The Manley Macro Memo

Rising Inflation Expectations and Higher Interest Rates are Causing the Bifricated Stock Market to Mean Revert

Executive Summary:

Despite the S&P 500's overvaluation and poor risk-reward, we believe the bifurcated economy and stock market provide substantial opportunities in 2021. The mega-cap technology and the "stay at home" stocks prospered in 2020, but today their valuations are extreme, and difficult year-over-year comparisons will slow their growth rates. We believe that the market sectors that thrived during the shutdown are at risk as the vaccine is administered and the economy reopens this spring/summer.

While many cheered the GameStop saga as a David and Goliath story of the small investor profiting at the expense of some hedge funds, we believe that the event illustrates how the Fed's profligate monetary policy has turned financial markets into a casino. In response to the economic shutdown caused by the pandemic, the Fed cut interest rates to zero percent and injected more than $3 trillion into financial markets by printing money and buying bonds

Last year, we invested in the safe havens – gold and the U.S. long-term Treasury bond -- to hedge our equity exposure from the momentous economic risks. This year, we are invested in commodities, energy, gold, and foreign markets to hedge our equity exposure from a likely inflation acceleration. While inflation has not been a problem for more than thirty years, the unprecedented monetary and fiscal stimulus used to support the economy during the Covid shutdowns will have unintended consequences.

Market Discussion:

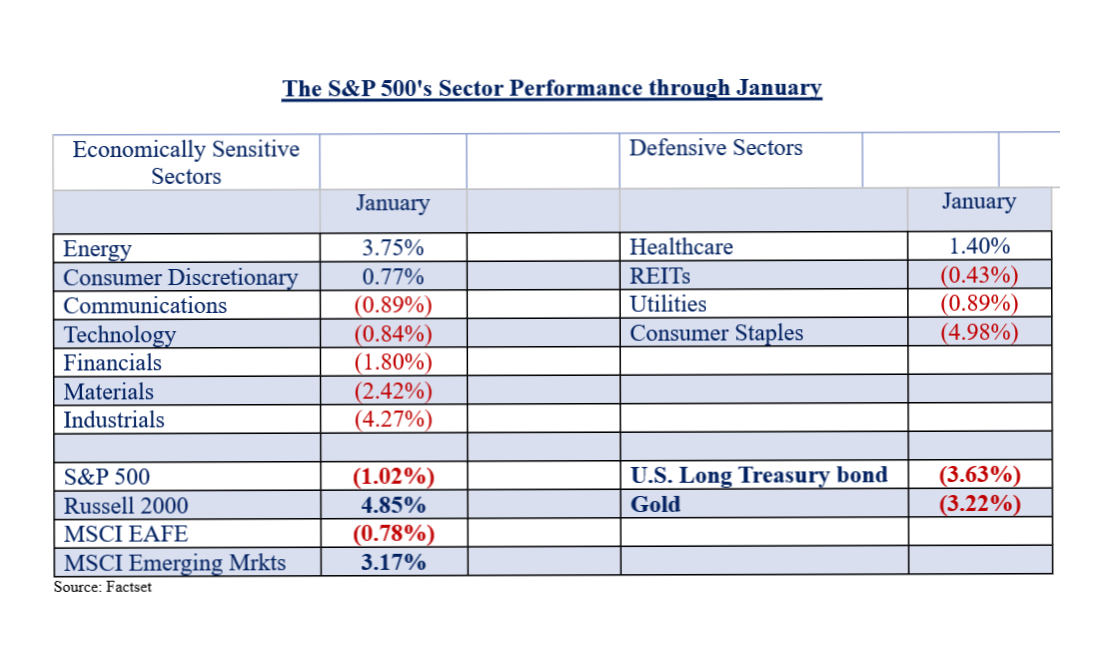

After a strong start to the new year, the stock market ended mixed in January. The S&P 500 declined by 1.0%, while the small-cap Russell 2000 and MSCI Emerging Markets Index rallied by 4.8% and 3.2%, respectively. Vaccine optimism and the promise of more fiscal stimulus drove the S&P 500 to a record high before a coordinated short squeeze led to a spike in market volatility and a sharp market decline near the end of the month.

On January 27th, stocks had their worst day since October because a group of small retail investors on Reddit, a social media platform, coordinated to drive GameStop (a video game retailer) higher because several large hedge funds heavily shorted it. GameStop exploded higher as the coordinated buying forced hedge funds to cover their short positions at a significant loss. This short squeeze strategy spread to other heavily shorted stocks, forcing many hedge funds to reduce their market exposure quickly. This de-risking led to a 4.6% decline in the S&P 500 during the last three days of January.

While many cheered the David and Goliath story of the small investor profiting at the expense of some hedge funds, we believe that the event illustrates how the Fed's profligate monetary policy has turned financial markets into a casino. In response to the economic shutdown caused by the pandemic, the Fed cut interest rates to zero percent and injected more than $3 trillion into financial markets by printing money and buying bonds.

The Fed's actions artificially inflated stocks by driving them from their underlying fundamentals. Additionally, the Fed's "promise" to support asset prices and keep interest rates near zero percent "at least until 2023" encouraged hedge funds and other speculators to increase their risk exposure by borrowing to expand their balance sheet. The chart below illustrates the sharp increase in investors' borrowing after the pandemic struck. In fact, the ratio of margin debt to GDP has never been higher.

Source:TheFelderReport.com

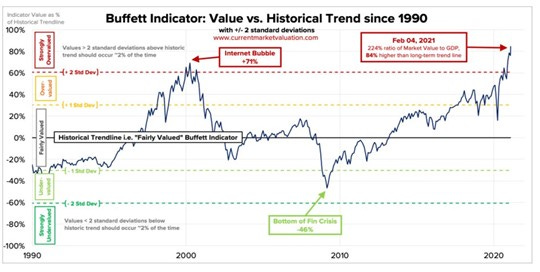

The Fed's financial repression strategy – zero percent interest rates, negative real rates, and printing $120 billion each month to buy financial assets – coupled with feverish speculation has driven stock valuations to a record high (see below the chart of the Buffet Indicator). Currently, the S&P 500 is very expensive and offers a poor risk-reward. According to Factset, the forward 12-month P/E ratio is 22.1, which is 40% above the 10-year average of 15.8.

Source: Bloomberg

As discussed last month, despite the S&P 500's overvaluation and poor risk-reward, we believe the bifurcated economy and stock market provide substantial opportunities in 2021. The mega-cap technology and the "stay at home" stocks prospered in 2020, but today their valuations are extreme, and difficult year-over-year comparisons will slow their growth rates. We believe that the market sectors that thrived during the shutdown are at risk as the vaccine is administered and the economy reopens this spring/summer.

While we expect growth stocks to struggle this year, we see good value and positive risk-rewards in the market's value sectors (financials, industrials, consumer, and energy), which performed poorly in 2020, and are positively leveraged to an economic recovery. Additionally, after underperforming the S&P 500 for more than a decade, we believe that the International and Emerging Markets are poised to outperform while increasing diversification.

In February, stocks are performing well due to the hope of an additional $1.9 trillion in fiscal stimulus and the significant progress in fighting Covid-19. The market's value sectors are outperforming, and many of the overvalued mega-tech stocks are struggling as rising inflation expectations and higher interest rates pressure their valuation levels. We expect these trends to continue for the next few quarters.

While the sharp January sell-off didn't spread into February, the event could presage a larger sell-off in the future if the speculative excesses are not reduced. Financial markets exist to provide price discovery and efficiently allocate resources to increase economic productivity and improve living standards. By targeting asset prices in an attempt to grow the economy, the Fed encourages excessive leverage and speculation, which leads to sudden increases in volatility and unstable financial markets. Additionally, the Fed's intervention into the markets leads to wealth inequality, malinvestment, lower productivity, and declining living standards.

Sector Review: Seven of the eleven sectors of the S&P 500 declined in January. The positive sectors were energy, healthcare, and consumer discretionary, while the consumer staples and the industrials performed worst. Interestingly, in this "risk-off" environment, the safe havens – U.S. long-term bond and gold performed poorly, while the speculative Russell 2000 and Emerging markets were strong.

Our Model Portfolio:

The benchmark for our model portfolio is the Traditional Blend — 60% equity, 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, we risk-weight our positions to manage volatility.

In January, we performed in line with our 60/40 benchmark while assuming less market risk. Our investments in the MSCI Emerging Markets, the GSCI Commodity Index, the S&P MidCap 400, the energy sector, and the Alerian MLP had a positive return for the month.

Our laggards in the portfolio were the industrials, financials, gold, and U.S. long-term bond.

Our portfolio is positioned for a reflationary economic environment (accelerating growth and inflation). The successful rollout of the vaccine and additional fiscal stimulus should lead to an economic acceleration this spring as the economy reopens and consumers spend their pent-up savings. We are overweight the economically sensitive sectors of the market (industrials, financials, and energy) and have exposure to the international and emerging markets, which are inexpensive and should benefit from a weak dollar.

Last year, we invested in the safe havens – gold and the U.S. long-term Treasury bond -- to hedge our equity exposure from the momentous economic risks. This year, we are invested in commodities, energy, gold, and foreign markets to hedge our equity exposure from a likely inflation acceleration. While inflation has not been a problem for more than thirty years, the unprecedented monetary and fiscal stimulus used to support the economy during the Covid shutdowns will have unintended consequences.

Our portfolio is positioned for a reflationary economic environment (accelerating growth and inflation). While our portfolio has the same overall risk level as our benchmark, we are underweight equities and fixed income and overweight commodities.

Our short-term (three-month) outlook is neutral:

Since the late-October vaccine low, the S&P 500 has rallied nearly 22%. We believe that the market offers a poor short-term risk-reward because it is very overbought, investors are euphoric, and signs of irrational speculation are occurring daily. In February, rising inflation expectations and higher long-term interest rates have adversely affected many of the overvalued growth stocks. We expect that higher interest rates will continue to pressure growth stocks as the virus is defeated and the economy rebounds. We expect to increase our tactical risk exposure during periods of weakness when investors are fearful, the market is oversold, and breadth improves. Our short-term market outlook is neutral.

Our long-term (more than four years) outlook is neutral:

We believe that the S&P 500 offers a poor risk-reward because it is extremely overvalued and has a 24% weighting to the over-owned mega-cap tech stocks. Conversely, the value sector of the market (economically sensitive, mid-cap, and international stocks) offers a favorable risk-reward and should perform well as the virus recedes and the economy reopens. Recently, the virus is in retreat, and the rotation from the mega-cap tech stocks into the value sector has begun. Over the next few quarters, we see a significant opportunity to invest in these value sectors of the market while avoiding the mega-cap tech and the S&P 500. While we expect to profit from the reflationary rotation into the cyclical stocks, longer-term, we remain concerned about the artificially low-interest rates and our record debt burden. Our Strategic Asset Allocation is underweight equities relative to our benchmark.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. All investments contain risk.