. Nvidia alone accounted for over 20% of the S&P 500's performance. The equal-weight S&P 500 and S&P 600 Small-cap indexes rose by 12.8% and 8.5%, respectively. MSCI EAFE International increased 3.5%, and MSCI Emerging Markets gained 6.5%.

The U.S. economy grew by an estimated 3%, and corporate profits rose 9.4% last year, with unemployment at 4.1% and core inflation at 3.25%. Growth was driven by investments in data centers, AI, and government spending from the CHIPS Act, Inflation Reduction Act, and Infrastructure Act. Unfortunately, growth relied on unsustainable deficit spending and the suppression of long-term interest rates. The new administration aims to reduce the deficit to 3% through spending cuts and boost economic growth via deregulation and low taxes. Additionally, they plan to combat inflation by increasing energy production by 23%. Additionally, President Trump proposes deporting illegal immigrants and imposing tariffs to reduce the trade deficit and increase domestic investment.

Reducing taxes, deregulating industries, incentivizing capital investment, and decreasing government spending will boost economic growth, lower inflation, and improve living standards over the long run. However, transitioning to a private sector-driven economy involves challenges, with potential short-term risks from tariffs, deportation policies, and terming out our national debt.

Despite significant short-term economic uncertainty, the S&P 500 is substantially overvalued and lacks diversification since the Mag-7 constitutes 33% of the index. To outperform and preserve capital during this high-risk period, we maintain a diversified portfolio that is underweight equities relative to our benchmark, and approximately 50% of the portfolio is allocated to short-duration bonds, yielding about 5.0%. We are underweighting the overvalued growth stocks and overweighing the value and small-cap sectors, which are relatively inexpensive. Additionally, we hold investments in gold, considered the ultimate safe haven, which has performed very well due to geopolitical tensions, economic uncertainty, and central bank actions. We intend to maintain a significant position in short-term fixed-income assets until economic conditions stabilize and equities offer a more favorable risk-reward profile.

2024 Market Review:

Equity markets finished 2024 with a mixed fourth-quarter performance. While the S&P 500 rallied by 2.5%, most major averages declined in Q4. The equal-weight S&P 500 and the S&P 600 Small-cap indexes declined by 1.9% and 0.5%, respectively. Foreign markets performed poorly—the MSCI EAFE International dropped by 8.4%, and the MSCI Emerging Markets index fell by 7.3%.

The primary driver of equity markets' weak Q4 performance was the sharp increase in interest rates and a strong dollar. Despite the Federal Reserve cutting short-term interest rates by 1.00% in the fourth quarter, long-term interest rates increased sharply, signaling that the Fed may have made another monetary mistake. The U.S. 2-year Treasury yield rose by 0.60% to 4.25%, while the U.S. 10-year Treasury yield jumped by 0.79% to 4.58% in Q4. In this period of rising interest rates, Gold and Oil increased by 4.5% and 5.2%, respectively.

As the table below indicates, the S&P 500's 2.1% increase was primarily due to a 3.5% increase in valuation since earnings estimates fell by 1.4%. The increase in the S&P 500's valuation is surprising, given the sharp rise in interest rates.

The major stock markets performed well in 2024, as the economy grew at an estimated 3%, unemployment remained at a historically low 4.1%, and core inflation fell from 3.9% to 3.25%. According to S&P Dow Jones, corporate profits grew by an estimated 9.4%, while revenue grew by 5.1%. The primary economic drivers in 2024 were data center and AI capital spending and government spending from the CHIPS Act, the Inflation Reduction Act, and the Infrastructure Act.

While the S&P 500 increased by 23.3%, most major averages had solid but less robust gains. The equal-weight S&P 500 and the S&P 600 Small-cap indexes increased by 12.8% and 8.5%, respectively. The MSCI EAFE International rose 3.5%, and the MSCI Emerging Markets indexes increased 6.5%.

The S&P 500's significant 2024 outperformance versus the other major equity averages was driven by the 31% concentration in the "Magnificent Seven" mega-cap technology stocks (Apple, Nvidia, Microsoft, Amazon, Google, Meta, and Tesla) that benefited from AI hype. The Magnificent Seven appreciated 67% and contributed 53% of the S&P 500's appreciation this year. NVIDIA, the technology company that designs AI chips, alone accounted for over 20% of the S&P 500 performance in 2024.

As the table below shows, much of the S&P 500's appreciation last year was driven by higher valuation. While the S&P rallied sharply this year, 2024 earnings grew by 9.3% over the past year, so the S&P 500's 23.3% increase was primarily due to a 12.9% increase in valuation. This valuation expansion is surprising since the 10-year bond rose 0.72% in 2024.

Economic Outlook

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of the rate of change for economic growth and inflation. This enables us to strategically position our portfolio to perform well in all economic environments.

Despite high interest rates, an inverted yield curve, and a manufacturing sector recession, the economy grew at its 50-year median growth rate of 3%, and unemployment remained at a subdued 4.1%. While the economy remained robust, inflation declined from 3.9% at the beginning of the year to 3.25% but remains above the Federal Reserve's 2% inflation target. The primary economic drivers in 2024 were data center and AI capital spending and government spending from the CHIPS Act, the Inflation Reduction Act, and the Infrastructure Act.

Although the economic headline numbers look solid, growth was driven by unsustainable deficit spending and structural imbalances. Since the Pandemic, economic growth has been led by government spending, large budget deficits, and a sharp increase in national debt. Since Q1 2000, government spending has increased by 45% to $7.05 trillion, while our debt burden has increased by 52.7% to $35.46 trillion, or 120% of GDP. Over this period, the real economy grew by only 13%.

Over the past 50 years, the median budget deficit was 2.8% of GDP. Government spending averaged about 20.3%, while government revenue averaged approximately 17.5%. In fiscal 2024, the budget deficit was almost $2 trillion or 6.8% of GDP, despite a very low 4.1% unemployment level. Since the government's $5.13 trillion revenue was equal to 17.5% of GDP, excess government spending equal to 24% of GDP was responsible for the large deficit.

To accommodate this profligate spending, the Federal Reserve grew its balance sheet (printed money to buy Treasury bonds) by 64%. The massive government spending and expansion of the Fed's balance sheet led to a sharp 22.5% inflation increase.

Since the Pandemic, government spending has increased by 45% and national debt by 53%, yet the real economy grew by only 13%. To accommodate this profligate spending, the Federal Reserve bought bonds, which grew its balance sheet by 64%. Unfortunately, this excessive spending and money printing led to a 22.5% increase in inflation.

Source: FRED

In addition to the unprecedented peacetime budget deficit, the economy was stimulated by artificially low long-term interest rates. Typically, the U.S. Treasury finances our debt with 15 to 20% short-term T-bills and the remainder in long-term notes and bonds. Since October 2023, Treasury Secretary Yellen issued about 70% bills to finance the deficit—which is surprising since the yield curve was inverted and issuing short-term debt was more costly.

By reducing the amount of long-term debt issued from approximately 80% to 30% of the deficit, long-term interest rates plunged by 1.2% in two months as the supply of long-term debt was suppressed. The 10-year U.S. Treasury yield fell from 5% in October 2023 to 3.8% in December 2023. Lower long-term interest rates (typically set by the financial markets) stimulate the economy and push stocks higher (since stock prices are based on the value of future cash flows, when long-term interest rates decline, stock prices rise because future earnings are worth more today, increasing the stock's value).

Source: Stockcharts.com

In addition to incurring higher interest expenses, the Treasury's decision to suppress long-term interest rates affected the Federal Reserve's efforts to reduce inflation. In an election year, the Treasury apparently prioritized stimulating the economy and boosting asset prices instead of fighting inflation.

To fight inflation, the Fed raised interest rates by 5.5% and, through Quantitative Tightening ("QT"), reduced its balance sheet by $25 billion each month. Despite the QT, the liquidity in the financial system increased as reductions in the U.S. Treasury General account and the reverse repo market neutralized the Fed's shrinking balance sheet. Financial liquidity increased by $200 billion after the regional banking crisis of March 2023. This increase in excess liquidity pushed asset prices higher and kept inflation elevated above the Fed's target.

Despite the Fed's Quantitative Tightening Program to reduce its balance sheet and excess liquidity, a reduction in reverse repos and the Treasury's general account led to a $200 billion increase in financial liquidity after the regional banking crisis of March 2023.

Source: FRED

While the economy appears stable, the large budget deficit and its financing with short-term debt are unsustainable. The Trump administration's Treasury Secretary, Scott Bessent, plans to address these economic issues. He aims to reduce the budget deficit to 3% by cutting government spending and growing the economy by 3% through deregulation and low taxes. Additionally, to fight inflation and bring interest rates down, he wants to increase energy production by an equivalent of 3mm barrels per day (up 23%) through deregulation. Bessent has also acknowledged the need to fix the nation's balance sheet by terming out the debt and not relying so heavily on short-term funding.

In addition to these pro-growth measures, President Trump wants to deport illegals immigrants and place large tariffs on our trading partners to promote fair trade, reduce our trade deficit, and encourage investment and job creation in the U.S. Since the timing and magnitude of these policies are uncertain, they could have an adverse impact on the economy.

We believe low taxes, deregulation, and incentivizing capital investment, along with reduced government spending, will boost economic growth, lower inflation, and improve living standards. However, transitioning to a private sector-driven economy could be challenging, with uncertain tariff and deportation policies adding short-term risks. Furthermore, the timing of terming out our short-term debt may negatively affect long-term interest rates, the stock market, and the overall economy.

While we are confident that these policies are necessary and will work in the long term, the timing and magnitude of these changes could have an adverse short-term impact on the economy and/or lead to an increasing inflation rate.

Stock Market Outlook:

We believe that the stock market offers a poor long-term risk reward. The S&P 500 is significantly overvalued and lacks diversification because the Magnificent Seven represents nearly 35% of the index. While the stock market is priced for perfection, we believe the short-term economic risks are significant as policies are implemented to address the many structural imbalances.

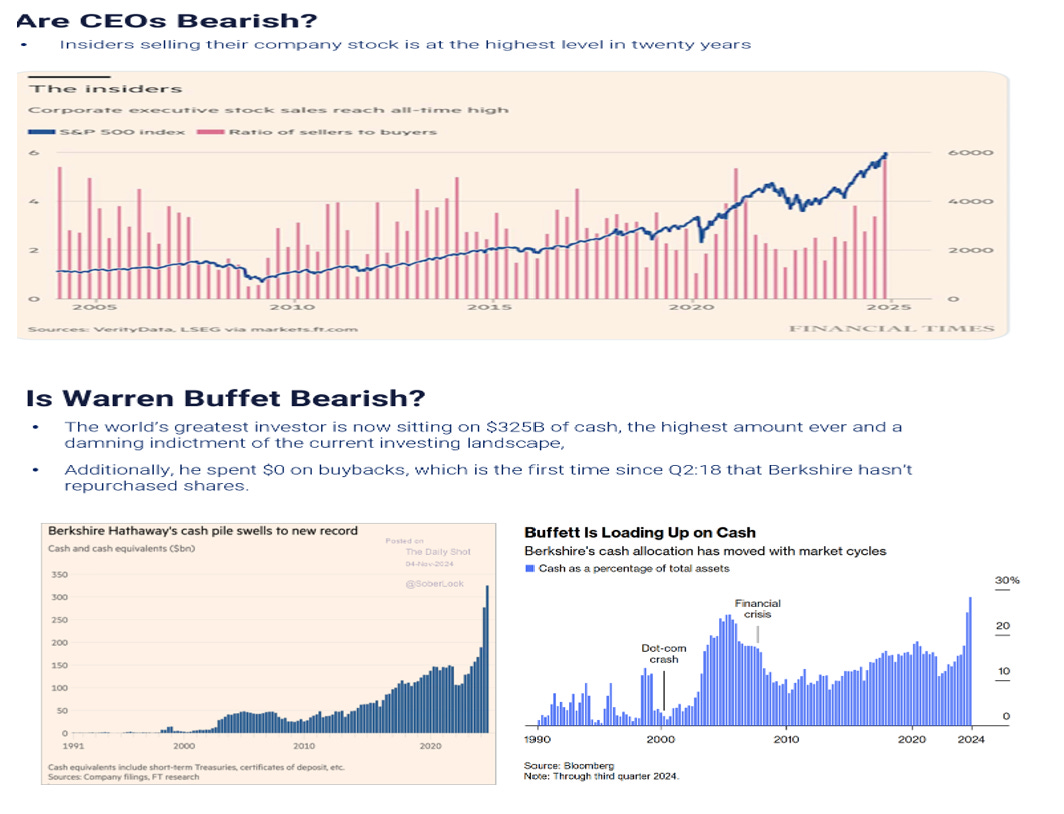

Furthermore, the loose monetary policies have resulted in speculative bubbles across various market sectors, such as AI, cryptocurrency, and quantum computing. Despite widespread investor enthusiasm, corporate insiders are divesting their shares, and prominent investor Warren Buffet has allocated $325 billion to Treasury bills rather than stocks.

Finally, the Mag-7 and the S&P 500 have greatly benefitted from the AI boom and the substantial investments in AI infrastructure. Recently, DeepSeek, a Chinese artificial intelligence firm, has released an open-source AI model that significantly outperforms current AI models at a fraction of the cost and investment. If this AI model proves legitimate, it may have commoditized existing AI models, which will negatively affect the capital expenditures driving these companies, and the Mag-7 and the S&P 500 would be vulnerable due to the hundreds of billions of dollars of malinvestment.

The S&P 500 increased by almost 60% in the past two years, marking its strongest two-year performance in twenty-five years. During this time, the Mag-7 stocks grew by an average of 268%, and these seven stocks now represent approximately 35% of the index. The heavy weight of these expensive technology stocks drove the S&P 500's valuation to a record high. Currently, the S&P 500 is significantly overvalued and lacks adequate diversification. For the first time since 2002, the equity risk premium is negative – i.e., the earnings yield of the S&P 500 is less than the 10-year U.S. Treasury bond.

Since the price paid for an investment is the best determinant of future returns, the extreme valuation of the S&P 500 is likely to result in poor long-term returns.

Market Value to GDP – "Still, it is probably the best single measure of where valuations stand at any given moment." –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks are more than 100% higher than their historical average level and more expensive than during the 2000 technology bubble.

Shiller's CAPE (a valuation measure that smooths out cyclical earnings fluctuations) indicates that stocks are more than 50% above their long-term average, and the 10-year expected return is about 2% per annum.

We believe the loose monetary conditions provided by the Fed and U.S. Treasury have led to bubbles in many market sectors -- AI, crypto, quantum computing, etc. For example, Dogecoin (DOGE) was created as a joke in 2013 and has grown into a digital coin with a value of $53 billion, down from its December peak of more than $70 billion. This meme coin with no supply constraint and limited use is worth as much as many blue-chip companies:

CVS Health Corporation

$ 68,646mm

FedEx Corporation

$ 65,822 mm

Target Corporation

$ 63,183 mm

Royal Caribbean Cruises Ltd.

$ 62,406 mm

Hilton Worldwide Holdings Inc.

$ 60,392 mm

MetLife Inc.

$ 59,569 mm

General Motors Company

$ 59,279 mm

While speculators have driven many stocks and crypto assets to specious valuations, corporate insiders are divesting their shares, and prominent investor Warren Buffet has allocated $325 billion to Treasury bills rather than stocks.

We are concerned that the S&P 500 lacks diversification and is priced for perfection while corporate insiders are selling and Warren Buffet is sitting on the sidelines with $325 billion in cash. We believe there is significant short-term economic uncertainty as policies are initiated to address the structural imbalances and inequality in the economy. Additionally, stocks are vulnerable as the two important drivers of asset prices – the Treasury's suppression of long-term rates and the excess liquidity provided by the declining reverse repo market and Treasury's general account – are poised to reverse and remove liquidity from the financial system.

Finally, the Mag-7 and S&P 500's strong performance over the past two years has been driven by AI hype and massive investments in AI infrastructure. Last week, Deep Seek, a Chinese AI firm, released an open-source AI model that outperforms current AI models at a significantly lower cost and was allegedly built in six months for less than $6mm. If proven legitimate (and not Chinese propaganda), this AI model could negatively impact future AI investments and disrupt mega-cap technology stocks due to their extreme valuation and potential malinvestment of hundreds of billions of dollars.

Our Model Portfolio Review:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

The current valuation of the S&P 500 indicates an unfavorable long-term risk-reward for investors. Additionally, the equity risk premium -- the additional compensation investors require for taking on higher-risk stocks compared to safer government bonds -- is negative for the first time since 2002, making stocks less attractive than U.S. Treasury bonds.

While stocks offer a poor long-term risk-reward, we believe there is significant economic uncertainty due to the unknown timing and magnitude of the proposed economic changes to fix the structural imbalances in the economy. We believe low taxes, deregulation, and incentivizing capital investment, along with reduced government spending, will boost economic growth, lower inflation, and improve living standards. However, transitioning to a private sector-driven economy could be challenging, with uncertain tariff and deportation policies adding short-term risks. Furthermore, the timing of terming out our short-term debt may negatively affect long-term interest rates, the stock market, and the overall economy.

Furthermore, artificial intelligence has significantly contributed to the outperformance of the S&P 500 over the past two years. If the economic theories supporting Deep Seek are accurate, the AI models in which U.S. technology companies have invested hundreds of billions of dollars have become commoditized. Consequently, the Mag-7 and the S&P 500 face potential risks as capital expenditures decrease and valuations return to their historical averages.

Due to short-term economic uncertainty and the equity market's poor risk-reward ratio, we remain cautious. To outperform our benchmark and preserve capital in this high-risk period, we maintain a diversified portfolio that is underweight equities relative to our benchmarks, amd 50% of the portfolio is invested in short-duration bonds that yield about 5.1%. We remain underweight the overvalued growth stocks and overweight the inexpensive value and small-cap sectors.

Finally, we are invested in gold – the ultimate safe haven – which is performing well due to geopolitical stress, economic uncertainty, and central bank ineptness. We plan to maintain a substantial position in short-term fixed-income assets until economic uncertainty diminishes and equities present a more favorable risk-reward opportunity.

Our portfolio's risk level (annualized volatility) is 8.6%, which is less than our 60\40 benchmark's historic risk level of 10.7%, and its current risk level of 12.7%.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed.

All investments contain risk.

Thanks for reading The Manley Market Memo! Subscribe for free to receive new posts and support my work.

Thanks for your thorough review and sharing of your portfolio.