Manley Market Memo

Congress Fails as the Virus Accelerates, yet the S&P 500 Sells at a Record Valuation?

Executive Summary

We believe that stocks offer a poor risk-reward. Despite the great uncertainty over the virus, the economy, and the election, stocks have never been more expensive because the Fed created another financial bubble by printing $3 trillion.

We believe the economy and the financial markets are vulnerable without additional stimulus to support the service economy until a vaccine is widely available. Unfortunately, it is unlikely that Congress will agree to a new stimulus bill until after the election is decided.

Once a vaccine is widely available, we expect a large rotation out of the mega-technology stocks that benefitted from the pandemic into the market's value sectors -- energy, financials, industrials, and materials. We see a tremendous long-term opportunity in owning these "beaten-up' sectors while avoiding the over-valued, over-owned, mega-cap technology stocks and the S&P 500, which has a 23% weighting to the group.

Our model portfolio is defense and underweight risk relative to our 60/40 benchmark.

Market Discussion:

September Market Review: After the strongest August since 1986, the S&P 500 fell by 4.1% in September, which was its first monthly decline since the March panic low. Both the S&P 500 and the Nasdaq dropped by more than 10% from their late-August peak. During this "risk-off" environment, the safe havens performance was disappointing– the long-term U.S. Treasury bond increased by 0.7%, while gold fell by 4.4%.

As discussed last month, we believed that stocks were due for a decline because the market was overbought, breadth was weak, and extreme optimism and speculation were rampant. Since the rally was driven by only a few mega-cap technology stocks (Apple, Amazon, Microsoft, Google, and Facebook), breadth was very poor, which typically indicates a vulnerable market.

While some setbacks occurred in September (two vaccine trials were temporarily halted and stimulus negotiations showed little progress), no apparent catalysts led to the September selloff. It appears that profit-taking in the mega-technology stocks -- which represent 23% of the S&P500 -- snowballed to more aggressive selling.

We continue to believe that stocks offer a poor risk-reward. Although we are in the deepest recession in a generation, and there is significant uncertainty regarding the virus and the election, the S&P 500 remains near its all-time high and sells at a record valuation.

We believe that the Fed-induced another financial bubble, in which asset valuations are detached from the underlying fundamentals. To combat the pandemic, the Fed printed nearly $3 trillion to buy financial assets and provide liquidity to the markets. While the Fed's action drove the S&P 500 up 63.6% in five months, it did little to create economic demand or jobs for the 12.6 million people out of work because of the pandemic.

Today, stocks sell at a record valuation, yet the economy appears to be weakening, as the number of daily new virus cases in Europe and the U.S surge. In our view, the economy and the financial markets are at risk without additional stimulus to support the service economy until a vaccine is widely available. Unfortunately, it is unlikely that Congress will agree to a new stimulus bill until after the election is decided.

Year-to-date (through September 30th), the market's breadth remains poor. Technology, Consumer Discretionary, and Communication Service, which are dominated by the mega-cap stocks (Facebook, Apple, Amazon, Microsoft, and Google), have had a strong year while the other sectors are flat or down in 2020. In fact, despite the 64% rally off the March low, five of the S&P 500's eleven sectors remain negative for the year. In fact, while the S&P 500 is near an all-time high, the Energy and Financial sectors have declined by 50.1% and 21.8%, respectively, year-to-date. The safe havens -- gold and the U.S. Treasury long bond -- continue to perform very well during this volatile and challenging year.

We remain focused on the Financial sector, which continues to disappoint. In September, the Financials declined nearly 4% and are down by 21.8% this year. This poor performance is concerning since the financials play a critical role in funding economic growth, and they typically begin to outperform the S&P 500 five months before the economic expansion starts. Since the Financials continue to lag the S&P 500 significantly, we believe that economic growth will disappoint ebullient investors, and the market is poised for a deeper correction.

The S&P 500's Sector Year-to-Date Performance

(through October 27th, 2020)

S&P 500 Index +5.3%

Economically Sensitive Sectors

Technology XLK +26.4%

Consumer Discretionary XLY +19.6%

Communication Services XLC +13.3%

Materials XLB +4.8%

Industrials XLI (2.9%)

Financials XLF (19.8%)

Energy XLE (51.2%)

Defensive, Non-Cyclical Sectors

Health Care XLV +4.7%

Consumer Staples XLP +2.5%

Utilities XLU +0.2%

Real Estate XLRE (8.9%)

Safe Havens

U.S. Treasury Long bond (TLT) 18.5%

Gold (GLD) 25.4%

Market Outlook:

We believe that stocks offer a poor risk-reward. Despite the great uncertainty over the virus, the economy, and the election, stocks have never been more expensive because the Fed created another financial bubble by printing $3 trillion.

Hopefully, over the next 4 to 8 weeks, many of these uncertainties should be resolved. While it is impossible to know what will happen, we know that stocks are very expensive and vulnerable if the virus continues to accelerate, the economy weakens, or there is a contested election.

In 2001, Waren Buffet told Fortune magazine that the Market Cap to GDP valuation measure is "probably the best single measure of where valuations stand at any given moment." Currently, the market value of the stock market is equal to 180% of GDP. Based on this valuation measure, stocks have never been more expensive, and today stocks are 29% more expensive than during the 2000 technology bubble (see chart below). Historically, market cap is equal to 65% of GDP, so based on this valuation measure, stocks are more than 50% overvalued.

Source: Gurufocus.com

We are concerned that the S&P 500's strength has masked how weak the economy is and how poorly Main Street is doing. The S&P 500 bottomed in March and rallied by 63.7% over the next five months because of the massive fiscal and monetary stimulus. While the S&P 500 rallied to an all-time high, the labor market remained in a deep recession.

Currently, the 4-week moving average of Initial Unemployment Claims is 811,250, which is worse than the peak of any recession since the Great Depression. Today, initial unemployment claims remain significantly greater than the height of the 2007/2008 Great Financial Crisis, which peaked at 659,250 initial unemployment claims (see chart below).

Source: FRED

While we are very cautious and believe that the next few months may be trying and volatile, we are hopeful that a vaccine is near, and the economy could begin to improve late next spring. Once the virus is contained, we expect a large rotation out of the mega-technology stocks that benefitted from the pandemic into the market's value sectors -- energy, financials, industrials, and materials. We see a tremendous long-term opportunity in owning these "beaten-up' sectors while avoiding the over-valued, over-owned, technology stocks and the S&P 500, which has a 23% weighting in these stocks.

The energy sector is an example of the tremendous long-term potential we see in the market's value sectors. The energy sector declined by 50% in 2020 and is only a 2.5% weighting in the S&P 500 -- in 2008, the energy sector was 16% of the S&P 500, and in 1980 it was 33%. Incredibly, Apple, Microsoft, Amazon, Google each have a greater weighting in the S&P 500 than the entire energy sector.

The industry is consolidating, and there have been four large mergers over the past month, which should lead to greater long-term profitability. Today, the energy sector remains highly leveraged to economic growth and provides a good inflation hedge, which may be useful given the large budget deficit and the Fed's profligate monetary policies.

It is interesting to note that in 2010, Exxon was the largest company in the world, yet today Zoom Video Communications is slightly larger with a market cap of $145 billion despite only $1.3 billion in sales.

Our Model Portfolio:

The benchmark for our model portfolio is the Traditional Blend — 60% equity, 40% bonds. Our goal is to outperform the benchmark with less risk. To outperform, our investment universe is diversified and economically balanced. We eliminate laggards and tilt the portfolio toward our location in the business cycle. Finally, we risk-weight our positions to manage volatility.

Our model portfolio is invested in the defensive sectors of the market. We are long the Quality and Minimum Volatility Factors, and the Healthcare, Consumer Staples, and Utility sectors of the market. Our only economically sensitive exposure is to the Consumer Discretionary and Communications sectors. Additionally, we are long the Emerging markets and Japan. We believe that international equity diversification makes sense because of the U.S’s weak dollar policy (large deficit spending and Quantitative Easing) and the probability that the technology bubble is poised to deflate.

We remain long the safe havens (gold and long-term U.S. Treasury bonds), and Treasury Inflation-Protected Securities (TIPS), which are bonds that protect from inflation. From a risk perspective, we remain defensively positioned relative to our benchmark.

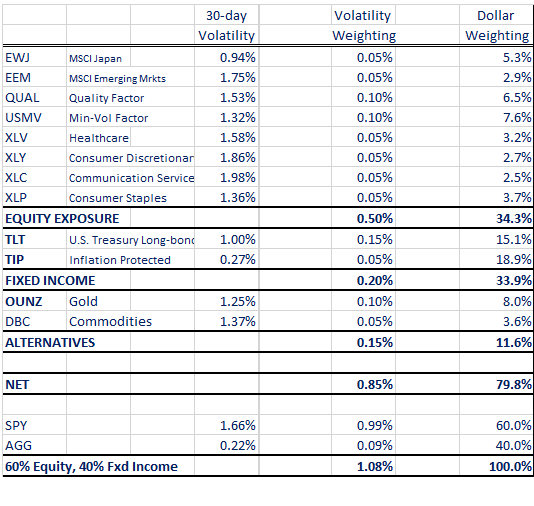

Historically, the 60/40 portfolio had an equity risk weighting of around 0.60% per day. Currently, our equity risk level is 0.50% with the benchmark’s historic average, and we are only 34.3% invested in stocks, because the market’s volatility is significantly elevated. Our risk exposure is allocated 59% to equities, 29% to gold, and 19% to fixed income, while our 60/40 benchmark has 89.6% of its risk allocated to equities (see table below)

Our portfolio has economically balanced from a risk perspective, and we remain defensively positioned relative to our benchmark. Our risk exposure is allocated 57% to equities, 23.5% to fixed income, and 17.6% to gold/commodities, while our 60/40 benchmark has 92% of its risk allocated to equities (see table below).

We believe that our high quality, defensive portfolio should outperform our benchmark during this volatile period of considerable economic uncertainty.

Our short-term (three-month) outlook is negative:

We believe that the bubble in mega-tech stocks burst, and stocks are vulnerable as the virus accelerates and the economic rebound stalls. We don't expect more fiscal stimulus until after the election is decided. The market offers a poor short-term risk-reward, and we expect to increase our tactical risk exposure when investors are fearful, the market is oversold, and breadth improves. Unfortunately, we don't expect a significant short-term bottom until the election is decided. Our short-term market outlook is negative.

Our long-term (more than four years) outlook is negative:

We believe that stocks offer a poor long-term risk-reward, and we remain underweight equities relative to our benchmark. Stocks are expensive, the year-over-year growth rate is deeply negative, and corporate debt is at a record level. We will remain defensively postured until the market offers a favorable risk-reward, i.e., valuations improve, and economic growth accelerates. Once the virus is contained, we expect a large rotation out of the mega-technology stocks that benefitted from the pandemic into the market's value sectors – i.e., energy, industrial, materials and financials. We see a significant opportunity in investing in these value sectors of the market while avoiding the mega-tech and the S&P 500. Our Strategic Asset Allocation is underweight equities relative to our benchmark; we are invested in the defensive sectors of the S&P 500 and the safe havens (gold and the U.S. long-bond).

In summary:

Since the market offers a poor long-term risk-reward, and there is unprecedented uncertainty, we will remain defensively postured and focused on preserving capital. We strongly believe that the key to growing wealth and compounding at an optimal rate is to avoid significant drawdowns, which typically appear in high-risk periods similar to today. We will continue to focus on preserving capital during this volatile and uncertain time. Protecting wealth will ensure that we will have significant cash available to take advantage of the substantial opportunities when the recession is over, the virus is contained, and stocks offer a favorable risk-reward.

If there are any questions or comments, please do not hesitate to contact me directly.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. This newsletter is not a substitute for professional investment services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. All investments contain risk.