It's Time to Consider a Roth Conversion

Reduce Tax Risk and Uncertainty in Your Retirement Years

It is a great time to consider a Roth Conversion (converting your 401K or Traditional IRA into a Roth IRA) because tax rates are unlikely to be this low again. In December 2017, Congress passed the 2017 Tax Cuts and Jobs Act (TCJA), which reduced tax rates to today's historically low level.

While these tax cuts are scheduled to expire in 2025, the massive budget deficit due to the Covid-19 pandemic, the unprecedented national debt burden, and the aging of the Baby Boomer generation may lead to higher taxes sooner – especially if the Democrats win the Georgia Senate run-off in January.

Key Points:

2020 has been a very difficult and trying year. If your income or a portion of your equity portfolio is depressed, a Roth Conversion may make sense this year, though time is running out since conversions must take place by December 31st to qualify as 2020 income.

Converting a traditional IRA or 401K to a Roth IRA in 2020 removes future tax uncertainty and risk because your retirement savings grow tax-free, and there are no required minimum distributions (RMDs).

Traditional IRAs and 401Ks are solid retirement vehicles because contributions are tax-deductible, and the taxes on your savings are deferred until retirement. Unfortunately, at 72 years old, Uncle Sam requires you to make a required minimum distribution (RMD) and pay ordinary income tax on the distribution – even if you don't need the money. While no one knows what tax rates will be in the future, given our record debt, and entitlement liabilities, we believe tax rates could be significantly higher as the baby boomer generation retires.

Roth IRAs are an excellent estate planning tool because heirs receive investments that will grow tax-free.

What is a Roth IRA?

A Roth IRA is an individual retirement account, which is funded with after-tax dollars, offers tax-free investment growth and tax-free withdrawals in retirement. Since you do not pay taxes on your withdrawals during retirement, a Roth IRA reduces tax risk and uncertainty in retirement. Also, a Roth IRA provides maximum flexibility since there is no annual required minimum distribution (RMD), and you can leave this tax-free asset to your heirs.

What is a Roth Conversion?

A Roth IRA conversion is a transfer of retirement assets from a tax-deferred retirement account (Traditional, SEP, or SIMPLE IRA) into a tax-exempt Roth IRA. This transfer creates a taxable event, in which the amount transferred is taxed as ordinary income. The deadline for conversions to count as 2020 income is December 31st, 2020.

To avoid a penalty, it is crucial to pay the tax liability from a source other than your IRA. Also, you must keep the assets in the Roth IRA for five years, after conversion, for the Roth IRA to qualify for tax-free status. Withdrawals can be made tax-free once the five-year period ends and you are older than 59.5 years old. Importantly, Roth Conversions can no longer be reversed.

Why You Need to Consider a Roth IRA Conversion Today

2020 has been a very uncertain and tragic year. If your income is down or your tax-deferred savings account has declined, the tax liability associated with a Roth Conversion will likely be reduced.

Diversification and risk management are important financial concepts that apply not only to investment portfolios but also asset location. Since no one knows where tax rates will be decades into the future, it is important to diversify the location of your retirement accounts between taxable, tax-exempt, and tax-free.

During the retirement years, individuals try to find ways to reduce uncertainty and minimize their income tax bills. A Roth IRA can be an excellent way to eliminate tax rate risk and uncertainty, especially if you think future tax rates will be higher.

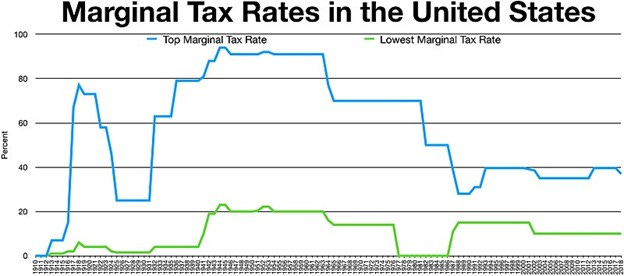

While tax rates have been low for the last thirty years, it is interesting that in 1986, the top marginal tax rate was 50%, and it was 70% in 1980 (see chart below).

Source: Wikimedia Commons

While tax rates are (hopefully) unlikely to return to the repressive rates of the past, there are long-term structural imbalances that will likely drive tax rates higher in the future. The Covid-19 pandemic has lead to a sharp economic downturn, which cost more than 10 million jobs. To stabilize the economy during the pandemic, Congress passed the $2.2 trillion CARES Act and ran massive budget deficits. The Congressional Budget Office (CBO) projects a federal budget deficit of $3.3 trillion this year, which is nearly 16% of GDP. Over the last 50 years, the average budget deficit is 3% of GDP, and the 2020 budget deficit is expected to be 60% greater than the deficit recorded during the Great Recession (see chart below).

Source: CBO

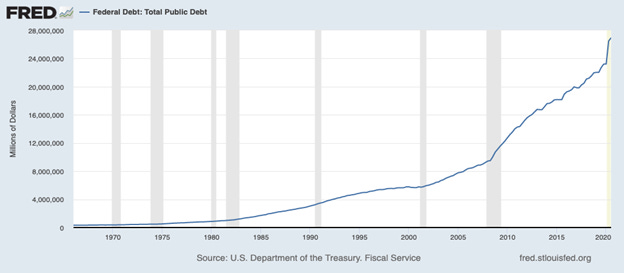

The recession and record deficit spending led to massive federal borrowing. Today, the national debt is a record $26.95 trillion, a 135% increase from the 2008/2009 financial crisis (see chart below).

Source: FRED

Since the beginning of the last recession, debt to GDP has grown from 64% to a record 127% (see chart below).

Source: FRED

While interest rates are low today because of the recession, as economic growth returns and interest rates normalize, this record debt level's cost will surge. To service this considerable debt burden, we believe that taxes and inflation will rise. Unfortunately, neither option is good for retirees.

In addition to our debt problem, we have massive unfunded entitlement liabilities (social security and medicare). Each day approximately 10,000 baby boomers (born between 1946 and 1964) turn 65 years old. As baby boomers retire and receive social security and medicare, the federal government's tax receipt declines as their entitlement expenditures expand. Since the last baby boomer won't turn 65 until 2029, we believe that tax rates could trend higher for decades.

A Roth IRA is Not For Everyone

If you expect lower taxes in the future

If you may need to withdraw the money in less than five years

If you can not pay the tax out of a taxable account

Summary

Unlike 401Ks and Traditional IRAs, a Roth IRA provides tax-free investment growth and tax-free withdraws

There are no RMDs, so you take your money out when you need it, not when the government requires you to

Roth IRA's eliminate the uncertainty and risk of higher tax rates in the future

Since heirs receive tax-free assets, Roth IRA's are an ideal legacy

Next Steps

For more details or to learn if a Roth Conversion makes sense for you, please contact us, and we will perform a FREE Roth Conversion analysis. Remember, to qualify for the 2020 tax year, Roth Conversions must be completed by December 31st.

For the do-it-yourselfers, consider the following steps:

Roughly calculate your 2020 taxable income

Estimate your 2020 income to determine your marginal tax rate and be sure to include capital gains (capital losses can reduce income by up to $3,000)

Subtract your deductions. Do you itemize or use the standard deduction of $12,400 for single or $24,800 for married?

Find your marginal tax bracket (see tax table below)

How much can you convert before going into the next tax bracket?

What is your likely tax on the conversion?

Can you pay that amount from sources other than your IRA?

How much can you convert by going into the next tax bracket?

What is your likely tax on the conversion?

Can you pay that amount from sources other than your IRA?

Source: IRS

Please contact a tax professional before taking any action, especially because Roth Conversions are no longer reversible.

Disclaimer: The material in this newsletter is for educational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. This newsletter is not a substitute for professional investment or tax services. Past performance is no guarantee of future results, and there is no assurance that investment objectives will be achieved. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. All investments contain risk.