The Manley Macro Memo

Despite uncertainties around tariffs, conflicts between the Administration and the Fed, and overly optimistic earnings forecasts, stocks are priced for perfection.

Executive Summary:

The second quarter of 2025 experienced significant volatility and large market fluctuations. Following a slight loss in the first quarter, stock prices declined sharply after President Trump unveiled his "Liberation Day” tariff plan that was more aggressive than expected. By April 9th, the S&P 500 had fallen 21.3% from its mid-February peak, when President Trump announced a 90-day suspension of new tariffs. Despite a sharp decline early in the quarter, most major asset classes rebounded strongly after tariffs were suspended. Despite ongoing economic uncertainty and geopolitical tensions, the S&P 500 climbed 10.8% to reach an all-time high by the end of the quarter.

This year, economic growth is slowing, and inflation remains high because of a heavy debt burden, a large budget deficit, and the Federal Reserve’s bloated balance sheet. These structural economic problems worsened because of the pandemic. Currently, the budget deficit is about $2 trillion (6.7% of GDP), and the interest expense on our national debt is $1.1 trillion (more than our military spending). Our nation’s debt has increased to $36.2 trillion (121% of GDP), while the inflation rate is 2.9%, significantly above the Federal Reserve’s 2% target.

When President Trump took office, he recognized that the budget deficit was unsustainable at nearly 7% of GDP, and he believed that unfair trade practices by our trading partners had led to the erosion of our country's manufacturing base. To reduce the budget deficit, the President proposed permanent low taxes, less government spending, and deregulation. To improve our manufacturing base and attract investment, he threatened to impose large tariffs on our trading partners, encouraging them to reduce their own tariffs and open their markets to U.S. goods.

It seems that the President changed course after the “Liberation Day” market panic. Instead of cutting spending to reduce the deficit, the President appears to favor imposing high tariffs to boost revenue and pressuring the Fed to cut interest rates to lower the country's interest costs. We believe that this shift away from supply-side, free-market economics toward mercantilism— the idea that national wealth and power are best increased by maximizing exports through tariffs, a weak currency, and suppressed interest rates— is not widely recognized by most investors.

We believe stocks currently offer a poor risk-reward profile because they are overbought, overvalued, and exhibiting weak market breadth. Despite uncertainties surrounding tariffs, conflicts between the Administration and the Fed, and overly optimistic earnings forecasts, stocks are priced for perfection. Investors appear complacent, assuming that the President won't implement the proposed tariffs, but we remain skeptical. We worry that in the long term, the Administration’s weak dollar policy and preference for artificially low interest rates could trigger an inflationary period similar to 2022. We believe we are well-positioned for that scenario due to our limited bond exposure and investments in international stocks, gold, and commodities.

Second Quarter 2025 Market Review:

The second quarter of 2025 experienced significant volatility and large market fluctuations. Following a slight loss in the first quarter, stock prices declined sharply after President Trump unveiled his "Liberation Day” tariff plan that was more aggressive than expected. By April 9th, the S&P 500 had fallen 21.3% from its mid-February peak, when President Trump announced a 90-day suspension of new tariffs.

Despite a sharp decline early in the quarter, most major asset classes rebounded strongly after tariffs were suspended. Despite ongoing economic uncertainty and geopolitical tensions, the S&P 500 climbed 10.8% to reach an all-time high by the end of the quarter. In this risk-on environment, the equal-weighted S&P 500 and Russell 2000 small-cap indexes increased by 5.3% and 8.5%, respectively. Additionally, international markets continued to outperform U.S. equities, supported by a weak dollar, with the MSCI EAFE Index rising by 11.3% and the MSCI Emerging Markets Index increasing by 11.4% during the second quarter.

While the S&P 500 was very volatile and increased by 10.8% in Q2, the bond market remained mostly stable. The U.S. 2-year Treasury yield dropped by 0.18% to 3.72%, while the U.S. 10-year Treasury yield rose slightly by 0.02% to 4.23%. Additionally, the volatility and economic uncertainty pushed gold, the ultimate safe haven, higher by 5.8%, while oil declined by 8.9% in Q2.

The economic data in the second quarter remained solid, despite volatility in the financial markets. The unemployment rate remained at a very low 4.1%, and core inflation increased slightly from 2.8% in March to 2.9% in June. The Federal Reserve Bank of Atlanta’s GDPNow forecasted that U.S. real GDP grew by 2.4% in the second quarter, while FactSet estimated corporate profits increased by 4.8%, on a revenue increase of 4.2% in Q2.

When President Trump took office, he recognized that the budget deficit was unsustainable at 7% of GDP, and he believed that unfair trade practices by our trading partners had led to the erosion of our country's manufacturing base. To reduce the budget deficit, he wanted Congress to make his 2017 tax cuts permanent and reduce other taxes to stimulate economic growth. Additionally, he established the DOGE (Department of Government Efficiency) to combat government waste and fraud. To improve our manufacturing base and attract investment, he threatened to impose large tariffs on our trading partners, encouraging them to reduce their own tariffs and open their markets to U.S. goods.

In Q1, the stock market was sluggish as the Trump administration implemented austerity policies, and U.S. Treasury Secretary Scott Bessent stated that as these policies are enacted, the economy will enter a “detox period” as it transitions from excessive government spending to a private-sector-led economy. He said that the economy and the market have become reliant on government spending, and now we must navigate this detoxification phase.

In Q2, following the announcement of substantial tariffs on “Liberation Day”, financial markets plummeted, as it was feared that these tariffs would push the economy into a recession. To stabilize the financial markets, tariffs were suspended for ninety days and recently delayed until August 1st. Additionally, instead of implementing strict austerity by cutting excessive government spending, the Administration and Congress opted for modest reductions, which, in our view, left the budget deficit at an unsustainable level. As the financial markets rallied, the Wall Street pundits created narratives – TACO (Trump always chickens out) to disparage the President’s negotiating style and DDM (deficits don’t matter) to explain and sustain the market rally.

Stocks tumbled in early April because the proposed tariffs would likely trigger a recession. Wall Street created narratives to encourage investors to ignore the risks and push stocks higher. The ninety-day suspension was extended to August 1st, and since no trade deals were finalized, President Trump sent letters to many of our trading partners informing them that tariffs as high as 30% would be implemented on August 1st. Although the recent letters proposed tariffs similar to those announced on “Liberation Day,” the markets had a muted reaction since many investors believe the threat is just a negotiating ploy (i.e., the TACO trade).

President Trump has made it clear that he supports tariffs because he believes foreign exporters pay the tax, not U.S. consumers and corporations. While 30% tariffs may be a negotiating tactic, we expect that the tariffs will be higher than the 10% level that Wall Street is comfortable with. Additionally, following numerous successes—securing the border, passing the One Big Beautiful Bill, and achieving military success in Iran—we believe the President is emboldened and will be more aggressive in trade negotiations, especially given the stock market's all-time high. We are concerned that high tariffs would push a slowing economy toward recession.

In our view, there is significant economic uncertainty, and U.S. equities are priced for perfection. The S&P 500 has an estimated earnings yield (earnings divided by price) of 4.1%, which is approximately 0.40% lower than the U.S. 10-year Treasury yield. Additionally, the S&P 500’s price-to-earnings (P/E) ratio, based on trailing 12-month earnings, is very high 26.1 times. In a slowing economic environment, the S&P’s P/E ratio could regress towards its 50-year average of 16.5x, implying a 36.8% market decline.

Economic Outlook

As value investors, our asset allocation is driven by long-term valuation measures and the risk-reward opportunities present in the market. Moreover, we analyze the leading economic and market-based indicators to determine the probable path of the rate of change for economic growth and inflation. This enables us to strategically position our portfolio to perform well in all economic environments.

This year, economic growth is slowing, and inflation remains high because of a heavy debt burden, a large budget deficit, and the Federal Reserve’s bloated balance sheet. These structural economic problems worsened because of the pandemic. Currently, the budget deficit is about $2 trillion (6.7% of GDP), and the interest expense on our national debt is $1.1 trillion (more than our military spending). Our nation’s debt has increased to $36.2 trillion (121% of GDP), while the inflation rate is 2.9%, significantly above the Federal Reserve’s 2% target.

Since the pandemic, the government's spending has risen from $4.86 trillion annually (22.4% of GDP) to $7.16 trillion (23.9% of GDP)—a 47% increase over five years. Today, government spending is 2.0% or $599 billion above its 40-year average spending-to-GDP ratio of 21.9%, and the government is spending more than during most recessions, despite a 4.1% unemployment rate, which is well below its 60-year median of 5.6%.

Government spending increased by 47% from 2020 to 2025, and is currently 2.0% or $599 billion above its 40-year average spending-to-GDP ratio of 21.9%. Although the unemployment rate is low at 4.1%, government spending remains higher than during most past recessions.

Source: FRED

While the government increased spending during the pandemic, the Federal Reserve cut interest rates to 0% and printed nearly $5 trillion to purchase financial assets to stabilize financial markets. The Fed failed to reverse its emergency measures, and inflation rose to a forty-year high in 2022. In our view, inflation remains high and well above the Fed’s 2% target because the Fed never adequately shrank its balance sheet. After increasing from $3.4 trillion before the pandemic to $6.4 trillion, the monetary base (comprising currency in circulation and bank reserves) has only slightly decreased and has remained around $5.6 trillion for the past three years.

The Federal Reserve did not sufficiently unwind its emergency policies after the pandemic, leading to a significant rise in inflation, which hit a forty-year high in 2022 and remains well above the Fed’s 2% target. This sustained inflation is due to the Fed's failure to shrink its balance sheet adequately.

Source: FRED

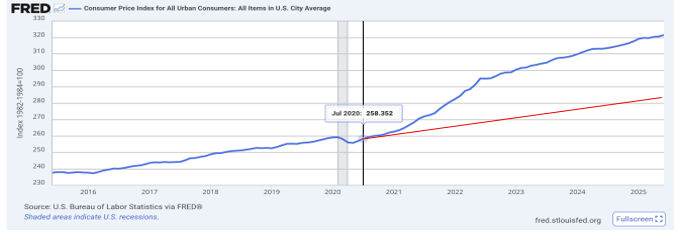

While the Fed claims that the inflation rate is declining, it is referring to the rate of change, not the aggregate price level, which continues to increase at a rate of 2.9%. If the Fed had been successful in keeping inflation at 2% after the pandemic, prices would be 11.3% below their current level (the red line represents the 2% trendline growth where prices should be).

Source: FRED

When President Trump took office, he recognized that the budget deficit was unsustainable at nearly 7% of GDP, and he believed that unfair trade practices by our trading partners had led to the erosion of the country's manufacturing base.

To reduce the budget deficit to 3%, he wanted Congress to make his 2017 tax cuts permanent and deregulate the private sector to boost the economy. He established the DOGE (Department of Government Efficiency) to combat government waste and fraud. Additionally, he sought to increase energy production through deregulation in order to combat inflation and lower interest rates. To improve our manufacturing base and attract investment, he threatened to impose large tariffs on our trading partners, encouraging them to reduce their own tariffs and open their markets to U.S. goods.

We believed that President Trump’s plan to keep taxes low, deregulate, reduce government spending, and incentivize capital investment would lead to robust growth, which would reduce the budget deficit and increase living standards in the long term. U.S. Treasury Secretary Scott Bessent stated that as these policies are enacted, the economy will enter a “detox period” as it transitions from excessive government spending to a private-sector-led economy. He said that the economy and the market had become reliant on government spending, and now we must navigate this detoxification phase.

When President Trump announced his “Liberation Day” tariff plan, the markets plunged because the tariffs were significantly higher than expected. Since tariffs are a tax increase, investors believed that the high tariffs, coupled with Secretary Bessent’s “detox period,” would drive the economy into recession. After four days of plunging stock and bond prices, President Trump announced a 90-day pause on the most severe "reciprocal" tariffs, and recently, the tariff deadline was extended until August 1st.

Following the market crash, President Trump revised his economic strategies. Although One Big Beautiful Bill made the 2017 tax cuts and 100% bonus depreciation permanent, the planned spending cuts were modest ($1.1 trillion over ten years), and the budget deficit is likely to stay large. Instead of reducing spending, the President appears to favor imposing high tariffs to boost revenue and pressuring the Fed to cut interest rates to lower the country's interest costs.

We believe that this shift from supply-side, free-market economics to mercantilism—the belief that national wealth and power are best increased by maximizing exports through tariffs, a weak currency, and suppressed interest rates—is not widely appreciated by most investors. While many investors expect President Trump to yield on his trade demands, we believe the President is emboldened by his success -- securing the border, passing the One Big Beautiful Bill, achieving military success in Iran and the stock market at an all-time high – and we expect that the tariff rate will be significantly above the current 10% rate.

Because there have been no formal trade agreements and limited progress, President Trump recently sent letters to trade partners to officially inform them of new or updated U.S. tariff rates on their exports. These rates will take effect on August 1, 2025, unless a new trade deal is made beforehand. According to Yale's Budget Lab, the proposed tariffs would have an effective rate of 20.6%, which is the highest since 1910 and greater than the Smoot-Hawley Tariff Act of 1930 that led to the Great Depression.

Tariffs are a tax that someone must pay, and President Trump believes that foreign exporters, not American corporations or consumers, will bear the cost. With U.S. annual imports reaching $3.36 trillion in 2024, a 10% tariff would generate about $336 billion (1.1% of GDP), while the Budget Lab’s estimated 20.6% tariff could bring in $692 billion in revenue (2.3% of GDP), assuming static conditions. To put this in perspective, last year the government collected $489.6 billion (1.6% of GDP) in corporate income tax revenue. We believe the President is emboldened to impose large tariffs to reduce the deficit and grow our manufacturing base. We are concerned that this tax will negatively affect the U.S. economy as it's implemented, and complacent investors are not prepared because they believe it’s a negotiating tactic.

Source: The Budget Lab at Yale

In addition to implementing tariffs, the President is pressuring the Federal Reserve to sharply cut interest rates to reduce the country’s $1.1 trillion interest expense and narrow the budget deficit. On July 9th, the President posted on Truth Social, “Our Fed Rate is AT LEAST 3 Points too high. “Too Late” is costing the U.S. 360 Billion Dollars a Point, PER YEAR, in refinancing costs. No Inflation, COMPANIES POURING INTO AMERICA. “The hottest Country in the World!” LOWER THE RATE!!!"

While we believe that the Fed’s loose monetary policy has contributed to wealth inequality, an excessive debt burden, and inflated asset bubbles, short-term interest rates seem appropriate given the elevated inflation rate and low unemployment levels. According to the Taylor Rule — a rules-based formula linking a central bank's policy rate to inflation and economic growth – short-term interest rates are essentially neutral, and aggressive rate cuts are not suitable. Additionally, since the Fed Funds rate is currently 4.33% and as of June 2025, the average interest rate on the national debt is 3.375%, the Fed would have to cut interest rates to recessionary levels to reduce the interest expense.

Source: Bloomberg

In summary, excessive government spending and unprecedented peacetime budget deficits are unsustainable. After the “Liberation Day” financial panic, it appears the President has shifted from proven supply-side, pro-growth economic policies to mercantilism in an effort to reduce the budget deficit and stimulate economic growth. We believe this change introduces significant economic uncertainty that many complacent investors may not be prepared for.

Stock Market Outlook:

We believe the market presents an unfavorable risk-reward. The stock market is overbought and overvalued, and the market’s breadth is weak. Additionally, the S&P 500 faces significant concentration risk, as the ten largest companies make up nearly 40% of the index.

By April 9th, the S&P 500 had fallen 21.3% from its mid-February peak and had technically entered a bear market. Stocks soared when President Trump announced a 90-day suspension of new tariffs, and eleven weeks later, the S&P 500 reached an all-time high. Since the April 9th tariff suspension, the S&P 500 has increased by more than 30%, despite no formal trade deals or significant improvements in the economic outlook – in fact, S&P 500’s 2025 earnings were revised lower by 3.7% in the second quarter.

We believe that this large rally was driven by retail investors “buying the dip,” as well as passive investment flows (automatic 401(k) contributions and corporate buybacks) and quantitative investors (trend-following and volatility-targeting strategies) that invest regardless of fundamentals. Additionally, option speculators and the market makers, who must quantitatively hedge their exposure, are having an outsized impact on the market’s structure and fueling the rally. According to Goldman Sachs, 0 DTE options (options that expire the same day) now account for more than 60% of S&P 500 listed volume.

Source: Goldman Sachs

Since the April 9th tariff suspension, the S&P 500 has increased by over 30% in about three months, reaching an all-time high. While the S&P 500 is at a record level, the equal-weighted S&P 500 is 1.2% below its December high, and the Russell 2000 (small-cap index) remains 8.9% below its November 2024 high. Also, only 54.7% of NYSE stocks are above their 200-day moving average, meaning that 45.3% of NYSE companies are in a bear market. Additionally, the ten largest companies in the S&P 500 now make up nearly 40% of the index. The market’s weak breadth and extreme concentration suggest that the market is not as healthy as it appears.

Source:Stockcharts.com

Source:Apollo

According to FactSet, the S&P 500's earnings are projected to grow by 9% in 2025 and 14% in 2026. The forward 12-month P/E ratio for the S&P 500 stands at 22.3, which is 21.1% higher than the 10-year average of 18.4. While Wall Street anticipates earnings to increase by 24.3% over the next two calendar years, the Federal Reserve, in its June Summary of Economic Projections, predicts nominal GDP growth of only 8.6%. Furthermore, the ten largest companies are valued more highly than the top ten during the 2000 internet bubble. In our opinion, Wall Street is overly optimistic given the slowing economy, the tariff uncertainty, and the conflict between the Administration and the Fed.

Despite the slowing economy and tariff uncertainty, stocks are selling at a historic valuation level. According to Apollo, the ten largest companies are currently more expensive than the ten largest during the 2000’s tech bubble.

Source:Apollo

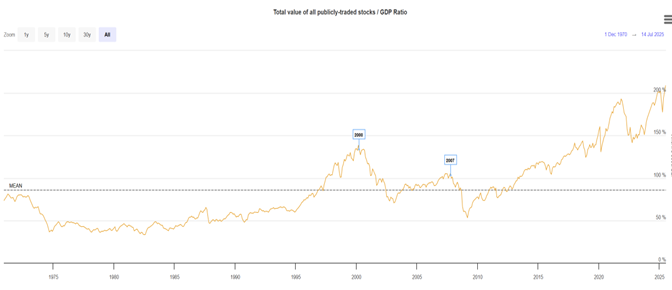

As value investors, we believe that the price you pay most accurately determines your return on investment. While valuation models exhibit little predictive power over the short term, they correlate strongly with long-term returns over ten years or more. According to Market Value to GDP and Shiller’s CAPE valuation models, the S&P 500 is expected to return between -2.9% per annum and 1.4% per annum over the next ten years.

Market Value to GDP – "Still, it is probably the best single measure of where valuations stand at any given moment." –Warren Buffett, December 10, 2001. Based on market value to GDP, stocks are more than 100% higher than their historical average level and more expensive than during the 2000 technology bubble. Over the next ten years, the model forecasts an annual return for the S&P 500 of -2.9%.

Source: Longtermtrends.com, Allocate Smartly

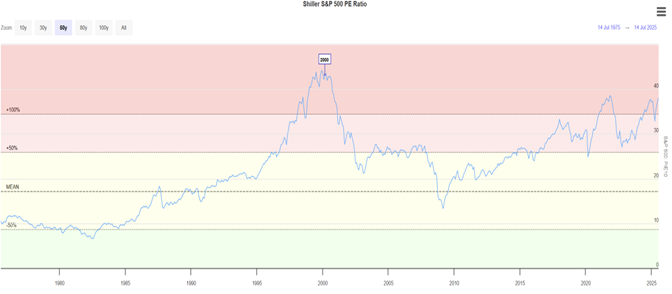

Shiller's CAPE (a valuation measure that smooths out cyclical earnings fluctuations) indicates that stocks are more than 90% above their long-term average, and the 10-year expected return is about 1.4% per annum. Since the 10-year Treasury Inflation Protected Securities (TIPS) yield a real return of 2.0%, the S&P 500 has an inadequate risk premium. Over the next ten years, the model forecasts an annual return for the S&P 500 of 1.4%.

Source: Longtermtrends.com, Allocate Smartly

Our tactical outlook for three months: The S&P 500 is significantly overbought, and several signs of technical exhaustion are apparent. We believe the S&P 500 will trade within a range from its current level of 6300 down to 5700 until the tariff situation and questions around monetary policy are resolved. If the tariifs are implemented as stated on August 1st, we expect greater downside.

Source: Demark

In summary, we believe stocks currently present a poor risk-reward due to being overbought, overvalued, and showing weak market breadth. Despite uncertainties around tariffs, conflicts between the Administration and the Fed, and overly optimistic earnings forecasts, stocks are priced for perfection. Investors appear complacent, believing that the President won't implement the proposed tariffs, but we remain doubtful. During this high-risk period, we will focus on capital preservation until the market’s risk-reward becomes more favorable—specifically, when stocks are cheaper, risk premiums are higher, and both earnings forecasts and investor sentiment are more cautious.

Our Model Portfolio Review:

The benchmark for our model portfolio is the Traditional Blend — 60% equity and 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, to manage risk, we volatility-weight our positions and set a volatility target equal to our benchmark's historic risk level. When volatility increases, our asset allocation dynamically reduces our equity risk exposure.

The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy, or investment product.

Year-to-date, we have performed well, especially on a risk-adjusted basis. Our strong performance is due to our highly diversified and balanced portfolio, which had lower equity exposure and shorter bond duration than our benchmark. Our investments in international stocks and gold, the ultimate safe haven, have yielded positive results, thanks to the dollar's weakness in the first half.

Although there is significant uncertainty about the proposed tariffs and their short-term economic effects, we worry that in the long run, the Administration’s weak dollar policy and preference for artificially low interest rates could lead to an inflationary period similar to 2022. We believe we are well prepared for that scenario due to our limited bond exposure and investments in international stocks, gold, and commodities.

Ultimately, we believe that low taxes, deregulation, incentives for capital investment, along with decreased government spending and stable monetary policy, stimulate economic growth, reduce inflation, and enhance living standards. However, we are worried that the April market panic has prompted the Administration to adopt Mercantilist policies, which could result in a stagflationary economic environment. In such a scenario, our priority will be preserving capital and maintaining purchasing power.

We plan to maintain a highly diversified and balanced asset allocation until economic uncertainty diminishes and equities present a more favorable risk-reward opportunity.

Current Risk-Weighted Model Portfolio

Our portfolio's risk level (annualized volatility) is 10.0%. Our 60\40 benchmark has a historic risk level of 10.7%, and its current risk level is 14.7%.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable but not guaranteed.

All investments contain risk.

All information disclosed in this statement is accurate and complete to the best of our knowledge. Past performance is no guarantee of future results, and there is no assurance that the firm or client's investment objectives will be achieved.

Very good info, Lawrence. My only criticism would be that the real and present risks are much higher than the article observed. Already very elevated tensions between the EU and Russia will only increase as Russia pushes relentlessly towards a Ukraine collapse, and there will be nothing but existential challenges incoming around the mideast, with at best a tactical regional nuc exchange (Game Theory) with a high risk of it escalating to a global hot war. (western commitment to Iran defeat requires a tactical nuc attack) Game theory strongly supports escalation and the closing of the Strait of Hormuz, which itself will crash the global economy.