The Manley Macro Memo

The S&P 500 offers a poor risk-reward since it is extremely overvalued and is no longer a diversified index since the Magnificent Seven mega-cap technology stocks represent a 31% weighting.

Executive Summary:

After a sharp 9.7% decline in early August, the equity rally continued during the third quarter, and the S&P 500 increased by 5.5%. After a weak first half of 2024, the broader market performed well in Q3, as the equal-weight S&P 500 and the Russell 2000 increased by 9.6% and 9.3%, respectively. While stocks rallied in the third quarter, interest rates declined sharply due to weak economic data and elevated geopolitical risk. The U.S. 2-year Treasury yield fell by 1.12% to 3.65%, while the U.S. 10-year Treasury yield dropped by 0.61% to 3.79%. Gold, the ultimate safe haven, jumped by 13.7% in the third quarter amid the volatility.

On September 18, the Federal Reserve reduced short-term interest rates by an unexpectedly large 0.50%. Since the Fed's jumbo rate cut and dovish rate projection, economic data has unexpectedly strengthened, and long-term bond yields rose sharply over concern that the Fed may have made another monetary mistake.

The economy has been in a deflationary environment for more than a year due to declining inflation and growth rates. We are concerned that the government's massive fiscal deficit and loose monetary conditions provided by the Fed could increase the inflation rate and push the economy into a stagflationary environment. During its monetary tightening phase, the Federal Reserve did not sufficiently reduce its balance sheet after injecting nearly $5 trillion into the economy during the pandemic. This excess liquidity and relaxed financial conditions have inflated asset values, creating a wealth effect. According to former Fed Chairman Ben Bernanke, when asset values such as stocks and real estate rise, households perceive themselves as wealthier, boosting their confidence, which increases consumer spending and economic growth. However, these loose financial conditions can also contribute to rising inflation.

The S&P 500 offers a poor risk-reward since it is extremely overvalued, and the 15% earnings estimates for next year seem unrealistic. Also, the S&P 500 is no longer a diversified index since the Magnificent Seven mega-cap technology stocks represent a 31% weighting. Finally, the economy has been in a deflationary environment for more than a year due to declining inflation and growth rates. We are concerned that the government's massive fiscal deficit and Fed’s loose monetary conditions could increase the inflation rate and push the economy into a stagflationary environment.

To outperform and preserve capital in this high-risk period, we maintain a diversified portfolio that is underweight the overvalued growth stocks and overweight the healthcare and consumer staples sectors, which typically outperform during periods of slowing growth. We are underweight equities relative to our benchmarks and about 50% of the portfolio is invested in short-duration bonds that yield about 5.0%. Finally, we are invested in gold – the ultimate safe haven – which is performing well this year due to geopolitical stress, economic uncertainty, and central bank ineptness. We plan to maintain a substantial position in short-term fixed-income assets until economic uncertainty diminishes and equities present a more favorable risk-reward opportunity.

Third Quarter Review:

After a sharp 9.7% decline in early August, the equity rally continued during the third quarter, and the S&P 500 increased by 5.5%. After a weak first half of 2024, the broader market performed well in Q3, as the equal-weight S&P 500 and the Russell 2000 increased by 9.6% and 9.3%, respectively. Foreign markets were also strong -- the MSCI EAFE International increased by 6.7%, and the MSCI Emerging Markets indexes rose by 7.6%.

While stocks rallied, interest rates declined sharply due to weak economic data and elevated geopolitical risk. The U.S. 2-year Treasury yield fell by 1.12% to 3.65%, while the U.S. 10-year Treasury yield dropped by 0.61% to 3.79%. Gold, the ultimate safe haven, jumped by 13.7% in the third quarter amid the market and economic volatility. Consistent with the weak economic data and recessionary concerns, the S&P's 2024 earnings estimate fell by 2.0% during Q3. As the table below indicates, the S&P 500's 5.5% increase was primarily due to a 7.6% increase in valuation and not improving fundamentals.

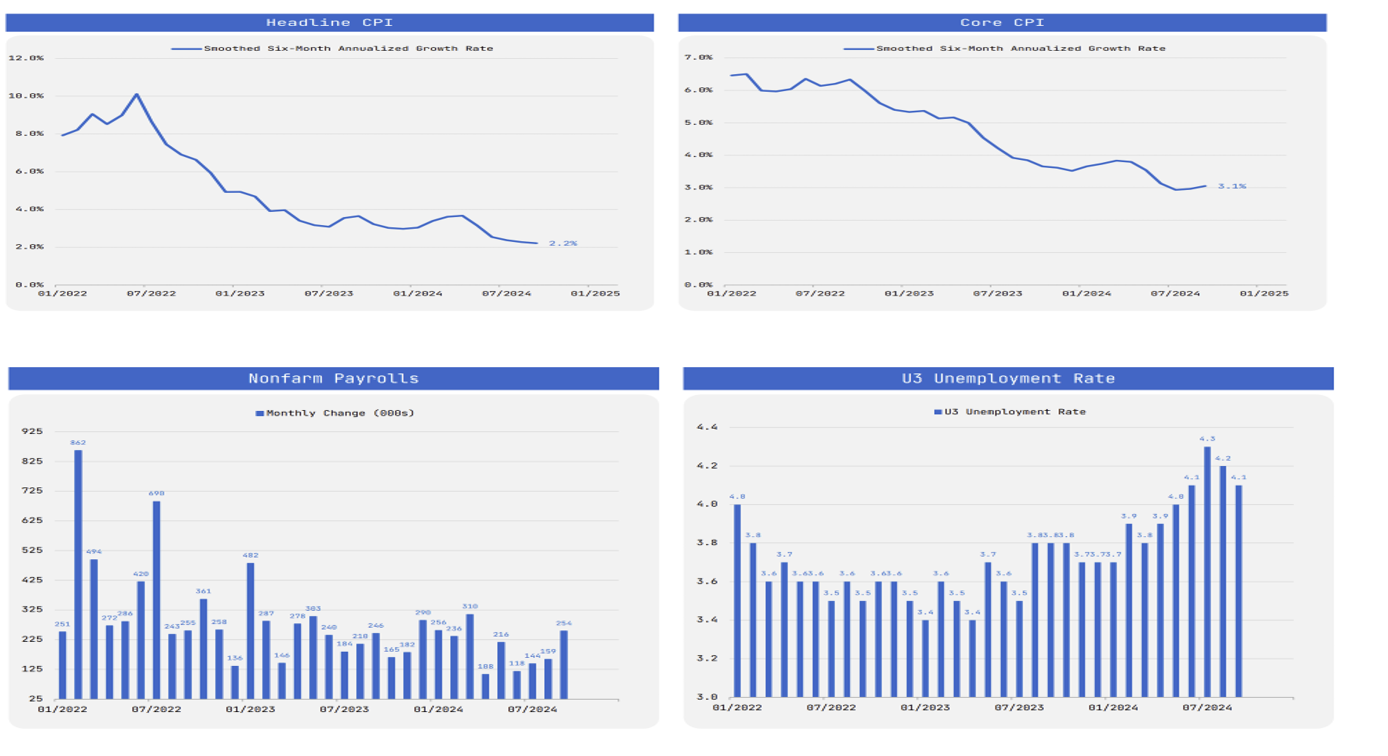

While the inflation rate continued to decrease toward the Fed's target in Q3, several weak employment reports concerned investors that the Fed kept short-term interest rates too high for too long and the economy was near recession. In August, it was reported that the July unemployment rate unexpectedly rose to 4.3% from 3.5% a year ago, and the Bureau of Labor Statistics (BLS) announced that it had overestimated payroll growth from April 2003 to March 2024 by 818,000 jobs. So, the economy created only 2.1 million jobs (an average of 175k per month) over those twelve months instead of the previously reported 2.9 million jobs (an average of 242k per month).

On September 18, the Federal Reserve reduced short-term interest rates by an unexpectedly large 0.50%. Its Summary of Economic Projections (SEP) indicated that it would cut rates by another 0.50% in 2024 and by 1.00% to yield 3.4% in 2025. Fed Chairman Powell stated, "Our restrictive monetary policy has helped restore the balance between aggregate supply and demand, easing inflationary pressures and ensuring that inflation expectations remain well anchored. Our patient approach over the past year has paid dividends: Inflation is now much closer to our objective, and we have gained greater confidence that inflation is moving sustainably toward 2 percent. As inflation has declined and the labor market has cooled, the upside risks to inflation have diminished, and the downside risks to employment have increased. We now see the risks to achieving our employment and inflation goals as roughly in balance, and we are attentive to the risks to both sides of our dual mandate."

Since the Fed's jumbo rate cut and dovish rate projection, economic data has unexpectedly strengthened, and long-term bond yields rose sharply over concern that the economic strength would lead to an increase in inflation. In October, the BLS reported that employment growth surged, and 254,000 jobs were created in September, which was significantly above economists' expectations of 140,000. Also, after growing 3.0% in Q2, the Atlanta Fed's GDPNow estimates that the economic growth accelerated to 3.4% in the third quarter.

Source: EPB Business Cycle Research

The S&P 500 increased by a stout 20.8% during the first nine months of 2024, while the equal-weight S&P 500 and the Russell 2000 increased by 13.5% and 10.1%, respectively. The MSCI EAFE International rose by 11.0%, and the MSCI Emerging Markets indexes increased by14.1%.

Year-to-date, the S&P 500's significant outperformance versus the other major equity averages was driven by the 31% concentration in the "Magnificent Seven" mega-cap technology stocks (Apple, Nvidia, Microsoft, Amazon, Google, Meta, and Tesla) that benefited from AI hype. The Magnificent Seven contributed 45% of the S&P 500's appreciation this year. Additionally, NVIDIA, the technology company that designs AI chips, accounted for 23.3% of the S&P 500 performance in 2024. Due to this concentration risk, we believe that the S&P 500 lacks appropriate diversification for long-term investors.

In addition to concentration risk, we are concerned that the S&P 500's appreciation this year was driven by higher valuation and not improving fundamentals. While the S&P rallied sharply this year, the 2024 earnings estimate fell by 3.1% through the third quarter. As the table below indicates, the S&P 500's 20.8% increase was primarily due to a 24.7% increase in valuation and not improving earnings.

Economic Outlook

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of the rate of change for economic growth and inflation. This enables us to strategically position our portfolio to perform well in all economic environments.

The economy has been in a deflationary environment for more than a year due to declining inflation and growth rates. We are concerned that the government's massive fiscal deficit and loose monetary conditions could increase the inflation rate and push the economy into a stagflationary environment.

Inflation in the United States reached a 40-year high in 2022, with the Consumer Price Index (CPI) peaking at 9.1% in June. This surge was due to massive government spending and the Fed printing nearly $5 trillion during the COVID-19 pandemic. To combat this high inflation, the Federal Reserve undertook a series of aggressive interest rate hikes starting in March 2022. By July 2023, the federal funds rate had been raised from 0% to 5.38%, marking one of the fastest rate hike cycles in history.

These rate increases were aimed to slow economic activity and bring inflation down toward the Fed's target of 2%. By September 2023, core inflation had peaked, and since then, we have been in a period of slow economic growth with a falling inflation rate. The leading economic indicators, such as the yield curve, Leading Economic Index (LEI), and money supply growth, suggest that the Fed's tightening cycle was likely to result in a mild recession. This outcome is consistent with most tightening cycles.

The inflation and economic growth rates have declined due to the Fed's interest rate tightening cycle. Since September 2022, core inflation fell from 6.6% to 3.2%, and employment growth dropped from 3.9% to 1.6%.

Source: FRED

Since 1968, every time short-term rates yielded more than long-term rates, a recession occurred with an average lead time of 14 months. One key explanation behind an inverted yield curve's ability to forecast the last eight recessions lies in the challenges it creates for banks and financial institutions. This results in reduced lending, which leads to slower economic growth. A flattening yield curve after inversion indicates that the recession is imminent.

Source: FRED

In addition to the yield curve, another accurate indicator of the economy is the Conference Board's Leading Economic Index. The LEI is currently forecasting a recession. According to famed economist David Rosenburg, the LEI has had a perfect record of forecasting recessions since 1959. Historically, when the LEI is below 0 and falling, the S&P 500 has an average return of (11.2%).

Source: The Conference Board

Milton Freidman famously said:" inflation is always and everywhere a monetary phenomenon." The Fed ignored the surging money supply, and inflation rose to a 40-year high. Today, the money supply's growth rate has collapsed, and economic growth and inflation will continue to decline.

Source: FRED

The aggregate economy has continued to grow steadily despite contractions in the leading and cyclical sectors. We attribute this resilience to excessive government spending and loose financial conditions. However, we believe the deficit spending is unsustainable, and the loose financial conditions will accelerate inflation.

Source: EPB Business Cycle Research

The National Bureau of Economic Research (NBER) examines six aggregate economic variables to determine whether the U.S. economy is in a recession – nonfarm payrolls, the employment level, real personal income, real personal consumption, real retail sales, and industrial production. Among these six economic variables, industrial production and real retail sales have been weak, the labor market and income growth have been slowing, while consumption has remained strong.

Source: EPB Business Cycle Research

In addition to the $1.8 trillion budget deficit (6.4% of GDP), consumption has remained strong because many consumers and businesses locked in low interest rates during the pandemic and were immune or even benefitted from higher short-term interest rates. Furthermore, during its monetary tightening phase, the Federal Reserve did not sufficiently reduce its balance sheet, resulting in excess liquidity and easy financial conditions. These easy financial conditions elevated asset values and led to a wealth effect. Former Fed Chairman Bernanke was a major proponent of the wealth effect. He believed that when asset values such as stocks and real estate increase, households feel wealthier, which boosts their confidence and leads to increased consumer spending and economic growth.

We believe the Fed failed to adequately reduce its balance sheet after printing nearly $5 trillion during the pandemic. The Fed started tightening financial conditions in March of 2022 by increasing short-term interest rates, reducing liquidity in the system, and shrinking its bloated balance sheet. After several large regional banks failed, the Fed changed course and increased liquidity in the system in March of 2023. In addition to not reducing liquidity, we believe it was a mistake for the Fed to cut short-term interest rates by 0.50% when the S&P 500 was near an all-time high, core CPI was 3.3%, the unemployment rate was 4.05%, and the estimated economic growth in Q3 was 3.4%.

In our view, the Fed and its 963 PhD economists have again underestimated inflation. In 2021, inflation reached the highest level in several decades, yet the Fed failed to tighten monetary policy because it believed that inflation was transitory and driven mainly by supply chain problems instead of the massive increase in the money supply. In February of 2022, inflation reached 8%, a 40-year high, yet the Fed kept short-term interest rates at 0% while printing $60 billion each month to buy financial assets and suppress long-term interest rates. By March of 2022, the Fed embarked on one of the most aggressive tightening campaigns, ultimately leading to three significant bank failures – Silicon Valley Bank, Signature Bank, and First Republic -- in Q2 2023.

We believe that the Fed continues to underestimate or ignore the impact of its balance sheet and the money supply on inflation. Since the Fed surprised the market by cutting interest rates by 0.50% and tacitly claiming victory over inflation, inflation expectations and bond yields have surged. The U.S. 10-year Treasury yield spiked from 3.7% on September 17 to 4.2% today. This 0.50% increase in long-term rates and the 6.5% spike in the price of gold clearly indicate that the market believes that the Fed made another monetary mistake.

During the pandemic, the Fed "printed" $4.8 trillion to buy financial assets to stabilize the financial markets and the economy. Its balance sheet grew from $4.16 trillion in Q1 2000 to $8.95 trillion in q2 2022, an increase from 19.8% to 35% of GDP. This massive increase in the Fed's balance sheet drove inflation to a forty-year high. During the Fed's tightening cycle, it only reduced its balance sheet by $1.8 trillion to $7.15 trillion, which is a bloated 25% of GDP.

In addition to the Fed's balance sheet, the Monetary Base (bank reserves plus currency in circulation) increased from $3.4 trillion before the pandemic to $6.4 trillion in December 2021. During the Fed's tightening cycle, the monetary base declined to $5.3 trillion in February 2023. In March of 2023, several significant regional bank failures led the Fed to increase liquidity in the system, and the monetary base rose by $600 billion, where it has essentially remained.

In the early 1970s, the Fed prematurely believed it had defeated inflation and began to ease monetary policy. Unfortunately, the Fed was wrong, and inflation reaccelerated to a record level. Hopefully, Chairman Powell has not made the same monetary mistake.

Stock Market Outlook:

We believe the S&P 500 offers a poor risk-reward since it is extremely overvalued, and the earnings estimates for next year seem unrealistic. The S&P 500 is no longer a diversified index since the Magnificient Seven mega-cap technology stocks represent a 31% weighting. In addition to concentration risk, we are concerned that the S&P 500 appreciation this year was driven by higher valuation and not improving fundamentals. While the S&P rallied sharply this year, the 2024 earnings estimate fell by 3.1% through the third quarter. As the table below indicates, the S&P 500's 21.2% increase was primarily due to a 25% increase in valuation and not improving earnings.

When the Fed met last month and reduced interest rates, it also gave its Summary of Economic Projections (SEP). The Fed forecasts that GDP will grow by 2.0% in 2025, and inflation will increase by 2.2% so that nominal GDP will increase by 4.2%. In this environment of modest economic growth, Wall Street analysts expect the S&P 500 profits will grow by 16.5% to $274 from an estimated $235 this year. This growth seems unrealistic since corporate profits grow in line with nominal GDP over time, and profit margins are currently near a record high.

According to Factset, the current S&P 500 earnings growth rate for the third quarter is only 3.4%. Excluding the Mag Seven, the growth rate of the remaining 493 companies in the S&P 500 is only 0.1%. In our view, the ebullient 2025 earnings expectations make no sense.

In addition to unrealistic earnings expectations, we believe that the S&P 500 is no longer a diversified index because seven mega-cap technology stocks have a 31% weighting. Since these stock valuations have benefitted from the AI mania, any disappointment in AI development would adversely impact the S&P 500. Additionally, according to Goldman Sachs, concentration risk is currently in the 99th percentile, and historically periods of extreme concentration have occurred at significant market tops.

Source: Goldman Sachs

Finally, stocks are very overvalued in a period of significant economic and geopolitical uncertainty.

Since the price you pay for an investment is the most critical factor in driving returns, investors should focus on valuation to determine an investment's long-term expected return and its risk-reward. Based on most long-term valuation measures, the S&P 500 is as overvalued as any period in market history. The main drivers of overvaluation are the excess liquidity from the Fed's balance sheet expansion and the impact of passive funds on the S&P 500.

The S&P 500 no longer adequately discounts the fundamentals because passive flows and speculative investment strategies drive it. The S&P 500 benefits from monthly 401k contributions that are passively invested in the index regardless of the fundamentals – i.e., changes in earnings and interest rates. Over thirty cents of each 401k contribution dollar are invested in the mega-cap technology stocks. Also, the S&P is impacted by quantitative investment strategies –short volatility, dispersion trades, risk parity, gamma squeezes, and trend following – that are not driven by the fundamentals. As we experienced in early August, these market structure issues can lead to forced selling as these quant strategies de-lever and unwind their speculative positions.

Market Value to GDP – "Still, it is probably the best single measure of where valuations stand at any given moment." –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks are more than 100% higher than their historical average level and more expensive than during the 2000 technology bubble.

Source: Longtermtrends.net

Shiller's CAPE (a valuation measure that smooths out cyclical earnings fluctuations) indicates that stocks are more than 50% above their long-term average and the 10-year expected return is less than 3% per annum.

Source: Longtermtrends.net

Last week, Goldman Sachs published a report based on their long-term valuation model. The model estimated the S&P 500 would generate a 3% annualized return over the next 10 years, which ranked in the 7th percentile of 10-year returns.

Source: Goldman Sachs

Our Model Portfolio Review:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of the rate of change for economic growth and inflation. This enables us to strategically position our portfolio to perform well in all economic environments.

The S&P 500 is currently overvalued, presenting investors with a poor long-term risk reward. This situation is exacerbated by an unfavorable economic environment characterized by slowing economic growth and elevated inflation. Additionally, the Federal Reserve's recent policy actions have raised concerns about another monetary mistake. After the Fed decided to cut short-term interest rates by 0.50%, the U.S. 10-year Treasury yield spiked by 0.50%, reaching its highest level since July, and gold prices surged by 6.5%, reflecting concern that inflation may accelerate in the future.

To outperform and preserve capital in this high-risk period, we have a diversified portfolio that is underweight the overvalued growth stocks and overweight the healthcare and consumer staples sectors, which typically outperform during periods of slowing growth. We have underweight equities relative to our benchmarks, and about 50% of the portfolio is invested in short-duration bonds that yield about 5.0%. Finally, we are invested in gold – the ultimate safe haven – which is performing well this year due to geopolitical stress, economic uncertainty, and central bank ineptness. We plan to maintain a substantial position in short-term fixed-income assets until economic uncertainty diminishes and equities present a more favorable risk-reward opportunity.

Current Risk-Weighted Portfolio

Our portfolio's risk level (annualized volatility) is 8.3%, which is less than our 60\40 benchmark's historic risk level of 10.7%, and its current risk level of 12.4%.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed.

All investments contain risk.

All information disclosed in this statement is accurate and complete to the best of our knowledge. Past performance is no guarantee of future results, and there is no assurance that the firm or client's investment objectives will be achieved.