The Fed Admitted That Inflation May Not Be Transitory, but Actions Speak Louder Than Words

Although the S&P 500 reached an all-time high, the major indexes were mixed in May because inflationary concerns tempered investor’s optimism over the economic reopening.

Executive Summary

Although the S&P 500 reached an all-time high, the major indexes were mixed in May because inflationary concerns tempered investor’s optimism over the economic reopening.

Despite higher than expected inflation and the surging stock, commodity, and housing markets, Fed Chairman Powell stated in May that the Fed was not yet “talking about talking about” tapering their emergency policies because the jobs market remained in a huge hole.

Investors were not as confident that inflation was “transitory,” and they aggressively rotated from the interest-sensitive growth sector to the economically sensitive value sector of the market. The Russell 1000 Value index rallied by 2.14%, while the interest-sensitive Russell 1000 Growth index fell by 1.47% -- i.e., value outperformed growth by 3.61% in May. Year-to-date through May 31st, the value sector has outperformed the growth sector by 11.0%.

On June 16th, the Federal Reserve surprised investors by stating that the inflation surge may not be transitory. Also, they revised their 2021 economic forecast revised higher. Real GDP is expected to grow at 7.0%, and inflation was revised significantly higher to 3.4% from 2.4%. Additionally, they signaled that the QE taper debate had started, and interest rates would rise sooner than previously expected.

Actions speak louder than words, and since the Fed will not act for the foreseeable future, we expect that inflation will become a more significant problem this fall. We expect the labor market will be robust as the economy accelerates, the PUA expires, and caregivers return to work. Also, since the European Union (the second-largest economy behind the U.S.) remains essentially closed, we believe the global economy and inflation are poised to surge as Europe becomes vaccinated and their economy reopens. We will continue to invest in the value sectors of the market (financials, industrials, materials, and energy) and commodities that will benefit from the global economic and inflationary surge.

By most valuation measurements, the stock market has never been more expensive. According to Factset, the forward 12-month P/E ratio for the S&P 500 is 22.4, which is 40% above the 10-year average of 16. While we expect value will continue to outperform growth in the second half of the year, we believe that stocks are extremely overvalued and offer a poor long-term risk-reward.

Market Discussion:

Although the S&P 500 reached an all-time high, the major indexes were mixed in May because inflationary concerns tempered investor’s optimism over the economic reopening. The S&P 500 and the small-cap Russell 2000 appreciated by 0.7% and 0.2%, respectively, while the Nasdaq Composite fell by 1.4%. The safe havens were also mixed, the U.S. long-bond was flat, and Gold appreciated by 7.7%.

As the economy reopened, economic growth accelerated, and inflation surged (see chart below). The Federal Reserve stated that the greater than expected inflation was not a concern because it was “transitory” since it was due to temporary supply chain disruptions and easy base effects (artificially low comparisons due to last year’s economic shutdown). Despite higher than expected inflation and the surging stock, commodity, and housing markets, Fed Chairman Powell stated that the Fed was not yet “talking about talking about” tapering their emergency policies because the jobs market remained in a huge hole.

Investors were not as confident that inflation was “transitory,” and they aggressively rotated from the interest-sensitive growth sector to the economically sensitive value sector of the market. The Russell 1000 Value index rallied by 2.14%, while the interest-sensitive Russell 1000 Growth index fell by 1.47% -- i.e., value outperformed growth by 3.61% in May. Year-to-date through May 31st, the value sector has outperformed the growth sector by 11.0%.

As the global economic recovery gains momentum, we expect inflation and interest rates to move higher and the economically sensitive value sector (financials, industrials, materials, and energy) to continue their outperformance over the interest-sensitive growth sector.

By most valuation measurements, the stock market has never been more expensive. According to Factset, the forward 12-month P/E ratio for the S&P 500 is 22.4, which is 40% above the 10-year average of 16. While we expect value will continue to outperform growth in the second half of the year, we believe that stocks are extremely overvalued and offer a poor long-term risk-reward.

Chart 1: In May, Core-PCE Inflation (the Fed’s favorite measure of price stability) jumped to the highest level since 1992. While the Fed believes this increase is “transitory,” booming equity, housing, and commodity markets may indicate that the Fed-induced a financial bubble.

Source: FRED.com

To stabilize the economy during the pandemic, the Fed cut interest rates to 0% and printed $120 billion each month to buy financial assets. In May, the Fed stated that they have not even discussed reducing their emergency monetary measures because the labor market had not sufficiently recovered, and the inflationary surge was “transitory.”

The Federal Reserve has a dual mandate of “maximum employment” and “stable prices.” Recently, they indicated that they would risk stable prices to achieve maximum employment. Unfortunately, it is not that simple, and the Fed may be making a significant policy error.

While the recent employment reports were disappointing, it is difficult to analyze the post-pandemic job market because many people unexpectedly retired during the pandemic. Also, since most schools were closed, caregivers had to leave their job to supervise their children’s distance learning. Additionally, the federal government extended their pandemic unemployment assistance (PUA), which in many cases incentivizes (or pays) workers to stay home. In our view, the unemployment rate will remain uncertain until the fall, when the PUA benefits expire and the schools reopen.

While it is difficult to know what post-pandemic “maximum employment” is, it is clear that inflation is surging. While the Fed believes that inflation is “transitory,” we are concerned that their unprecedented monetary policies created financial asset bubbles and an inflation problem.

According to famed economist Milton Friedman, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” Over the past fifteen months, the Fed has increased the quantity of money to an unprecedented level. We believe that this profligate increase in the money supply, not the base effects or supply chain issues, is responsible for the inflationary surge and booming asset prices (stocks, housing, and commodities).

Chart 2: To combat the economic shutdown, the Fed has increased the money supply by a historic amount. We believe higher inflation and asset bubbles are the unintended consequence of the Fed’s reckless monetary policy.

Source: FRED

Last Wednesday, the Federal Reserve surprised investors by stating that the inflation surge may not be transitory. Also, they revised their 2021 economic forecast revised higher. Real GDP is expected to grow at 7.0%, and inflation was revised significantly higher to 3.4% from 2.4%. Additionally, they signaled that the QE taper debate had started, and interest rates would rise sooner than previously expected. The Fed’s hawkish pivot led to a sharp but brief market decline and a rotation out of the economically sensitive sectors of the market.

Although the Fed admitted that the inflationary surge might not be transitory, they continue to print $120 billion per month to buy financial assets, and they do not expect to increase short-term interest rates until 2023. Since inflation is currently 5% and interest rates are 0%, real interest rates (interest rates minus inflation) are the lowest since 1980 (see chart below).

Chart 3: The Fed’s emergency monetary measures and surging inflation produced the lowest real interest rates since 1980. Since monetary policy acts with a lag, inflation could become a significant headwind for investors.

Source: FRED.com

Actions speak louder than words, and since the Fed will not act for the foreseeable future, we expect that inflation will become a more significant problem this fall. We expect the labor market will be robust as the economy accelerates, the PUA expires, and caregivers return to work. Also, since the European Union (the second-largest economy behind the U.S.) remains essentially closed, we believe the global economy and inflation are poised to surge as Europe becomes vaccinated and their economy reopens.

We expect the U.S. 10-year Treasury bond yield to rise to at least 2.75% during this reflationary environment, which would pressure the interest-sensitive growth stocks.

Chart 4: During the past three economic cycles, the U.S. 10-year Treasury bond yield peaked approximately 2.5% above the U.S. 2-year Treasury bond. We expect that the historical precedent will continue, and the U.S. 10-year Treasury bond yield will approach 3% during this economic cycle.

Source: FRED

In summary, the S&P 500 rallied to a record high because of the successful vaccine rollout, the surging growth due to the reopening of the economy, and the massive monetary stimulus. We are concerned that financial markets will be vulnerable as the global economy surges and the Fed is abruptly forced to tighten monetary policy. We will continue to invest in the value sectors of the market (financials, industrials, materials, and energy) and commodities that will benefit from the global economic and inflationary surge.

Sector Review:

Inflationary concerns led to the value sectors significant outperformance in May. We expect the value sector of the market (financials, industrials, materials, and energy) will continue to outperform during this reflationary economic environment.

Our Model Portfolio:

The benchmark for our model portfolio is the Traditional Blend — 60% equity, 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment portfolio is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, we risk-weight our positions to manage volatility.

We remain positioned for a reflationary economic environment (accelerating growth and inflation). We are concerned that significant monetary and fiscal policy errors could lead to an inflation problem in the second half as the global economy accelerates.

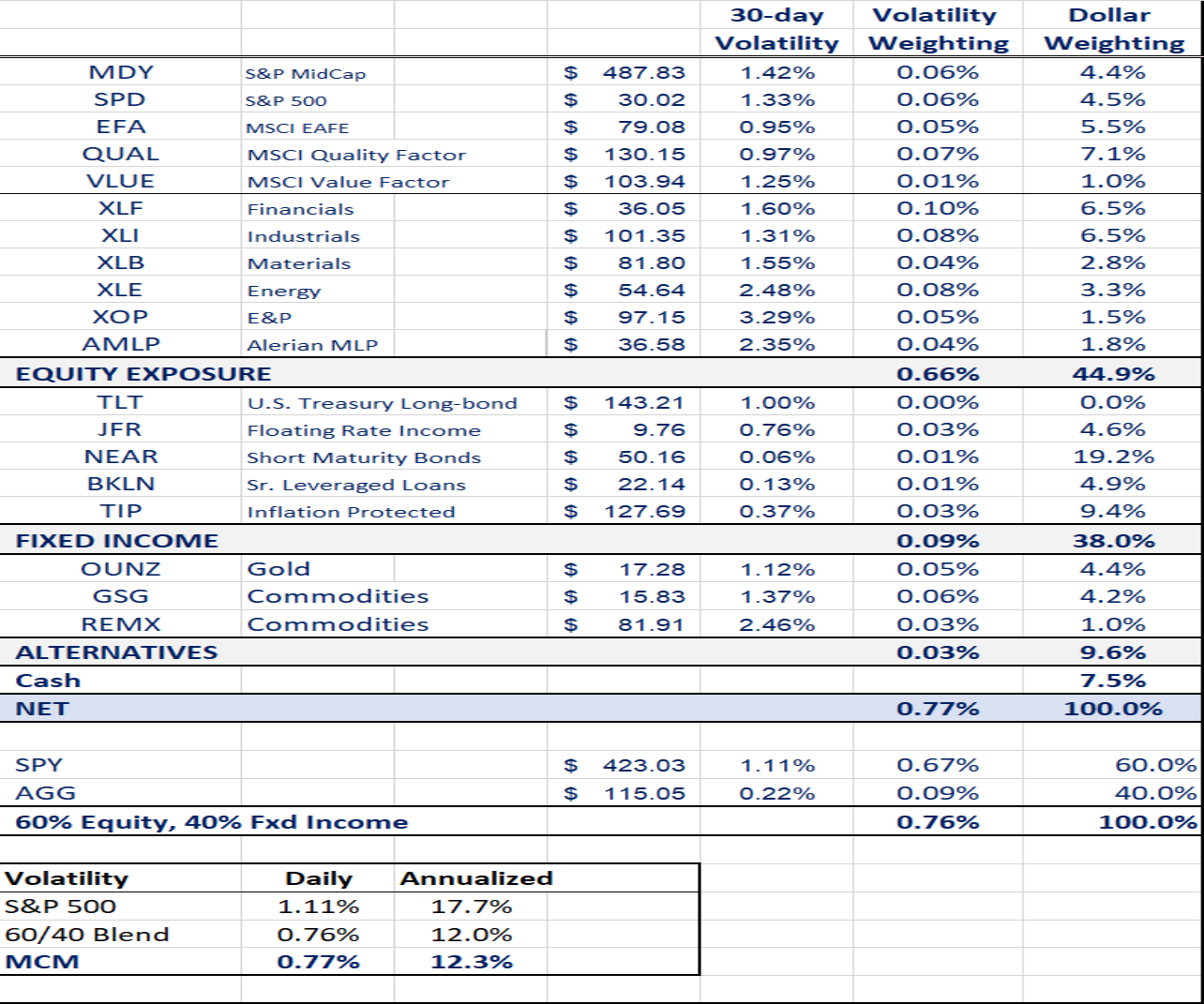

Our core positions are in the economically sensitive sectors of the market (industrials, financials, and Energy), commodities, and TIP’s (U.S. Treasury Inflation-Protected Securities). We remain underweight equities and fixed income duration and overweight commodities relative to our benchmark. Our portfolio’s annualized volatility is 12.3%, which is inline with our benchmark.

Current Risk-Weighted Portfolio:

Our short-term (three-months) outlook is neutral:

We believe that the market offers a poor short-term risk-reward because investors are complacent, and market breadth is deteriorating. Narrowing market breadth typically presages a market correction. After the market’s record run, we believe that a correction to reduce the excesses would be healthy. When investors are fearful, the market is oversold, and breadth begins to improve, we expect to increase our tactical risk exposure. Our short-term market outlook is neutral.

Our long-term (more than four years) outlook is neutral:

We believe that the S&P 500 offers a poor risk-reward because it is extremely overvalued. Also, we are concerned about the long-term unintended consequence of the unprecedented monetary and fiscal policy that was used to combat the pandemic. Artificially low interest rates and historic peacetime deficits have led to a record debt burden, which will become problematic as the economy grows, and interest rates normalize.

Over the next two quarters, we continue to see a significant opportunity to invest in the value sectors of the market while avoiding the mega-cap tech and the S&P 500. While we expect to profit from the reflationary rotation into the cyclical stocks, longer-term, we remain concerned about the impact rising interest rates will have on stock valuations. Our Strategic Asset Allocation is underweight equities relative to our benchmark.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. All investments contain risk.